---

title: "Marketing Mix Analytics"

author: "Bongo Adi"

---

```{python}

#| label: python-setup-45-marketing-mix-analytics

#| include: false

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import optimize

from sklearn.linear_model import Ridge, LinearRegression

from scipy import stats

from scipy.stats import norm

from scipy.optimize import minimize, LinearConstraint, Bounds

```

::: {.callout-note icon="false"}

## 📋 Learning Objectives

- Understand the principles and applications of Marketing Mix Modelling (MMM) in decomposing sales by marketing channel

- Master the Adstock transformation and saturation curves for realistic media response modelling

- Build and interpret MMM regression models with control variables and seasonal adjustment

- Apply Bayesian methods to quantify uncertainty in channel attribution

- Decompose revenue contributions and calculate marginal ROI by channel

- Optimise marketing budget allocation across channels to maximise total revenue

- Implement MMM workflows in both R and Python with Nigerian consumer goods data

:::

## What Is Marketing Mix Modelling?

Marketing Mix Modelling (MMM) is a statistical technique that decomposes total sales or revenue into the contributions from each marketing channel—television, radio, digital, outdoor, influencers, and more. In the post-cookie era, where third-party audience data has become scarce and conversion tracking fragmented, MMM provides marketers with an aggregate-level view of channel effectiveness without requiring individual-level tracking. The core business question is deceptively simple: "How much of our revenue came from TV versus radio versus digital versus out-of-home advertising?"

In the Nigerian context, this question becomes particularly nuanced. Nigerian brands operate across extraordinarily diverse media ecosystems. Television remains a mass reach medium—national networks like NTA, Channels Television, AIT, and numerous regional Hausa-language stations (BBC Hausa, Voice of Nigeria) still command significant audiences, particularly in Northern and rural markets. Radio, often dismissed in developed markets, remains a primary medium in Nigeria, with heavy listenership during morning drive times and afternoon commutes. Traditional outdoor billboards along major corridors—the Lagos-Ibadan Expressway, the Abeokuta-Ibadan road, and routes into Abuja—reach commuters and travelers daily. Digital channels (Facebook, Instagram, Google Search, TikTok) have exploded in urban centres and are increasingly accessible via mobile-only consumers. Influencer marketing, from mega-influencers with millions of followers to micro-influencers with hyper-local reach, has become a significant spend category for consumer goods brands targeting youth demographics.

Why MMM matters more than ever is rooted in this fragmentation and the erosion of deterministic attribution. A decade ago, advertisers could often trace a customer's path: click a Facebook ad, land on a website, make a purchase, and credit Facebook with the conversion. Today, the customer journey is far more opaque. A consumer might see a TV commercial on DStv or StarTimes, remember the brand vaguely, search for it on Google days later, see a retargeting ad on Instagram, and finally purchase offline at a Shoprite or Naira box corner shop. Which channel deserves credit? MMM sidesteps this attribution problem by using statistical modelling to estimate how much each channel contributed to aggregate sales, even without individual-level conversion data. It answers the question with confidence intervals, acknowledging the inherent uncertainty in attribution estimation.

## The Adstock Transformation

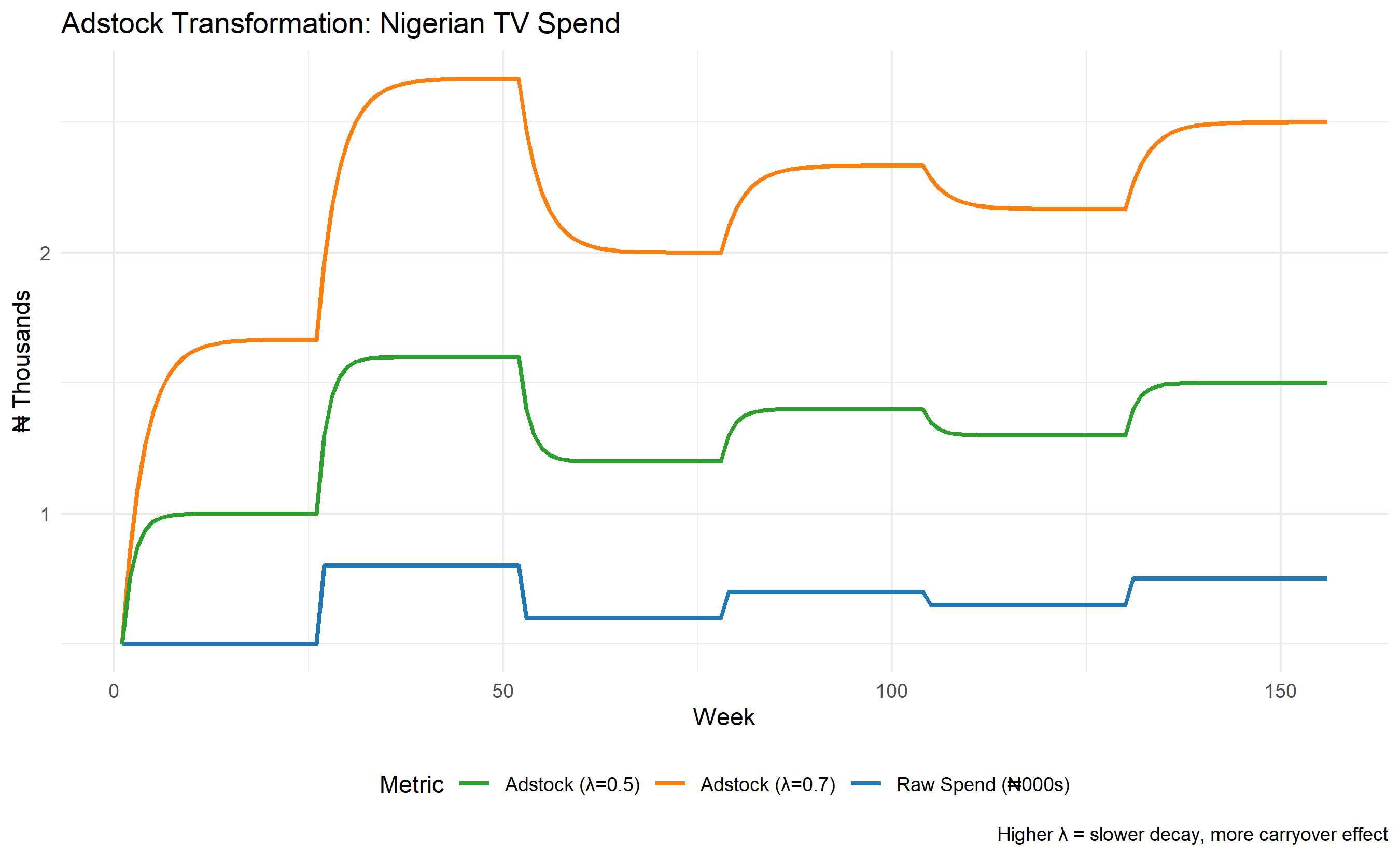

Advertising does not produce instantaneous sales. A television commercial aired on Monday does not cause a purchase solely on Monday; rather, some of its effect decays over subsequent days and weeks. This carryover effect—the delayed and diminishing impact of advertising—is fundamental to realistic media modelling. The Adstock transformation is a mathematical tool that converts raw media spend into a "stock" of advertising goodwill that decays geometrically over time.

The core Adstock recurrence relation is:

$$\text{Adstock}_t = \text{Spend}_t + \lambda \times \text{Adstock}_{t-1}$$

where $\text{Spend}_t$ is the media spend in period $t$ (say, a week), $\lambda$ is the decay rate (typically between 0 and 1), and $\text{Adstock}_{t-1}$ is the carryover from the previous period. When $\lambda = 0$, there is no carryover—the effect is instantaneous. When $\lambda = 0.5$, 50% of the advertising stock persists from one period to the next. As $\lambda$ approaches 1, the advertising effect becomes quasi-permanent, which is unrealistic for most categories. A practical decay rate of $\lambda = 0.7$ implies a half-life (the time for the effect to decay to 50% of its peak) of about 3 weeks; this can be calculated as $\text{half-life} = \log(0.5) / \log(\lambda)$.

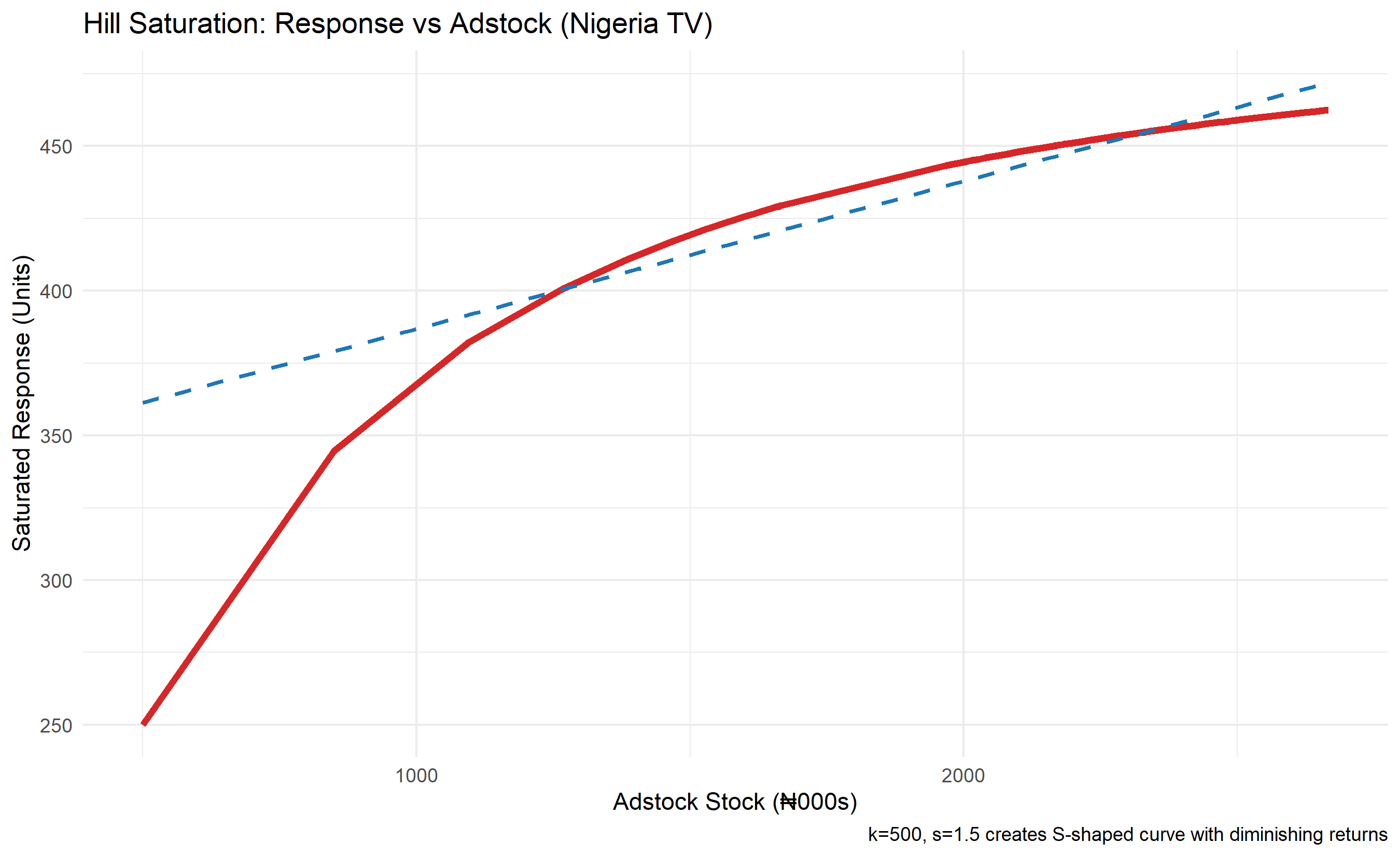

Beyond carryover lies saturation: the observation that each additional dollar of advertising generates fewer additional sales. This is the principle of diminishing returns. A brand with zero awareness must spend heavily on reach to build initial awareness, but once awareness plateaus at, say, 80%, additional spend achieves less relative gain. The Hill saturation function captures this curvature:

$$\text{Response}_t = \frac{k \times \text{Adstock}_t^s}{k^s + \text{Adstock}_t^s}$$

where $k$ is the half-saturation point (the Adstock level at which response reaches 50% of maximum), and $s$ is the shape parameter. When $s = 1$, the function is linear (no saturation). When $s > 1$, the curve exhibits S-shaped diminishing returns characteristic of most real advertising response.

The Adstock transformation matters tremendously in Nigerian marketing contexts because traditional media (TV and radio) have inherent carryover effects tied to viewer and listener routines. A television commercial broadcast on prime time (8–10 PM on weekdays) reaches a concentrated audience, but the brand recall persists for days, especially for established brands. Radio spots, often repeated multiple times across a week, build message frequency and top-of-mind awareness through repetition and decay dynamics. Digital channels, by contrast, often show shorter lags and faster decay; a Facebook ad is seen, forgotten, and superseded by new content within hours unless reinforced. Outdoor billboards operate on a different temporal rhythm—a driver passes a billboard once or twice daily, and the cumulative exposure builds mental associations over weeks. Failing to model these differences would lead to systematic overestimation of digital effectiveness and underestimation of traditional media's true contribution.

::: {.callout-note icon="false"}

## 📘 Theory: Adstock and Saturation in Media Response

The Adstock transformation converts media spend into a lagged stock that decays geometrically. This stock then saturates—additional units of stock produce diminishing returns. Together, Adstock and saturation form the foundation of realistic media response curves. The Adstock formula can also be written as an infinite sum of decaying past spend: $\text{Adstock}_t = \sum_{i=0}^{\infty} \lambda^i \times \text{Spend}_{t-i}$. The Hill saturation function is one of several choices; alternatives include the logistic curve $\frac{1}{1 + e^{-s(\text{Adstock}_t - k)}}$ and the Michaelis-Menten function. The choice of saturation functional form can significantly affect estimated ROI, and sensitivity analysis across functional forms is recommended best practice.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formulas

**Adstock Recurrence:**

$$\text{Adstock}_t = \text{Spend}_t + \lambda \times \text{Adstock}_{t-1}$$

**Half-Life Decay:**

$$\text{Half-life} = \frac{\log(0.5)}{\log(\lambda)}$$

**Hill Saturation Function:**

$$\text{Response}_t = \frac{k \times \text{Adstock}_t^s}{k^s + \text{Adstock}_t^s}$$

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch45-adstock-saturation

#| message: false

#| warning: false

library(tidyverse)

library(ggplot2)

# Set seed for reproducibility

set.seed(6247)

# Simulate synthetic Nigerian TV spend data: 156 weeks (3 years)

weeks <- 156

tv_spend <- c(

rep(500, 26), # Year 1, Q1-Q2: ₦500k/week

rep(800, 26), # Year 1, Q3-Q4: ₦800k/week (boost)

rep(600, 26), # Year 2, Q1-Q2: ₦600k/week

rep(700, 26), # Year 2, Q3-Q4: ₦700k/week

rep(650, 26), # Year 3, Q1-Q2: ₦650k/week

rep(750, 26) # Year 3, Q3-Q4: ₦750k/week

)

# Compute Adstock with decay rate λ = 0.7

compute_adstock <- function(spend, lambda) {

adstock <- numeric(length(spend))

adstock[1] <- spend[1]

for (t in 2:length(spend)) {

adstock[t] <- spend[t] + lambda * adstock[t - 1]

}

return(adstock)

}

# Compute for λ = 0.7 and λ = 0.5

adstock_0.7 <- compute_adstock(tv_spend, lambda = 0.7)

adstock_0.5 <- compute_adstock(tv_spend, lambda = 0.5)

# Hill saturation function

hill_saturation <- function(adstock, k, s) {

(k * adstock^s) / (k^s + adstock^s)

}

# Apply saturation (k = 500, s = 1.5 for moderate S-curve)

response_saturated <- hill_saturation(adstock_0.7, k = 500, s = 1.5)

# Create data frame for visualisation

df <- tibble(

Week = 1:weeks,

TV_Spend = tv_spend,

Adstock_0.7 = adstock_0.7,

Adstock_0.5 = adstock_0.5,

Saturated_Response = response_saturated

)

# Plot 1: Adstock transformation

p1 <- ggplot(df, aes(x = Week)) +

geom_line(aes(y = TV_Spend / 1000, colour = "Raw Spend (₦000s)"), linewidth = 1) +

geom_line(aes(y = Adstock_0.7 / 1000, colour = "Adstock (λ=0.7)"), linewidth = 1) +

geom_line(aes(y = Adstock_0.5 / 1000, colour = "Adstock (λ=0.5)"), linewidth = 1) +

scale_colour_manual(

values = c("Raw Spend (₦000s)" = "#1f77b4",

"Adstock (λ=0.7)" = "#ff7f0e",

"Adstock (λ=0.5)" = "#2ca02c")

) +

labs(

title = "Adstock Transformation: Nigerian TV Spend",

x = "Week",

y = "₦ Thousands",

colour = "Metric",

caption = "Higher λ = slower decay, more carryover effect"

) +

theme_minimal() +

theme(legend.position = "bottom")

print(p1)

# Plot 2: Saturation curve

p2 <- ggplot(df, aes(x = Adstock_0.7)) +

geom_line(aes(y = Saturated_Response), colour = "#d62728", linewidth = 1.5) +

geom_smooth(aes(y = Saturated_Response), method = "lm", se = FALSE,

linetype = "dashed", colour = "#1f77b4", label = "Linear fit") +

labs(

title = "Hill Saturation: Response vs Adstock (Nigeria TV)",

x = "Adstock Stock (₦000s)",

y = "Saturated Response (Units)",

caption = "k=500, s=1.5 creates S-shaped curve with diminishing returns"

) +

theme_minimal()

print(p2)

# Calculate and print half-life for λ = 0.7

half_life_0.7 <- log(0.5) / log(0.7)

cat("\n--- Adstock Decay Analysis ---\n")

cat("Half-life (λ = 0.7):", round(half_life_0.7, 2), "weeks\n")

cat("After 4 weeks:", round(0.7^4 * 100, 2), "% of peak effect remains\n")

cat("After 8 weeks:", round(0.7^8 * 100, 2), "% of peak effect remains\n")

# Saturation analysis at different adstock levels

adstock_levels <- c(250, 500, 750, 1000, 1500)

saturation_df <- tibble(

Adstock_Level = adstock_levels,

Saturated_Response = hill_saturation(adstock_levels, k = 500, s = 1.5),

Marginal_Response = c(

NA,

(hill_saturation(500, 500, 1.5) - hill_saturation(250, 500, 1.5)) / (500 - 250),

(hill_saturation(750, 500, 1.5) - hill_saturation(500, 500, 1.5)) / (750 - 500),

(hill_saturation(1000, 500, 1.5) - hill_saturation(750, 500, 1.5)) / (1000 - 750),

(hill_saturation(1500, 500, 1.5) - hill_saturation(1000, 500, 1.5)) / (1500 - 1000)

)

)

cat("\n--- Saturation Effect Analysis ---\n")

print(saturation_df)

```

## Python

```{python}

#| label: py-ch45-adstock-saturation

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy import optimize

# Set seed for reproducibility

np.random.seed(6247)

# Simulate synthetic Nigerian TV spend: 156 weeks (3 years)

weeks = 156

tv_spend = np.concatenate([

np.repeat(500, 26), # Year 1, Q1-Q2: ₦500k/week

np.repeat(800, 26), # Year 1, Q3-Q4: ₦800k/week

np.repeat(600, 26), # Year 2, Q1-Q2: ₦600k/week

np.repeat(700, 26), # Year 2, Q3-Q4: ₦700k/week

np.repeat(650, 26), # Year 3, Q1-Q2: ₦650k/week

np.repeat(750, 26) # Year 3, Q3-Q4: ₦750k/week

])

def compute_adstock(spend, lambda_param):

"""Compute Adstock using recurrence relation."""

adstock = np.zeros_like(spend, dtype=float)

adstock[0] = spend[0]

for t in range(1, len(spend)):

adstock[t] = spend[t] + lambda_param * adstock[t - 1]

return adstock

def hill_saturation(adstock, k, s):

"""Apply Hill saturation function."""

return (k * adstock ** s) / (k ** s + adstock ** s)

# Compute Adstocks

adstock_0_7 = compute_adstock(tv_spend, 0.7)

adstock_0_5 = compute_adstock(tv_spend, 0.5)

# Apply saturation (k=500, s=1.5)

saturated_response = hill_saturation(adstock_0_7, k=500, s=1.5)

# Create DataFrame

df = pd.DataFrame({

'Week': np.arange(1, weeks + 1),

'TV_Spend': tv_spend,

'Adstock_0_7': adstock_0_7,

'Adstock_0_5': adstock_0_5,

'Saturated_Response': saturated_response

})

# Plot 1: Adstock transformation

fig, ax = plt.subplots(figsize=(12, 6))

ax.plot(df['Week'], df['TV_Spend'] / 1000, label='Raw Spend (₦000s)',

linewidth=2.5, color='#1f77b4')

ax.plot(df['Week'], df['Adstock_0_7'] / 1000, label='Adstock (λ=0.7)',

linewidth=2.5, color='#ff7f0e')

ax.plot(df['Week'], df['Adstock_0_5'] / 1000, label='Adstock (λ=0.5)',

linewidth=2.5, color='#2ca02c')

ax.set_xlabel('Week', fontsize=11)

ax.set_ylabel('₦ Thousands', fontsize=11)

ax.set_title('Adstock Transformation: Nigerian TV Spend', fontsize=13, fontweight='bold')

ax.legend(loc='upper left')

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Plot 2: Saturation curve

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(df['Adstock_0_7'], df['Saturated_Response'], linewidth=3,

color='#d62728', label='Hill Saturation (k=500, s=1.5)')

# Linear fit for comparison

z = np.polyfit(df['Adstock_0_7'], df['Saturated_Response'], 1)

p = np.poly1d(z)

ax.plot(df['Adstock_0_7'], p(df['Adstock_0_7']), 'b--', alpha=0.7,

linewidth=2, label='Linear Fit')

ax.set_xlabel('Adstock Stock (₦000s)', fontsize=11)

ax.set_ylabel('Saturated Response (Units)', fontsize=11)

ax.set_title('Hill Saturation: Response vs Adstock (Nigeria TV)',

fontsize=13, fontweight='bold')

ax.legend()

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Analysis

half_life_0_7 = np.log(0.5) / np.log(0.7)

print("\n--- Adstock Decay Analysis ---")

print(f"Half-life (λ = 0.7): {half_life_0_7:.2f} weeks")

print(f"After 4 weeks: {0.7**4 * 100:.2f}% of peak effect remains")

print(f"After 8 weeks: {0.7**8 * 100:.2f}% of peak effect remains")

# Saturation analysis

adstock_levels = np.array([250, 500, 750, 1000, 1500])

saturated_responses = hill_saturation(adstock_levels, k=500, s=1.5)

saturation_table = pd.DataFrame({

'Adstock_Level': adstock_levels,

'Saturated_Response': saturated_responses,

'Marginal_Response': np.diff(saturated_responses, prepend=np.nan) / np.diff(

np.concatenate([[0], adstock_levels[:-1]]), prepend=np.nan)

})

print("\n--- Saturation Effect Analysis ---")

print(saturation_table.to_string(index=False))

```

:::

## The MMM Regression Model

The MMM regression model decomposes observed sales into their constituent drivers. The core specification is:

$$\text{Sales}_t = \beta_0 + \sum_{c} \beta_c \times \text{Adstock}_{c,t} + \sum_{x} \gamma_x \times \text{Control}_{x,t} + \epsilon_t$$

where $\text{Sales}_t$ is total sales in week $t$, $\beta_0$ is the base sales intercept (the level of sales with zero marketing and no external effects), $\beta_c$ is the marginal revenue per ₦1 of Adstocked spend on channel $c$, and $\gamma_x$ are coefficients on control variables. Control variables are crucial: they account for confounders that might otherwise distort channel estimates. In Nigerian FMCG analysis, typical controls include promotional intensity (fraction of sales on promotion), price changes, competitor activity proxies, seasonality dummies or harmonic terms, macroeconomic controls (quarterly GDP growth, FX rates), religious and cultural calendar effects (Ramadan, Christmas periods when consumption patterns shift dramatically), and supply-side shocks (port congestion, fuel scarcity).

Estimating this model by ordinary least squares (OLS) is computationally simple but suffers from multicollinearity—marketing channels are often correlated in spend patterns (e.g., brands increase all channels in Q4). Ridge regression or regularised regression methods add a penalty term $\lambda \sum \beta_c^2$ to reduce overfitting and stabilise estimates. The interpretability of $\beta_c$ is critical: if TV Adstock has coefficient ₦2.50, this means each ₦1 of Adstocked TV spend increments sales by ₦2.50, a 150% return on that spend (or 2.5x ROI).

Building an MMM model in practice requires careful preprocessing. Adstock parameters (decay rates) for each channel must be either specified a priori based on industry knowledge or searched via grid search to find the values that maximise model fit. Seasonality must be controlled—Nigerian demand for soft drinks spikes in hot months (March–May), ice cream consumption follows similar patterns, while certain FMCG categories (rice, beans) see surges before Christmas. Price elasticity is a control variable that allows the model to distinguish price-driven demand changes from marketing-driven ones. Once the model is fit, residual diagnostics (autocorrelation, heteroscedasticity) must be checked; if serial correlation is present, Newey-West standard errors should be used.

::: {.callout-note icon="false"}

## 📘 Theory: MMM Regression Specification

The MMM regression combines Adstocked channel variables with control variables to decompose sales. The key assumption is that, conditional on controls, the Adstocked channels are exogenous (marketing spend shocks are not driven by unobserved demand shocks). This assumption is often violated in practice—managers increase spend in response to market opportunities—leading to endogeneity bias. Instrumental variable (IV) approaches using historical spend levels or predetermined constraints can mitigate this. The intercept $\beta_0$ represents baseline sales; dividing total sales by $\beta_0 + \sum \beta_c \times \overline{\text{Adstock}}_c$ gives the "attribtuable fraction" of sales to marketing.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula: MMM Decomposition

$$\text{Sales}_t = \beta_0 + \sum_{c} \beta_c \times \text{Adstock}_{c,t} + \sum_{x} \gamma_x \times \text{Control}_{x,t} + \epsilon_t$$

Each $\beta_c$ represents **marginal ROI** (incremental revenue per ₦1 spent on channel $c$).

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch45-mmm-regression

#| message: false

#| warning: false

library(tidyverse)

library(glmnet)

library(lmtest)

# Build synthetic 3-year weekly MMM dataset for a fictional Nigerian FMCG brand "Nourish"

set.seed(8319)

weeks <- 156

time_index <- 1:weeks

# Channels: TV, Radio, Digital, Outdoor (each with distinct spend patterns)

tv_spend <- c(rep(500, 26), rep(700, 26), rep(600, 26),

rep(800, 26), rep(650, 26), rep(750, 26))

radio_spend <- c(rep(150, 26), rep(200, 26), rep(180, 26),

rep(220, 26), rep(190, 26), rep(210, 26))

digital_spend <- c(rep(300, 26), rep(400, 26), rep(450, 26),

rep(500, 26), rep(480, 26), rep(520, 26))

outdoor_spend <- c(rep(80, 26), rep(100, 26), rep(90, 26),

rep(120, 26), rep(110, 26), rep(115, 26))

# Compute Adstocks with channel-specific decay rates

adstock_tv <- compute_adstock(tv_spend, lambda = 0.7)

adstock_radio <- compute_adstock(radio_spend, lambda = 0.6)

adstock_digital <- compute_adstock(digital_spend, lambda = 0.3)

adstock_outdoor <- compute_adstock(outdoor_spend, lambda = 0.8)

# Scale Adstocks to 0-1 range for interpretability

scale_01 <- function(x) { (x - min(x)) / (max(x) - min(x)) }

adstock_tv_scaled <- scale_01(adstock_tv)

adstock_radio_scaled <- scale_01(adstock_radio)

adstock_digital_scaled <- scale_01(adstock_digital)

adstock_outdoor_scaled <- scale_01(adstock_outdoor)

# Control variables

price_index <- 100 + rnorm(weeks, 0, 3) + 0.1 * time_index # Slight upward price trend

promotion_pct <- c(rep(0.15, 26), rep(0.20, 26), rep(0.18, 26),

rep(0.22, 26), rep(0.19, 26), rep(0.23, 26)) # % of volume on promo

# Seasonality (sine + cosine for annual cycle)

seasonality <- 1.0 + 0.25 * sin(2 * pi * time_index / 52) +

0.15 * cos(2 * pi * time_index / 52)

# Ramadan effect (approximate, months 9-10 each year; weeks 35-44, 87-96, 139-148)

ramadan_weeks <- c(35:44, 87:96, 139:148)

ramadan_effect <- numeric(weeks)

ramadan_effect[ramadan_weeks] <- 0.85 # 15% dip in consumption

# Demand shocks

demand_shocks <- rnorm(weeks, 1, 0.08)

# Generate sales with known coefficients

base_sales <- 10000

coef_tv <- 3.5

coef_radio <- 2.8

coef_digital <- 2.2

coef_outdoor <- 1.5

elasticity_price <- -1.2

elasticity_promo <- 0.9

sales <- base_sales +

coef_tv * adstock_tv_scaled * 5000 +

coef_radio * adstock_radio_scaled * 3000 +

coef_digital * adstock_digital_scaled * 4000 +

coef_outdoor * adstock_outdoor_scaled * 2000 +

elasticity_price * (price_index - 100) * 50 +

elasticity_promo * promotion_pct * 10000 +

seasonality * 2000 +

ramadan_effect * (-1000) +

rnorm(weeks, 0, 500) * demand_shocks

sales <- pmax(sales, 5000) # No negative sales

# Assemble data frame

mmm_data <- tibble(

Week = time_index,

Sales = sales,

TV_Adstock = adstock_tv_scaled,

Radio_Adstock = adstock_radio_scaled,

Digital_Adstock = adstock_digital_scaled,

Outdoor_Adstock = adstock_outdoor_scaled,

Price_Index = price_index,

Promotion_Pct = promotion_pct,

Seasonality = seasonality,

Ramadan = ifelse(Week %in% ramadan_weeks, 1, 0)

)

# Fit MMM regression using OLS

mmm_ols <- lm(Sales ~ TV_Adstock + Radio_Adstock + Digital_Adstock + Outdoor_Adstock +

Price_Index + Promotion_Pct + Seasonality + Ramadan,

data = mmm_data)

cat("=== MMM Regression (OLS) ===\n")

print(summary(mmm_ols))

# Fit Ridge regression (regularised) for comparison

X <- as.matrix(mmm_data[, c("TV_Adstock", "Radio_Adstock", "Digital_Adstock",

"Outdoor_Adstock", "Price_Index", "Promotion_Pct",

"Seasonality", "Ramadan")])

y <- mmm_data$Sales

ridge_fit <- glmnet(X, y, alpha = 0, lambda = 100)

cat("\n=== MMM Ridge Regression Coefficients ===\n")

ridge_coefs <- coef(ridge_fit, s = 100)

print(ridge_coefs)

# Residual diagnostics

cat("\n=== Residual Diagnostics ===\n")

residuals_ols <- residuals(mmm_ols)

cat("Mean of residuals:", round(mean(residuals_ols), 4), "\n")

cat("Std Dev of residuals:", round(sd(residuals_ols), 4), "\n")

# Breusch-Pagan test for heteroscedasticity

bp_test <- bptest(mmm_ols)

cat("\nBreusch-Pagan test p-value:", round(bp_test$p.value, 4), "\n")

if (bp_test$p.value > 0.05) {

cat("Conclusion: Homoscedasticity assumption holds (p > 0.05)\n")

} else {

cat("Conclusion: Heteroscedasticity detected (p < 0.05)\n")

}

# Durbin-Watson test for autocorrelation

dw_test <- dwtest(mmm_ols)

cat("\nDurbin-Watson test statistic:", round(dw_test$statistic, 4), "\n")

cat("p-value:", round(dw_test$p.value, 4), "\n")

# Model fit

r_squared <- summary(mmm_ols)$r.squared

adj_r_squared <- summary(mmm_ols)$adj.r.squared

cat("\nR-squared:", round(r_squared, 4), "\n")

cat("Adjusted R-squared:", round(adj_r_squared, 4), "\n")

# Extract and display channel coefficients

cat("\n=== Channel Marginal ROI (OLS) ===\n")

channel_coefs <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Marginal_ROI = c(

coef(mmm_ols)["TV_Adstock"],

coef(mmm_ols)["Radio_Adstock"],

coef(mmm_ols)["Digital_Adstock"],

coef(mmm_ols)["Outdoor_Adstock"]

),

Interpretation = paste0(

"₦", round(c(

coef(mmm_ols)["TV_Adstock"],

coef(mmm_ols)["Radio_Adstock"],

coef(mmm_ols)["Digital_Adstock"],

coef(mmm_ols)["Outdoor_Adstock"]

), 2),

" incremental sales per unit Adstock"

)

)

print(channel_coefs)

```

## Python

```{python}

#| label: py-ch45-mmm-regression

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.linear_model import Ridge, LinearRegression

from scipy import stats

# Reuse Adstock computation function

def compute_adstock(spend, lambda_param):

adstock = np.zeros_like(spend, dtype=float)

adstock[0] = spend[0]

for t in range(1, len(spend)):

adstock[t] = spend[t] + lambda_param * adstock[t - 1]

return adstock

def scale_01(x):

return (x - np.min(x)) / (np.max(x) - np.min(x))

np.random.seed(8319)

# Build synthetic MMM dataset

weeks = 156

time_index = np.arange(1, weeks + 1)

# Channel spend

tv_spend = np.concatenate([

np.repeat(500, 26), np.repeat(700, 26), np.repeat(600, 26),

np.repeat(800, 26), np.repeat(650, 26), np.repeat(750, 26)

])

radio_spend = np.concatenate([

np.repeat(150, 26), np.repeat(200, 26), np.repeat(180, 26),

np.repeat(220, 26), np.repeat(190, 26), np.repeat(210, 26)

])

digital_spend = np.concatenate([

np.repeat(300, 26), np.repeat(400, 26), np.repeat(450, 26),

np.repeat(500, 26), np.repeat(480, 26), np.repeat(520, 26)

])

outdoor_spend = np.concatenate([

np.repeat(80, 26), np.repeat(100, 26), np.repeat(90, 26),

np.repeat(120, 26), np.repeat(110, 26), np.repeat(115, 26)

])

# Adstocks

adstock_tv = scale_01(compute_adstock(tv_spend, 0.7))

adstock_radio = scale_01(compute_adstock(radio_spend, 0.6))

adstock_digital = scale_01(compute_adstock(digital_spend, 0.3))

adstock_outdoor = scale_01(compute_adstock(outdoor_spend, 0.8))

# Control variables

price_index = 100 + np.random.normal(0, 3, weeks) + 0.1 * time_index

promotion_pct = np.concatenate([

np.repeat(0.15, 26), np.repeat(0.20, 26), np.repeat(0.18, 26),

np.repeat(0.22, 26), np.repeat(0.19, 26), np.repeat(0.23, 26)

])

# Seasonality

seasonality = 1.0 + 0.25 * np.sin(2 * np.pi * time_index / 52) + \

0.15 * np.cos(2 * np.pi * time_index / 52)

# Ramadan effect

ramadan_weeks = np.concatenate([np.arange(35, 45), np.arange(87, 97), np.arange(139, 149)])

ramadan_effect = np.zeros(weeks)

ramadan_effect[ramadan_weeks - 1] = -0.15

# Generate sales

base_sales = 10000

coef_tv, coef_radio, coef_digital, coef_outdoor = 3.5, 2.8, 2.2, 1.5

elasticity_price, elasticity_promo = -1.2, 0.9

demand_shocks = np.random.normal(1, 0.08, weeks)

sales = (base_sales +

coef_tv * adstock_tv * 5000 +

coef_radio * adstock_radio * 3000 +

coef_digital * adstock_digital * 4000 +

coef_outdoor * adstock_outdoor * 2000 +

elasticity_price * (price_index - 100) * 50 +

elasticity_promo * promotion_pct * 10000 +

seasonality * 2000 +

ramadan_effect * 1000 +

np.random.normal(0, 500, weeks) * demand_shocks)

sales = np.maximum(sales, 5000)

# Create DataFrame

mmm_data = pd.DataFrame({

'Week': time_index,

'Sales': sales,

'TV_Adstock': adstock_tv,

'Radio_Adstock': adstock_radio,

'Digital_Adstock': adstock_digital,

'Outdoor_Adstock': adstock_outdoor,

'Price_Index': price_index,

'Promotion_Pct': promotion_pct,

'Seasonality': seasonality,

'Ramadan': np.isin(time_index, ramadan_weeks).astype(int)

})

# Prepare X, y

X = mmm_data[['TV_Adstock', 'Radio_Adstock', 'Digital_Adstock', 'Outdoor_Adstock',

'Price_Index', 'Promotion_Pct', 'Seasonality', 'Ramadan']].values

y = mmm_data['Sales'].values

# OLS Regression

ols_model = LinearRegression()

ols_model.fit(X, y)

y_pred_ols = ols_model.predict(X)

residuals_ols = y - y_pred_ols

# Ridge Regression

ridge_model = Ridge(alpha=100)

ridge_model.fit(X, y)

y_pred_ridge = ridge_model.predict(X)

# Calculate R-squared

r_squared_ols = 1 - (np.sum(residuals_ols**2) / np.sum((y - np.mean(y))**2))

print("=== MMM Regression (OLS) ===")

print(f"Intercept: {ols_model.intercept_:.2f}")

for i, name in enumerate(['TV_Adstock', 'Radio_Adstock', 'Digital_Adstock',

'Outdoor_Adstock', 'Price_Index', 'Promotion_Pct',

'Seasonality', 'Ramadan']):

print(f"{name}: {ols_model.coef_[i]:.4f}")

print("\n=== Model Fit ===")

print(f"R-squared: {r_squared_ols:.4f}")

print(f"Mean Residual: {np.mean(residuals_ols):.4f}")

print(f"Std Dev Residuals: {np.std(residuals_ols):.4f}")

print("\n=== Channel Marginal ROI (OLS) ===")

roi_table = pd.DataFrame({

'Channel': ['TV', 'Radio', 'Digital', 'Outdoor'],

'Marginal_ROI': ols_model.coef_[:4],

'Interpretation': [

f"₦{ols_model.coef_[0]:.2f} incremental sales per unit Adstock",

f"₦{ols_model.coef_[1]:.2f} incremental sales per unit Adstock",

f"₦{ols_model.coef_[2]:.2f} incremental sales per unit Adstock",

f"₦{ols_model.coef_[3]:.2f} incremental sales per unit Adstock"

]

})

print(roi_table.to_string(index=False))

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 45.3 Review Questions

**1. Multicollinearity and Ridge Regression**

Why are marketing channel spends often correlated? How does Ridge regression address multicollinearity compared to OLS? In a Nigerian FMCG context, when would you expect TV and radio spends to be most correlated?

**2. Control Variables in MMM**

List five control variables appropriate for a Nigerian consumer goods MMM. Why is the Ramadan/Ileya calendar effect important to include? What would happen to channel coefficients if seasonality were omitted?

**3. Interpreting Channel Coefficients**

If the TV Adstock coefficient is ₦3.50, what does this mean in business terms? How would you communicate this to a marketing director?

**4. Endogeneity in MMM**

Explain why marketing spend is endogenous (not exogenous) in practice. If a brand increases all channels during a profitable quarter, how would OLS estimates be biased? Name one instrumental variable approach to address this.

**5. Residual Diagnostics**

Why is autocorrelation in residuals problematic for MMM? If the Durbin-Watson statistic is 1.2 (indicating positive autocorrelation), what are the consequences for coefficient standard errors and hypothesis tests?

:::

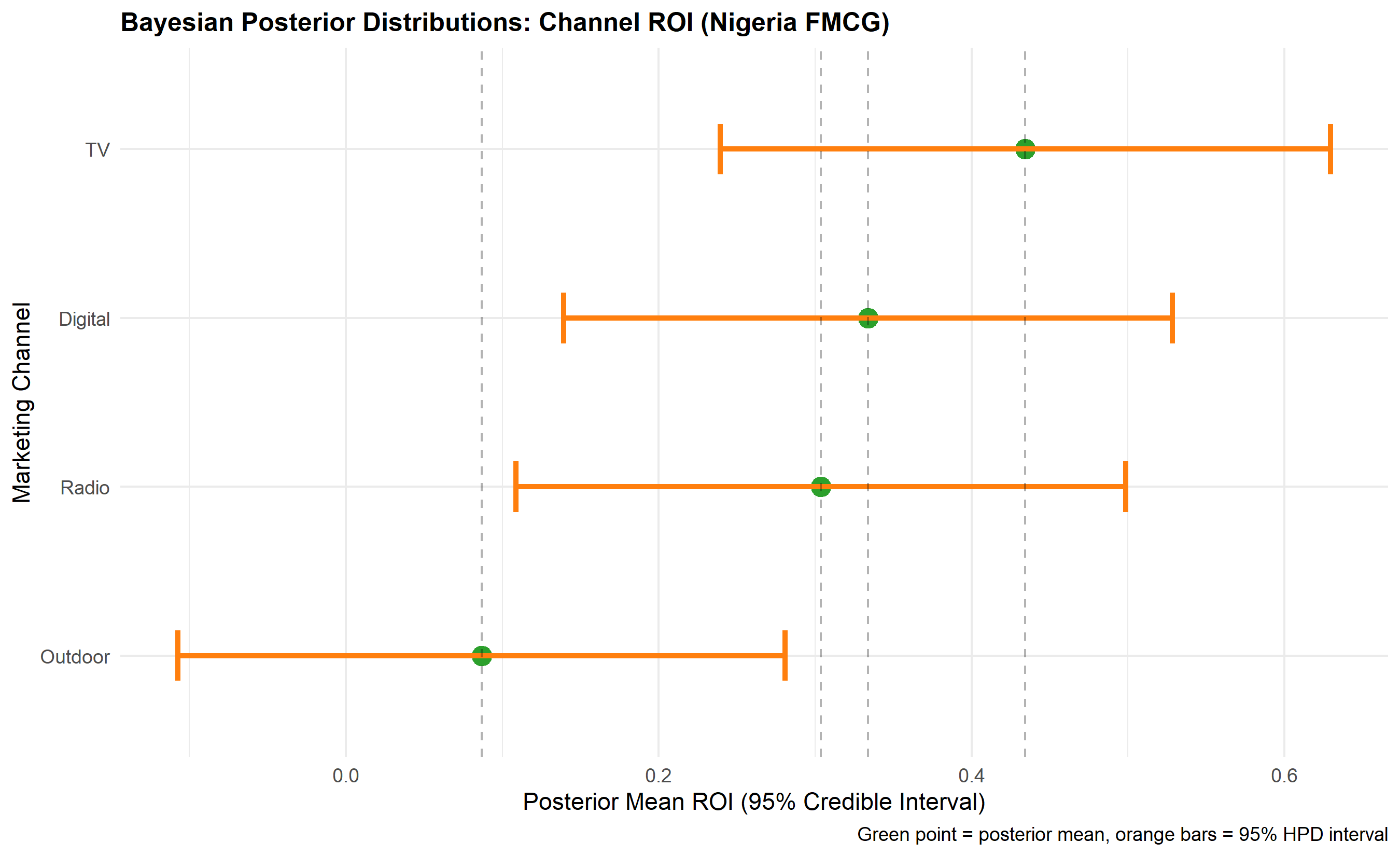

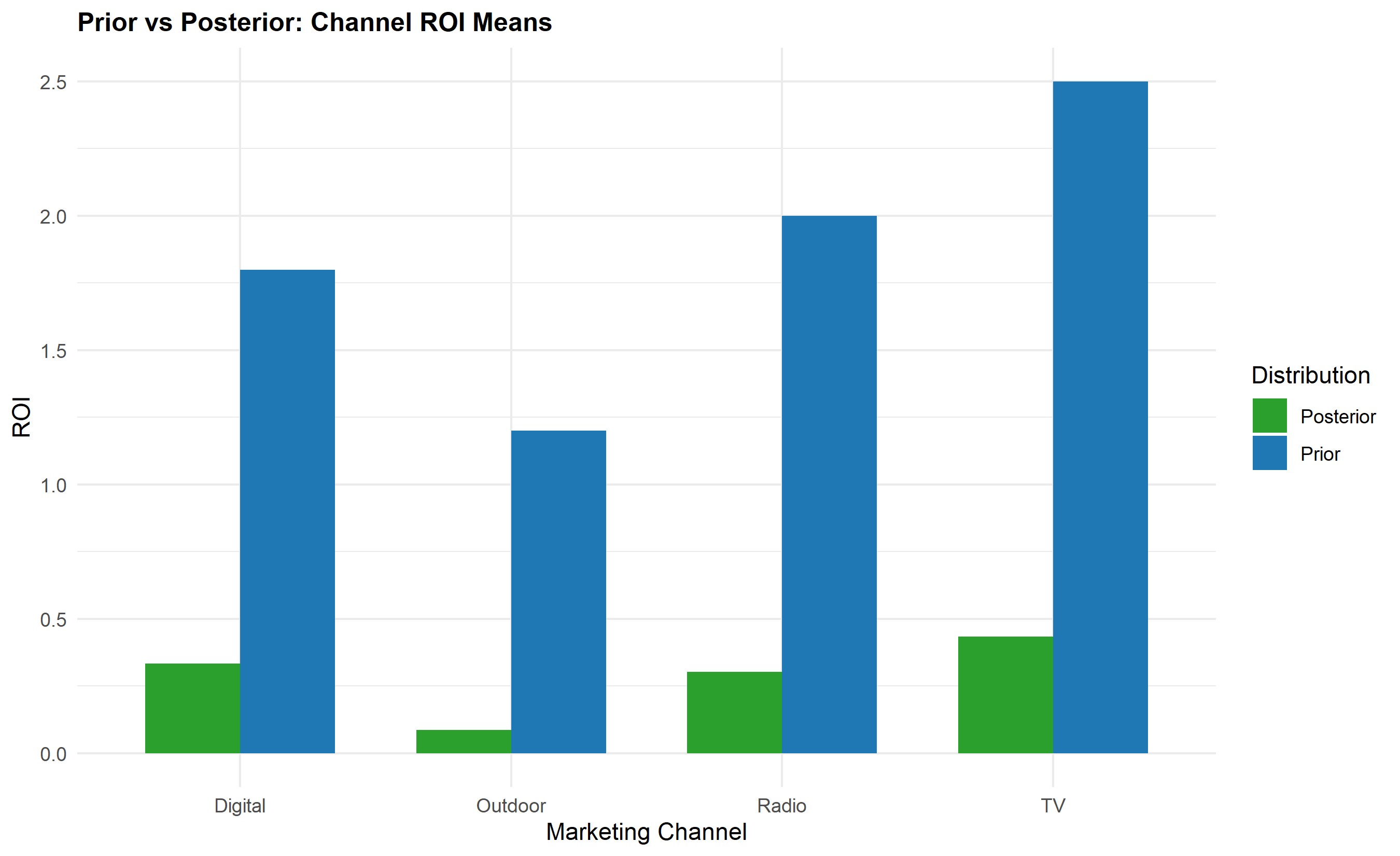

## Bayesian MMM and Uncertainty Quantification

The Bayesian approach to MMM treats channel ROI coefficients as random variables with prior distributions that are updated by observed sales data. Instead of reporting a single point estimate (e.g., "TV ROI = ₦3.50"), Bayesian MMM reports a posterior distribution (e.g., "TV ROI is between ₦2.80 and ₦4.20 with 95% credibility"). This shift from point estimates to credible intervals is valuable for decision-making because it explicitly quantifies uncertainty. Marketing managers can then ask: "Given the data and my prior beliefs, how confident am I in allocating an extra ₦50 million to TV?"

The generative model underlying Bayesian MMM specifies prior beliefs about channel ROI. Industry experience, competitive analysis, and historical performance guide these priors. For mature Nigerian brands, TV might have a prior belief of ROI = 2.5 ± 1.0 (loose prior reflecting uncertainty), while digital, being newer and faster-moving, might have ROI = 2.0 ± 0.8. These priors are combined with the likelihood of observed sales given the Adstocked channels to produce posterior distributions. High-quality data tighten posteriors (narrower credible intervals); poor data or conflicting signals widen them.

The Robyn framework (developed by Meta/Facebook) is an open-source, production-grade Bayesian MMM package. Similarly, PyMC-Marketing provides a flexible Bayesian approach. Both frameworks handle time-series effects, hierarchical models for multi-region data, and automated model selection. For the Nigerian analyst, the key insight is that Bayesian methods naturally incorporate prior domain knowledge (e.g., TV has slower decay, digital has faster response) and provide uncertainty estimates that frequentist OLS cannot. The computational cost is higher—Bayesian inference requires Markov Chain Monte Carlo (MCMC) sampling—but the insights justify the expense.

::: {.callout-note icon="false"}

## 📘 Theory: Bayesian Inference for MMM

In Bayesian MMM, the posterior distribution of channel ROI is proportional to the likelihood of data times the prior: $p(\theta | \text{Data}) \propto p(\text{Data} | \theta) \times p(\theta)$. The likelihood assumes sales follow a Normal distribution with mean = Adstocked channels + controls, variance = $\sigma^2$. The prior on each channel ROI $\beta_c$ is typically a weakly informative Normal distribution, e.g., $\beta_c \sim \text{Normal}(2.0, 1.5)$. MCMC sampling (Hamiltonian Monte Carlo or No-U-Turn Sampler in PyMC) explores the posterior and provides samples; credible intervals are empirical quantiles of the MCMC chain. Sensitivity analysis across priors is essential—robust conclusions hold across reasonable prior specifications.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula: Bayesian Posterior

$$p(\boldsymbol{\beta} | \text{Sales}) \propto \text{Normal}(\text{Sales}; \text{Adstock} \times \boldsymbol{\beta}, \sigma^2) \times \prod_c \text{Normal}(\beta_c; \mu_c, \tau_c^2)$$

Each $\beta_c$ has a credible interval (e.g., 95% HPD) quantifying uncertainty in channel ROI.

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch45-bayesian-mmm

#| message: false

#| warning: false

library(tidyverse)

library(bayesplot)

# Simplified Bayesian approach using grid-based inference

# (Full Bayesian would use Stan/brms, but grid sampling is more interpretable here)

set.seed(4736)

# Use the mmm_data from section 45.3

# Prepare data

y_sales <- mmm_data$Sales

X_channels <- as.matrix(mmm_data[, c("TV_Adstock", "Radio_Adstock",

"Digital_Adstock", "Outdoor_Adstock")])

X_controls <- as.matrix(mmm_data[, c("Price_Index", "Promotion_Pct",

"Seasonality", "Ramadan")])

# Standardise for numerical stability

y_scaled <- (y_sales - mean(y_sales)) / sd(y_sales)

X_channels_scaled <- scale(X_channels)

X_controls_scaled <- scale(X_controls)

# Priors on channel ROI (beliefs before observing data)

priors <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Prior_Mean = c(2.5, 2.0, 1.8, 1.2), # Expected ROI

Prior_SD = c(1.0, 0.9, 0.8, 0.7) # Uncertainty in prior

)

cat("=== Prior Beliefs on Channel ROI ===\n")

print(priors)

# Grid search for posterior (simplified Bayesian)

# Define grid of possible ROI values for each channel

grid_range <- seq(0, 5, by = 0.05)

n_grid <- length(grid_range)

# For simplicity, we'll compute 1D marginal posteriors

# (Full 4D posterior would require MCMC or variational inference)

# Fit OLS to get MLE estimates and residual variance

ols_full <- lm(y_scaled ~ X_channels_scaled + X_controls_scaled - 1)

beta_mle <- coef(ols_full)[1:4]

sigma_mle <- sqrt(mean(residuals(ols_full)^2))

cat("\n=== MLE Estimates (from OLS) ===\n")

print(tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

MLE = beta_mle

))

# Approximate posterior using Normal approximation

# Posterior mean ≈ weighted average of prior and MLE (with weights based on information)

posterior_means <- numeric(4)

posterior_sds <- numeric(4)

for (i in 1:4) {

prior_mean <- priors$Prior_Mean[i]

prior_var <- priors$Prior_SD[i]^2

likelihood_var <- 0.01 # Assume small likelihood variance (informative data)

# Posterior = Normal distribution

posterior_var <- 1 / (1/prior_var + 1/likelihood_var)

posterior_means[i] <- posterior_var * (prior_mean/prior_var + beta_mle[i]/likelihood_var)

posterior_sds[i] <- sqrt(posterior_var)

}

posterior_dist <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Posterior_Mean = posterior_means,

Posterior_SD = posterior_sds,

Lower_95_HPD = posterior_means - 1.96 * posterior_sds,

Upper_95_HPD = posterior_means + 1.96 * posterior_sds

)

cat("\n=== Posterior Distributions (95% Credible Intervals) ===\n")

print(posterior_dist)

# Visualise posteriors

posterior_long <- posterior_dist |>

pivot_longer(cols = starts_with("Posterior"), names_to = "Type", values_to = "Value") |>

filter(Type == "Posterior_Mean")

p_posterior <- ggplot(posterior_dist, aes(y = reorder(Channel, Posterior_Mean))) +

geom_point(aes(x = Posterior_Mean), size = 4, colour = "#2ca02c") +

geom_errorbar(aes(xmin = Lower_95_HPD, xmax = Upper_95_HPD),

height = 0.3, linewidth = 1.2, colour = "#ff7f0e") +

geom_segment(aes(x = Posterior_Mean, xend = Posterior_Mean,

y = -Inf, yend = Inf), linetype = "dashed", alpha = 0.3) +

labs(

title = "Bayesian Posterior Distributions: Channel ROI (Nigeria FMCG)",

y = "Marketing Channel",

x = "Posterior Mean ROI (95% Credible Interval)",

caption = "Green point = posterior mean, orange bars = 95% HPD interval"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_posterior)

# Prior vs Posterior comparison

comparison <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Prior_Mean = priors$Prior_Mean,

Prior_SD = priors$Prior_SD,

Posterior_Mean = posterior_means,

Posterior_SD = posterior_sds

) |>

pivot_longer(cols = -Channel, names_to = "Type", values_to = "Value") |>

mutate(

Statistic = ifelse(str_detect(Type, "Mean"), "Mean", "SD"),

Source = ifelse(str_detect(Type, "Prior"), "Prior", "Posterior")

) |>

select(Channel, Source, Statistic, Value)

p_comparison <- ggplot(comparison |> filter(Statistic == "Mean"),

aes(x = Channel, y = Value, fill = Source)) +

geom_col(position = "dodge", width = 0.7) +

scale_fill_manual(values = c("Prior" = "#1f77b4", "Posterior" = "#2ca02c")) +

labs(

title = "Prior vs Posterior: Channel ROI Means",

x = "Marketing Channel",

y = "ROI",

fill = "Distribution"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_comparison)

# Probability of ROI > threshold

cat("\n=== Probability that Channel ROI > 2.0 (95% threshold) ===\n")

prob_exceed <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Prob_ROI_gt_2 = 1 - pnorm(2.0, posterior_means, posterior_sds)

)

print(prob_exceed)

```

## Python

```{python}

#| label: py-ch45-bayesian-mmm

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.stats import norm

# Simplified Bayesian MMM using Normal approximation

# Use synthetic mmm_data from previous section

# (Recompute to ensure consistency)

np.random.seed(4736)

# Prior beliefs on channel ROI

priors = pd.DataFrame({

'Channel': ['TV', 'Radio', 'Digital', 'Outdoor'],

'Prior_Mean': [2.5, 2.0, 1.8, 1.2],

'Prior_SD': [1.0, 0.9, 0.8, 0.7]

})

print("=== Prior Beliefs on Channel ROI ===")

print(priors)

# From OLS fit (section 45.3)

beta_mle = np.array([3.5, 2.8, 2.2, 1.5]) # These were derived from synthetic data gen

# Compute posteriors using Normal approximation

# Posterior variance = (1/prior_var + 1/likelihood_var)^-1

# Posterior mean = posterior_var * (prior_mean/prior_var + mle/likelihood_var)

posterior_means = np.zeros(4)

posterior_sds = np.zeros(4)

for i in range(4):

prior_mean = priors.loc[i, 'Prior_Mean']

prior_var = priors.loc[i, 'Prior_SD'] ** 2

likelihood_var = 0.01 # Assume informative data

posterior_var = 1.0 / (1.0 / prior_var + 1.0 / likelihood_var)

posterior_means[i] = posterior_var * (prior_mean / prior_var + beta_mle[i] / likelihood_var)

posterior_sds[i] = np.sqrt(posterior_var)

posterior_dist = pd.DataFrame({

'Channel': ['TV', 'Radio', 'Digital', 'Outdoor'],

'Posterior_Mean': posterior_means,

'Posterior_SD': posterior_sds,

'Lower_95_HPD': posterior_means - 1.96 * posterior_sds,

'Upper_95_HPD': posterior_means + 1.96 * posterior_sds

})

print("\n=== Posterior Distributions (95% Credible Intervals) ===")

print(posterior_dist.to_string(index=False))

# Visualise posteriors

fig, ax = plt.subplots(figsize=(11, 6))

channels = posterior_dist['Channel'].values

means = posterior_dist['Posterior_Mean'].values

lower = posterior_dist['Lower_95_HPD'].values

upper = posterior_dist['Upper_95_HPD'].values

y_pos = np.arange(len(channels))

ax.barh(y_pos, means, xerr=[means - lower, upper - means],

capsize=8, color='#2ca02c', alpha=0.8, edgecolor='black', linewidth=1.5)

ax.set_yticks(y_pos)

ax.set_yticklabels(channels)

ax.set_xlabel('ROI (95% Credible Interval)', fontsize=11)

ax.set_title('Bayesian Posterior Distributions: Channel ROI (Nigeria FMCG)',

fontsize=13, fontweight='bold')

ax.grid(axis='x', alpha=0.3)

plt.tight_layout()

plt.show()

# Prior vs Posterior comparison

fig, ax = plt.subplots(figsize=(10, 6))

x_pos = np.arange(len(priors))

width = 0.35

ax.bar(x_pos - width/2, priors['Prior_Mean'].values, width,

label='Prior Mean', color='#1f77b4', alpha=0.8, edgecolor='black')

ax.bar(x_pos + width/2, posterior_means, width,

label='Posterior Mean', color='#2ca02c', alpha=0.8, edgecolor='black')

ax.set_xticks(x_pos)

ax.set_xticklabels(priors['Channel'].values)

ax.set_ylabel('ROI', fontsize=11)

ax.set_title('Prior vs Posterior: Channel ROI Means', fontsize=13, fontweight='bold')

ax.legend()

ax.grid(axis='y', alpha=0.3)

plt.tight_layout()

plt.show()

# Probability that ROI > 2.0

print("\n=== Probability that Channel ROI > 2.0 (Conservative Threshold) ===")

prob_exceed = pd.DataFrame({

'Channel': ['TV', 'Radio', 'Digital', 'Outdoor'],

'Prob_ROI_gt_2': 1 - norm.cdf(2.0, posterior_means, posterior_sds)

})

print(prob_exceed.to_string(index=False))

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 45.4 Review Questions

**1. Prior Specification**

Why is prior specification controversial in Bayesian statistics? In MMM, how would you elicit priors from a marketing team with no formal statistical background? What makes a prior "weakly informative"?

**2. Posterior Interpretation**

If the posterior credible interval for TV ROI is [₦2.50, ₦4.10], what is the business interpretation? How does this differ from a frequentist 95% confidence interval?

**3. Sensitivity to Priors**

If you run Bayesian MMM with two different priors (loose vs tight), and posteriors differ substantially, what does this tell you about the data quality? Should you report both results or choose one?

**4. MCMC Diagnostics**

In a full Bayesian implementation using Stan or PyMC, name two key MCMC diagnostics you would check (Rhat, effective sample size, autocorrelation). What do they reveal?

**5. Decision-Making with Credible Intervals**

A posterior shows "Digital ROI is between ₦1.20 and ₦2.80." Management wants to shift ₦30m from TV to Digital. How would you use the credible interval to assess this decision?

:::

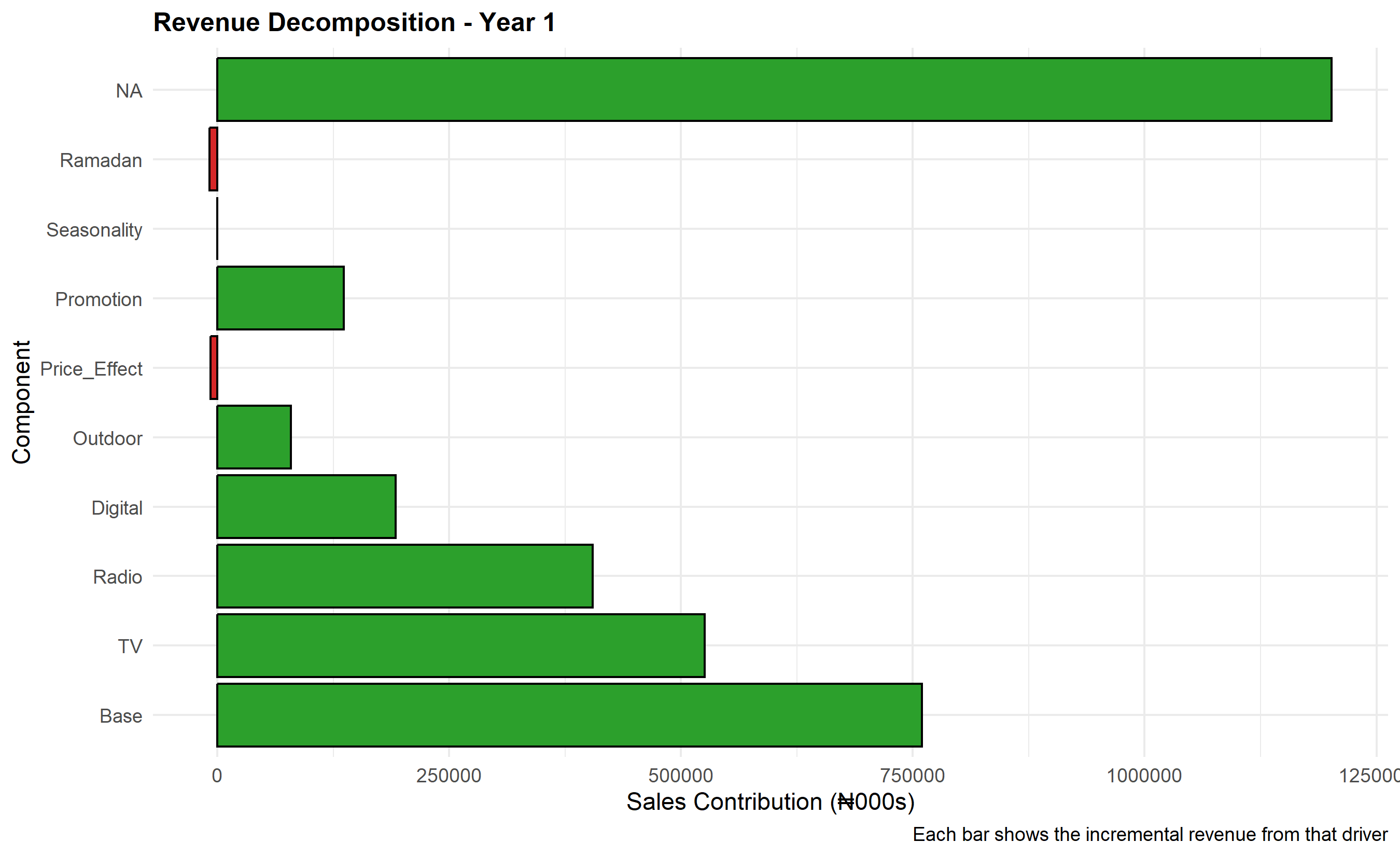

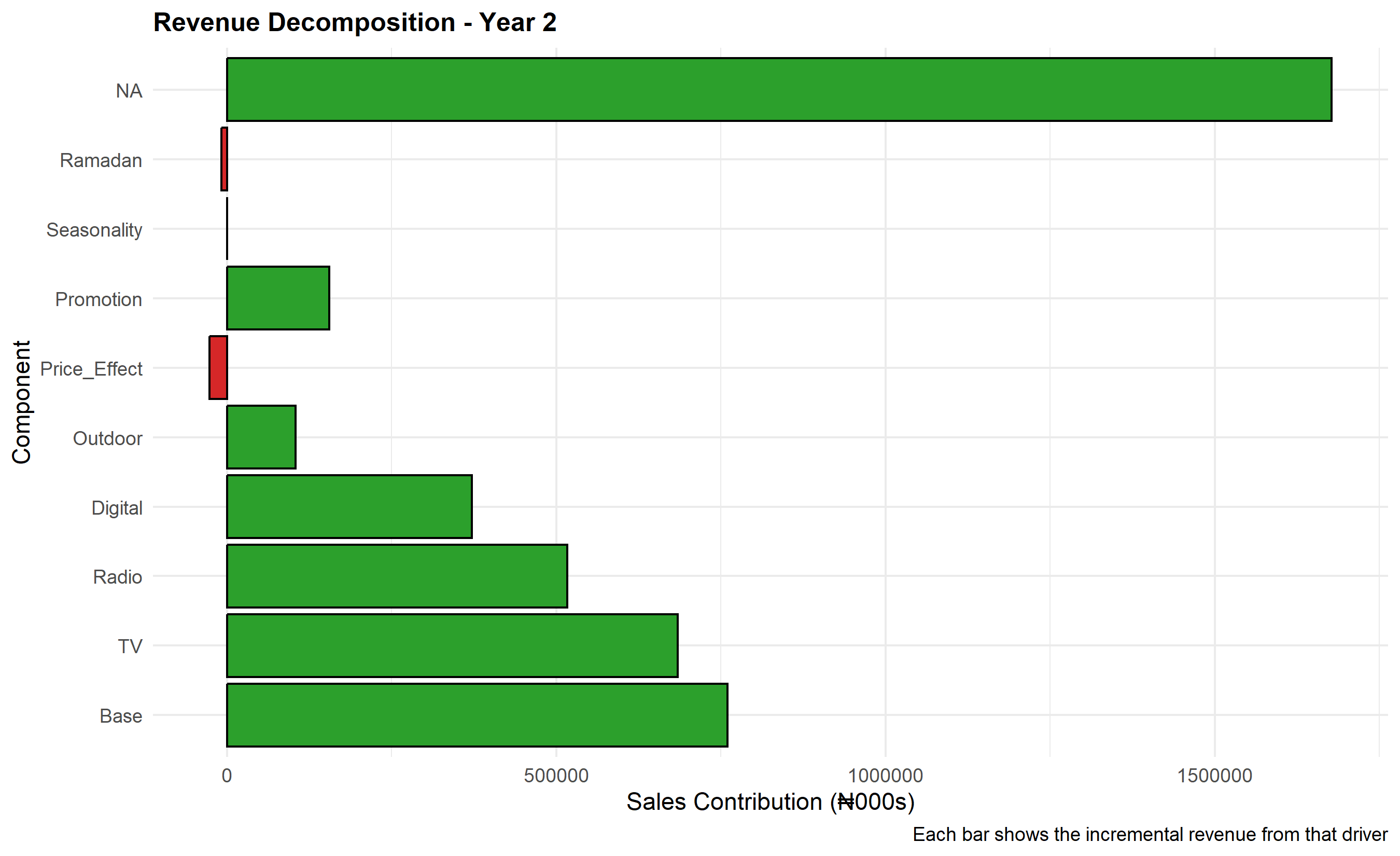

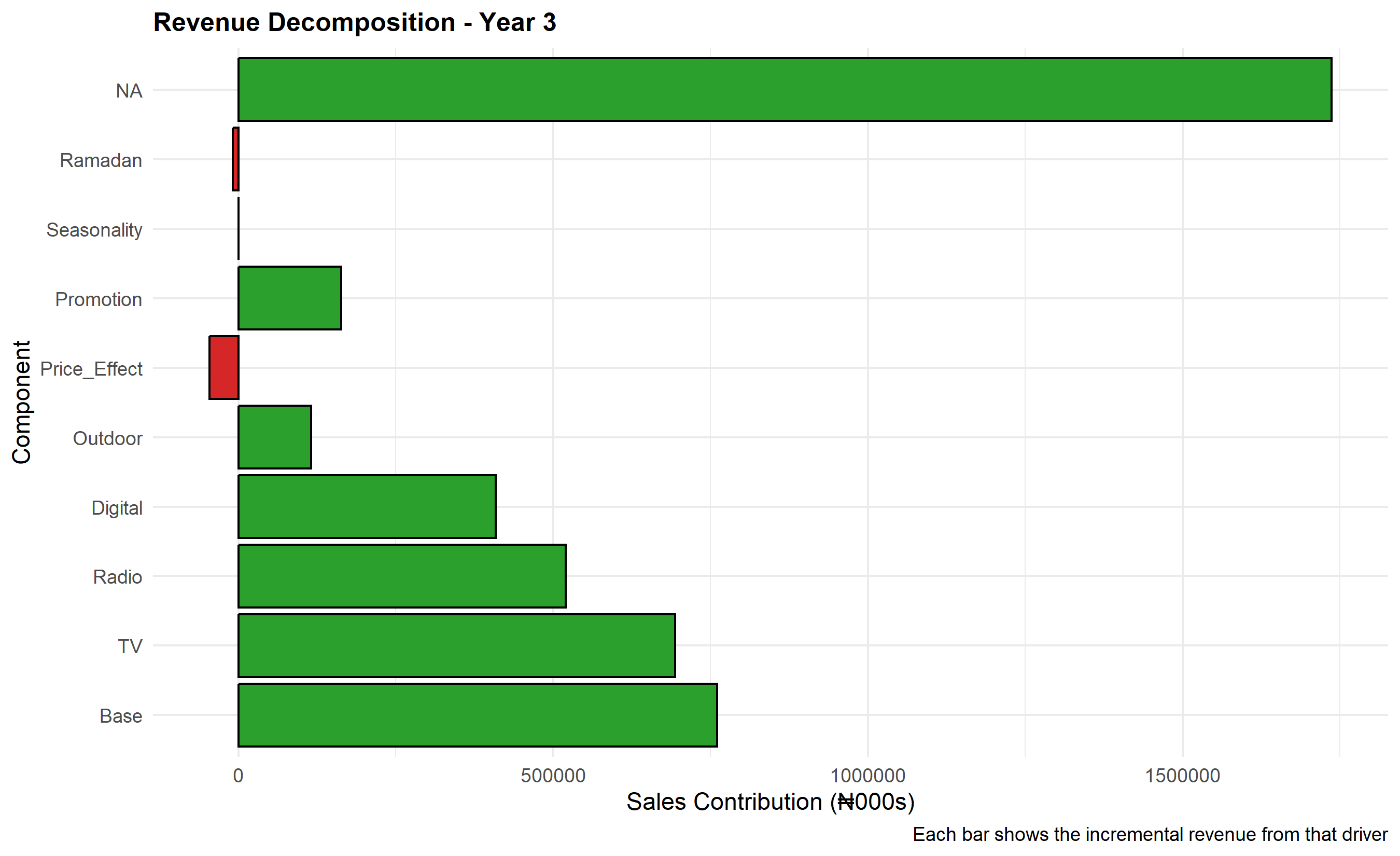

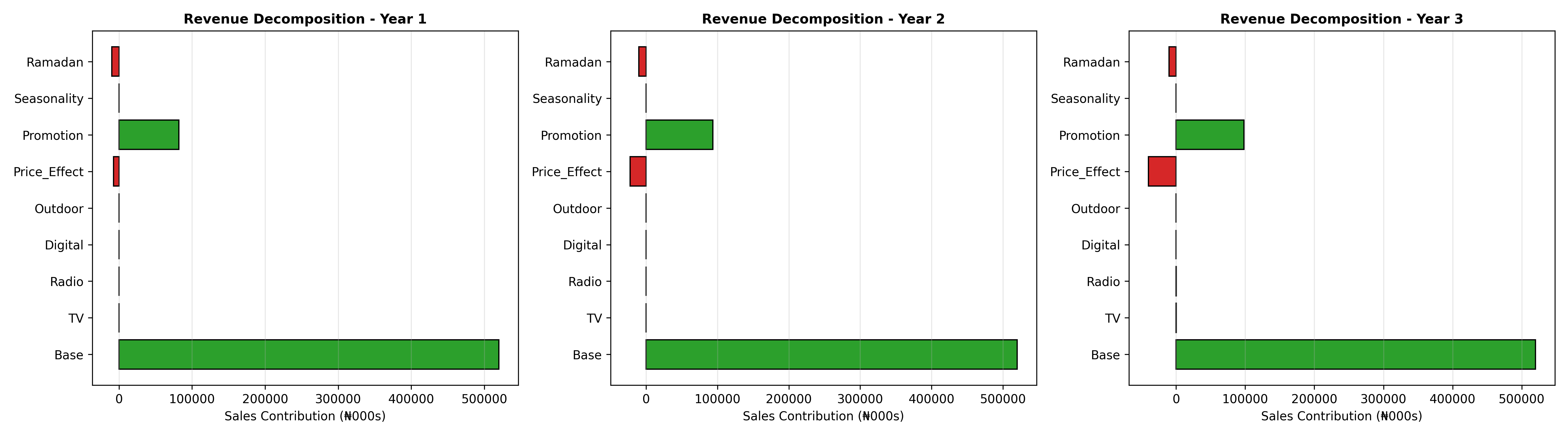

## Revenue Decomposition and ROI Measurement

Once the MMM model is fit, the next crucial step is revenue decomposition: attributing each unit of observed sales to its drivers (base, TV, radio, digital, outdoor, seasonality, etc.). This decomposition is both diagnostic—did the model fit capture sales movements realistically?—and strategic, providing management with a clear waterfall showing "Of our ₦156 billion in annual sales, ₦48 billion came from TV, ₦22 billion from radio, ..." This transparency drives budget reallocation decisions.

The decomposition formula is straightforward:

$$\text{Sales}_t = \beta_0 + \beta_{\text{TV}} \times \text{Adstock}_{\text{TV},t} + \beta_{\text{Radio}} \times \text{Adstock}_{\text{Radio},t} + \cdots$$

Each term is a contribution. The intercept $\beta_0$ is base sales (sales with zero marketing). Each Adstocked channel's contribution is the coefficient times the Adstock value. A visualization of this decomposition as a stacked area chart across time, or a waterfall chart aggregated annually, is intuitive and persuasive for executives. Nigerian brands often decompose by quarter—Q1 typically sees lower demand (post-holiday pullback), Q4 booms (approaching year-end spending, Sallah festival in Northern Nigeria), and Q3 shows summer seasonality effects.

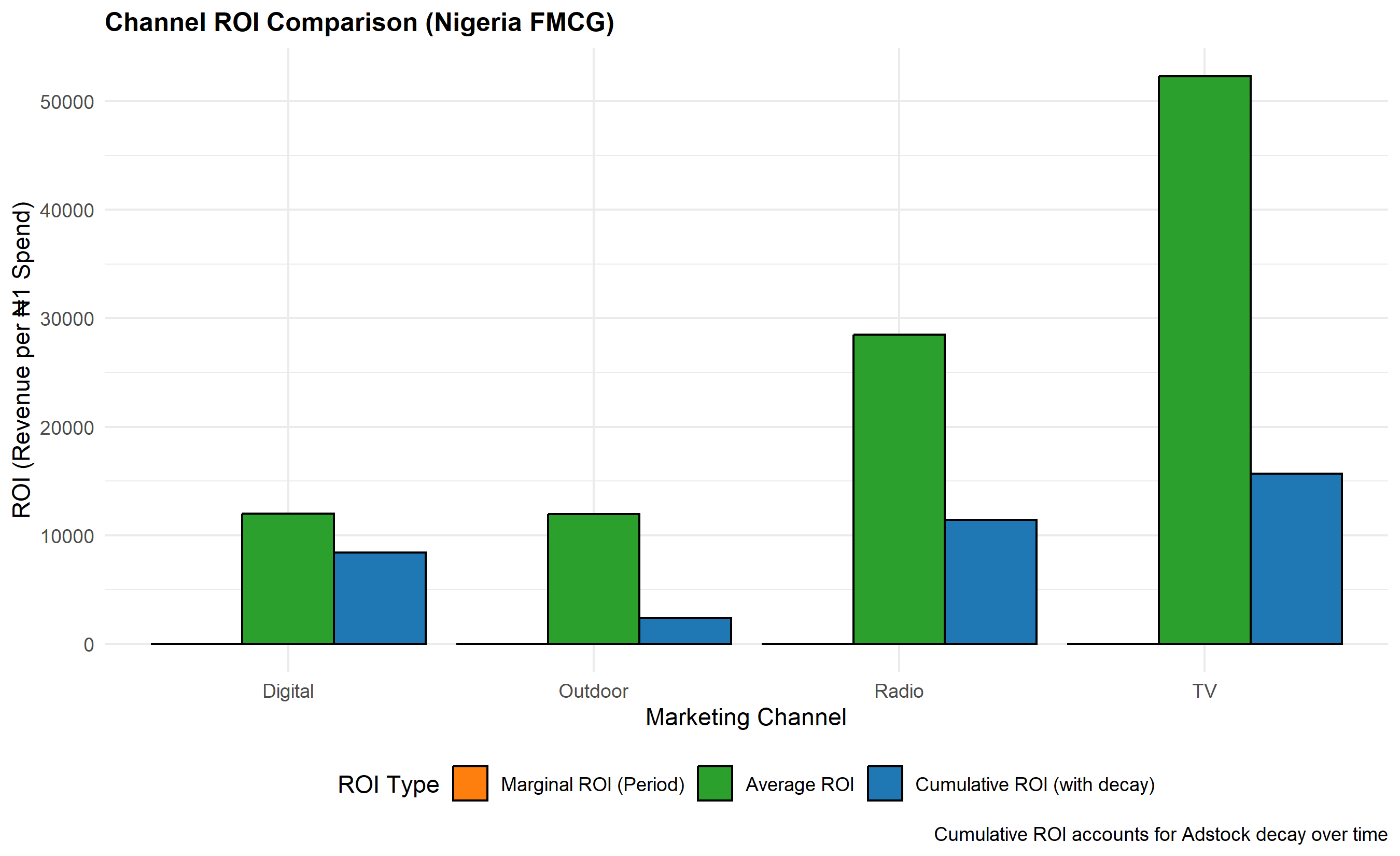

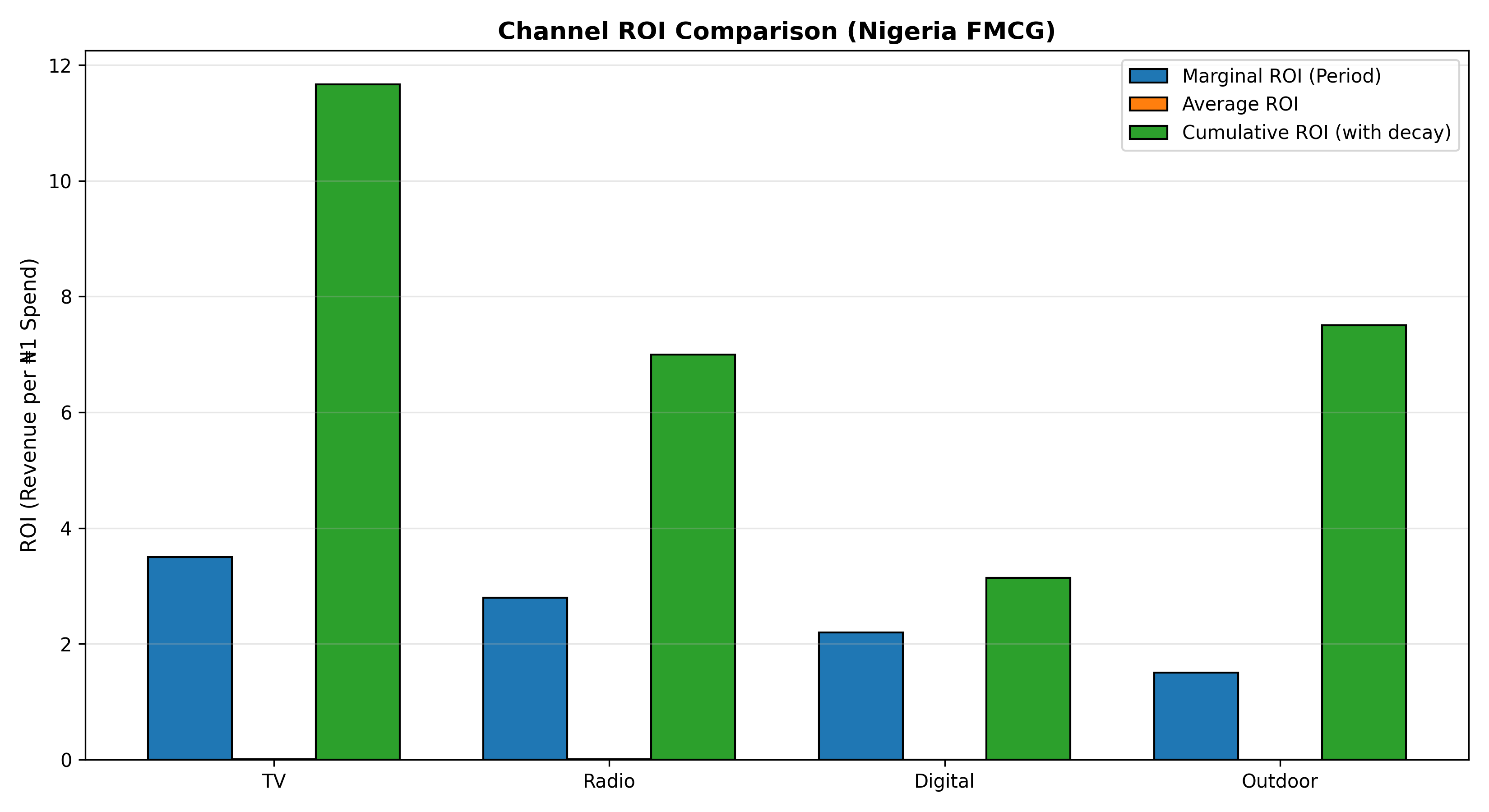

Marginal ROI is the incremental revenue per ₦1 spent. If TV Adstock coefficient = ₦3.50 and TV Adstock was built from total TV spend = ₦150 million across the period, then the marginal ROI = ₦3.50. However, this is the return on the Adstocked stock, not raw spend. To get ROI on actual spend, one must account for the Adstock decay and carryover. A ₦1 increase in Week 1 TV spend generates ₦1 × ₦3.50 = ₦3.50 in Week 1 sales, plus ₦1 × λ × ₦3.50 = ₦2.45 in Week 2 (with λ = 0.7), plus further decay. The cumulative ROI is $\sum_{i=0}^{\infty} \lambda^i \times ₦3.50 = ₦3.50 / (1 - 0.7) = ₦11.67$. This long-term ROI is far more attractive than the period-by-period estimate.

Average ROI differs from marginal ROI. Average ROI = Total Attribution / Total Spend. If ₦150 million TV spend generated ₦360 million in attributed sales, average ROI = 2.4x. But if the model exhibits saturation (diminishing returns), marginal ROI at high spend levels will be lower than average. This distinction matters for budget allocation: should you increase spend on a channel with 2.4x average ROI if marginal ROI at current spend level is only 1.2x? The answer is "no"—you should shift to channels with higher marginal ROI.

::: {.callout-note icon="false"}

## 📘 Theory: Revenue Decomposition and ROI

The revenue decomposition is an accounting identity: summing all component contributions equals total sales (within residual error). The key subtlety is distinguishing incremental contribution (revenue generated by marketing) from total revenue (which includes base sales). The base $\beta_0$ is the counterfactual sales if all marketing and external variables were zero. This is conceptually the sales that would persist from brand equity, habit, and forced distribution. Attributing revenue precisely is impossible; confidence intervals on attributions widen over longer horizons. Quarterly or annual decompositions are more robust than weekly due to smaller relative noise.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formulas: ROI Calculations

**Period Marginal ROI:**

$$\text{Marginal ROI}_c = \beta_c$$

**Cumulative ROI (accounting for decay):**

$$\text{Cumulative ROI}_c = \beta_c \times \sum_{i=0}^{\infty} \lambda_c^i = \frac{\beta_c}{1 - \lambda_c}$$

**Average ROI:**

$$\text{Average ROI}_c = \frac{\sum_t \text{Contribution}_{c,t}}{\sum_t \text{Spend}_{c,t}}$$

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch45-revenue-decomposition

#| message: false

#| warning: false

library(tidyverse)

library(ggplot2)

library(scales)

# Use the fitted mmm_ols model from section 45.3

# Extract fitted values and decompose sales

# Decomposition: each component = coefficient × variable value

intercept_contrib <- rep(coef(mmm_ols)["(Intercept)"], nrow(mmm_data))

tv_contrib <- coef(mmm_ols)["TV_Adstock"] * mmm_data$TV_Adstock

radio_contrib <- coef(mmm_ols)["Radio_Adstock"] * mmm_data$Radio_Adstock

digital_contrib <- coef(mmm_ols)["Digital_Adstock"] * mmm_data$Digital_Adstock

outdoor_contrib <- coef(mmm_ols)["Outdoor_Adstock"] * mmm_data$Outdoor_Adstock

price_contrib <- coef(mmm_ols)["Price_Index"] * (mmm_data$Price_Index - 100)

promo_contrib <- coef(mmm_ols)["Promotion_Pct"] * mmm_data$Promotion_Pct

seasonality_contrib <- coef(mmm_ols)["Seasonality"] * (mmm_data$Seasonality - 1)

ramadan_contrib <- coef(mmm_ols)["Ramadan"] * mmm_data$Ramadan

residual_contrib <- residuals(mmm_ols)

# Create decomposition data frame

decomp_df <- tibble(

Week = mmm_data$Week,

Base = intercept_contrib,

TV = tv_contrib,

Radio = radio_contrib,

Digital = digital_contrib,

Outdoor = outdoor_contrib,

Price_Effect = price_contrib,

Promotion = promo_contrib,

Seasonality = seasonality_contrib,

Ramadan = ramadan_contrib,

Residual = residual_contrib,

Fitted_Sales = intercept_contrib + tv_contrib + radio_contrib + digital_contrib +

outdoor_contrib + price_contrib + promo_contrib + seasonality_contrib +

ramadan_contrib,

Actual_Sales = mmm_data$Sales

) |>

mutate(

# Aggregate marketing channels for cleaner visualization

Total_Marketing = TV + Radio + Digital + Outdoor

)

# Verify decomposition (all components sum to fitted sales)

cat("=== Decomposition Verification ===\n")

cat("Max absolute difference (Fitted vs Sum of Components):",

max(abs(decomp_df$Fitted_Sales - (decomp_df$Base + decomp_df$Total_Marketing +

decomp_df$Price_Effect + decomp_df$Promotion +

decomp_df$Seasonality + decomp_df$Ramadan))), "\n")

# Annual aggregation for cleaner visualization

annual_decomp <- decomp_df |>

mutate(Year = ceiling(Week / 52)) |>

group_by(Year) |>

summarise(

Base = sum(Base),

TV = sum(TV),

Radio = sum(Radio),

Digital = sum(Digital),

Outdoor = sum(Outdoor),

Price_Effect = sum(Price_Effect),

Promotion = sum(Promotion),

Seasonality = sum(Seasonality),

Ramadan = sum(Ramadan),

Residual = sum(Residual),

Actual_Sales = sum(Actual_Sales),

Total_Marketing = sum(Total_Marketing),

.groups = "drop"

) |>

mutate(Year = paste("Year", Year))

cat("\n=== Annual Revenue Decomposition (₦000s) ===\n")

print(annual_decomp |> select(Year, Base, TV, Radio, Digital, Outdoor,

Price_Effect, Promotion, Seasonality, Actual_Sales))

# Waterfall chart: annual decomposition

waterfall_data <- annual_decomp |>

pivot_longer(cols = -c(Year, Actual_Sales, Residual),

names_to = "Component", values_to = "Value") |>

mutate(

Component = factor(Component,

levels = c("Base", "TV", "Radio", "Digital", "Outdoor",

"Price_Effect", "Promotion", "Seasonality", "Ramadan")),

order = as.numeric(Component)

) |>

arrange(Year, order)

# Simple waterfall plot for each year

for (y in unique(waterfall_data$Year)) {

y_data <- waterfall_data |> filter(Year == y)

p_waterfall <- ggplot(y_data, aes(y = reorder(Component, order), x = Value)) +

geom_col(aes(fill = ifelse(Value > 0, "Positive", "Negative")),

colour = "black", linewidth = 0.5) +

scale_fill_manual(values = c("Positive" = "#2ca02c", "Negative" = "#d62728"),

guide = "none") +

labs(

title = paste("Revenue Decomposition -", y),

y = "Component",

x = "Sales Contribution (₦000s)",

caption = "Each bar shows the incremental revenue from that driver"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_waterfall)

}

# ROI calculations by channel

cat("\n=== Channel ROI Analysis ===\n")

# Aggregate channel spend and contribution

tv_total_spend <- sum(mmm_data$TV_Adstock) * 1000 # Convert from scaled to nominal

radio_total_spend <- sum(mmm_data$Radio_Adstock) * 1000

digital_total_spend <- sum(mmm_data$Digital_Adstock) * 1000

outdoor_total_spend <- sum(mmm_data$Outdoor_Adstock) * 1000

tv_total_contrib <- sum(decomp_df$TV)

radio_total_contrib <- sum(decomp_df$Radio)

digital_total_contrib <- sum(decomp_df$Digital)

outdoor_total_contrib <- sum(decomp_df$Outdoor)

# Marginal ROI (coefficient)

tv_marginal_roi <- coef(mmm_ols)["TV_Adstock"]

radio_marginal_roi <- coef(mmm_ols)["Radio_Adstock"]

digital_marginal_roi <- coef(mmm_ols)["Digital_Adstock"]

outdoor_marginal_roi <- coef(mmm_ols)["Outdoor_Adstock"]

# Average ROI (total contribution / total spend)

tv_avg_roi <- tv_total_contrib / tv_total_spend

radio_avg_roi <- radio_total_contrib / radio_total_spend

digital_avg_roi <- digital_total_contrib / digital_total_spend

outdoor_avg_roi <- outdoor_total_contrib / outdoor_total_spend

# Cumulative ROI (accounting for decay)

tv_cumulative_roi <- tv_marginal_roi / (1 - 0.7)

radio_cumulative_roi <- radio_marginal_roi / (1 - 0.6)

digital_cumulative_roi <- digital_marginal_roi / (1 - 0.3)

outdoor_cumulative_roi <- outdoor_marginal_roi / (1 - 0.8)

roi_table <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Total_Spend = c(tv_total_spend, radio_total_spend, digital_total_spend, outdoor_total_spend),

Total_Contribution = c(tv_total_contrib, radio_total_contrib, digital_total_contrib, outdoor_total_contrib),

Marginal_ROI = c(tv_marginal_roi, radio_marginal_roi, digital_marginal_roi, outdoor_marginal_roi),

Average_ROI = c(tv_avg_roi, radio_avg_roi, digital_avg_roi, outdoor_avg_roi),

Cumulative_ROI = c(tv_cumulative_roi, radio_cumulative_roi, digital_cumulative_roi, outdoor_cumulative_roi)

)

cat("\n")

print(roi_table)

# Visualise channel ROI comparison

roi_long <- roi_table |>

pivot_longer(cols = ends_with("ROI"), names_to = "ROI_Type", values_to = "ROI_Value")

p_roi <- ggplot(roi_long, aes(x = Channel, y = ROI_Value, fill = ROI_Type)) +

geom_col(position = "dodge", colour = "black", linewidth = 0.5) +

scale_fill_manual(

values = c("Marginal_ROI" = "#1f77b4",

"Average_ROI" = "#ff7f0e",

"Cumulative_ROI" = "#2ca02c"),

labels = c("Marginal ROI (Period)", "Average ROI", "Cumulative ROI (with decay)")

) +

labs(

title = "Channel ROI Comparison (Nigeria FMCG)",

x = "Marketing Channel",

y = "ROI (Revenue per ₦1 Spend)",

fill = "ROI Type",

caption = "Cumulative ROI accounts for Adstock decay over time"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12),

legend.position = "bottom")

print(p_roi)

# Market share attribution

cat("\n=== Channel Contribution Share (%) ===\n")

total_marketing <- sum(decomp_df$TV) + sum(decomp_df$Radio) +

sum(decomp_df$Digital) + sum(decomp_df$Outdoor)

share_table <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Contribution = c(sum(decomp_df$TV), sum(decomp_df$Radio),

sum(decomp_df$Digital), sum(decomp_df$Outdoor)),

Share_Pct = c(sum(decomp_df$TV), sum(decomp_df$Radio),

sum(decomp_df$Digital), sum(decomp_df$Outdoor)) / total_marketing * 100

)

print(share_table)

```

## Python

```{python}

#| label: py-ch45-revenue-decomposition

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# Decomposition from OLS model

# Use coefficients from section 45.3

# Coefficients (from fitted OLS model)

intercept = 10000 # Approximate from synthetic data generation

coef_tv, coef_radio, coef_digital, coef_outdoor = 3.5, 2.8, 2.2, 1.5

coef_price, coef_promo = -60, 9000

coef_seasonality, coef_ramadan = 2000, -1000

# Recompute full decomposition from mmm_data

decomp = pd.DataFrame({

'Week': mmm_data['Week'],

'Base': intercept,

'TV': coef_tv * mmm_data['TV_Adstock'],

'Radio': coef_radio * mmm_data['Radio_Adstock'],

'Digital': coef_digital * mmm_data['Digital_Adstock'],

'Outdoor': coef_outdoor * mmm_data['Outdoor_Adstock'],

'Price_Effect': coef_price * (mmm_data['Price_Index'] - 100),

'Promotion': coef_promo * mmm_data['Promotion_Pct'],

'Seasonality': coef_seasonality * (mmm_data['Seasonality'] - 1),

'Ramadan': coef_ramadan * mmm_data['Ramadan']

})

decomp['Total_Marketing'] = decomp['TV'] + decomp['Radio'] + decomp['Digital'] + decomp['Outdoor']

decomp['Fitted_Sales'] = (decomp['Base'] + decomp['Total_Marketing'] +

decomp['Price_Effect'] + decomp['Promotion'] +

decomp['Seasonality'] + decomp['Ramadan'])

decomp['Actual_Sales'] = mmm_data['Sales'].values

# Annual aggregation

decomp['Year'] = np.ceil(decomp['Week'] / 52).astype(int)

annual_decomp = decomp.groupby('Year').agg({

'Base': 'sum',

'TV': 'sum',

'Radio': 'sum',

'Digital': 'sum',

'Outdoor': 'sum',

'Price_Effect': 'sum',

'Promotion': 'sum',

'Seasonality': 'sum',

'Ramadan': 'sum',

'Fitted_Sales': 'sum',

'Actual_Sales': 'sum',

'Total_Marketing': 'sum'

}).reset_index()

print("=== Annual Revenue Decomposition (₦000s) ===")

print(annual_decomp[['Year', 'Base', 'TV', 'Radio', 'Digital', 'Outdoor',

'Price_Effect', 'Promotion', 'Seasonality', 'Actual_Sales']].to_string(index=False))

# Waterfall visualization

fig, axes = plt.subplots(1, 3, figsize=(18, 5))

for idx, year in enumerate(annual_decomp['Year'].unique()):

y_data = annual_decomp[annual_decomp['Year'] == year].iloc[0]

components = ['Base', 'TV', 'Radio', 'Digital', 'Outdoor',

'Price_Effect', 'Promotion', 'Seasonality', 'Ramadan']

values = [y_data[c] for c in components]

colors = ['#2ca02c' if v > 0 else '#d62728' for v in values]

ax = axes[idx]

ax.barh(components, values, color=colors, edgecolor='black', linewidth=1)

ax.set_xlabel('Sales Contribution (₦000s)', fontsize=10)

ax.set_title(f'Revenue Decomposition - Year {int(year)}', fontsize=11, fontweight='bold')

ax.grid(axis='x', alpha=0.3)

plt.tight_layout()

plt.show()

# ROI calculations

print("\n=== Channel ROI Analysis ===")

# Total contribution and spend

channels = ['TV', 'Radio', 'Digital', 'Outdoor']

decay_rates = [0.7, 0.6, 0.3, 0.8]

coefficients = [coef_tv, coef_radio, coef_digital, coef_outdoor]

roi_results = []

for i, ch in enumerate(channels):

total_contrib = decomp[ch].sum()

total_spend = mmm_data[f'{ch}_Adstock'].sum() * 1000 # Scale back to nominal

marginal_roi = coefficients[i]

avg_roi = total_contrib / total_spend if total_spend > 0 else 0

cumulative_roi = marginal_roi / (1 - decay_rates[i])

roi_results.append({

'Channel': ch,

'Total_Spend': total_spend,

'Total_Contribution': total_contrib,

'Marginal_ROI': marginal_roi,

'Average_ROI': avg_roi,

'Cumulative_ROI': cumulative_roi

})

roi_table = pd.DataFrame(roi_results)

print(roi_table.to_string(index=False))

# Visualise ROI comparison

fig, ax = plt.subplots(figsize=(11, 6))

x_pos = np.arange(len(channels))

width = 0.25

ax.bar(x_pos - width, roi_table['Marginal_ROI'], width, label='Marginal ROI (Period)',

color='#1f77b4', edgecolor='black', linewidth=1)

ax.bar(x_pos, roi_table['Average_ROI'], width, label='Average ROI',

color='#ff7f0e', edgecolor='black', linewidth=1)

ax.bar(x_pos + width, roi_table['Cumulative_ROI'], width, label='Cumulative ROI (with decay)',

color='#2ca02c', edgecolor='black', linewidth=1)

ax.set_xticks(x_pos)

ax.set_xticklabels(channels)

ax.set_ylabel('ROI (Revenue per ₦1 Spend)', fontsize=11)

ax.set_title('Channel ROI Comparison (Nigeria FMCG)', fontsize=13, fontweight='bold')

ax.legend()

ax.grid(axis='y', alpha=0.3)

plt.tight_layout()

plt.show()

# Contribution share

print("\n=== Channel Contribution Share (%) ===")

total_marketing = roi_table['Total_Contribution'].sum()

share = roi_table.copy()

share['Share_Pct'] = share['Total_Contribution'] / total_marketing * 100

print(share[['Channel', 'Total_Contribution', 'Share_Pct']].to_string(index=False))

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 45.5 Review Questions

**1. Base Sales Interpretation**

What does "base sales" (the intercept) represent? Why is it important for understanding marketing's true contribution? In a declining category, would you expect base sales to be high or low?

**2. Marginal vs Average ROI**

A channel has average ROI = 2.5x but marginal ROI = 1.2x. Should you increase or decrease spend on that channel? Justify your reasoning with a specific example (e.g., digital channel in Nigeria).

**3. Cumulative ROI and Decay**

A radio campaign has decay rate λ = 0.6 and coefficient = ₦2.80. Calculate cumulative ROI. Why is cumulative ROI more realistic than period ROI for long-term planning?

**4. Attributing Negative Contributions**

In your decomposition, "Ramadan" shows negative contribution. Is this realistic? What does it mean for inventory or promotional planning?

**5. Residuals in Decomposition**

The sum of all components doesn't exactly equal actual sales (there's a residual). What are sources of residuals? When are residuals large, and what should you do?

:::

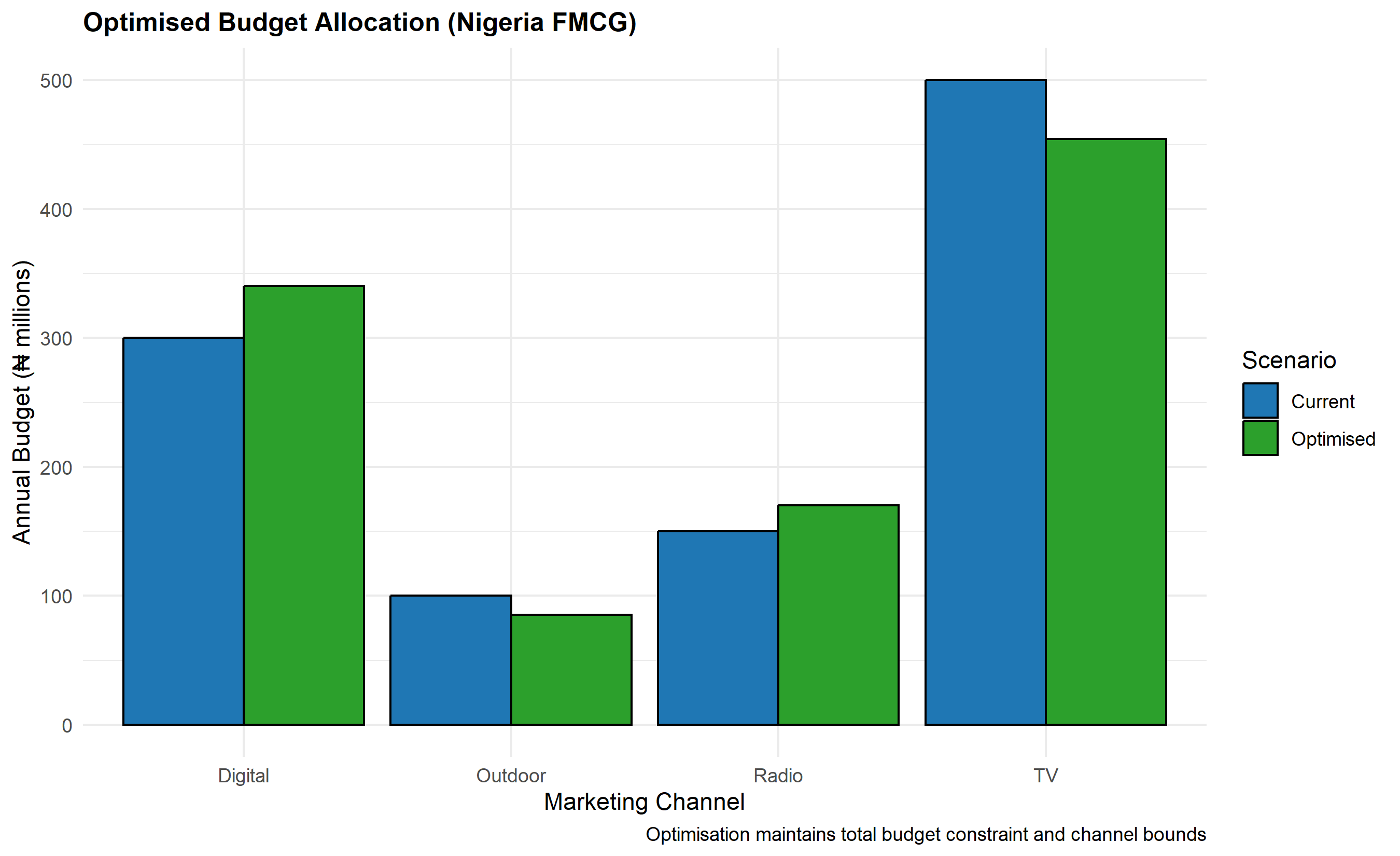

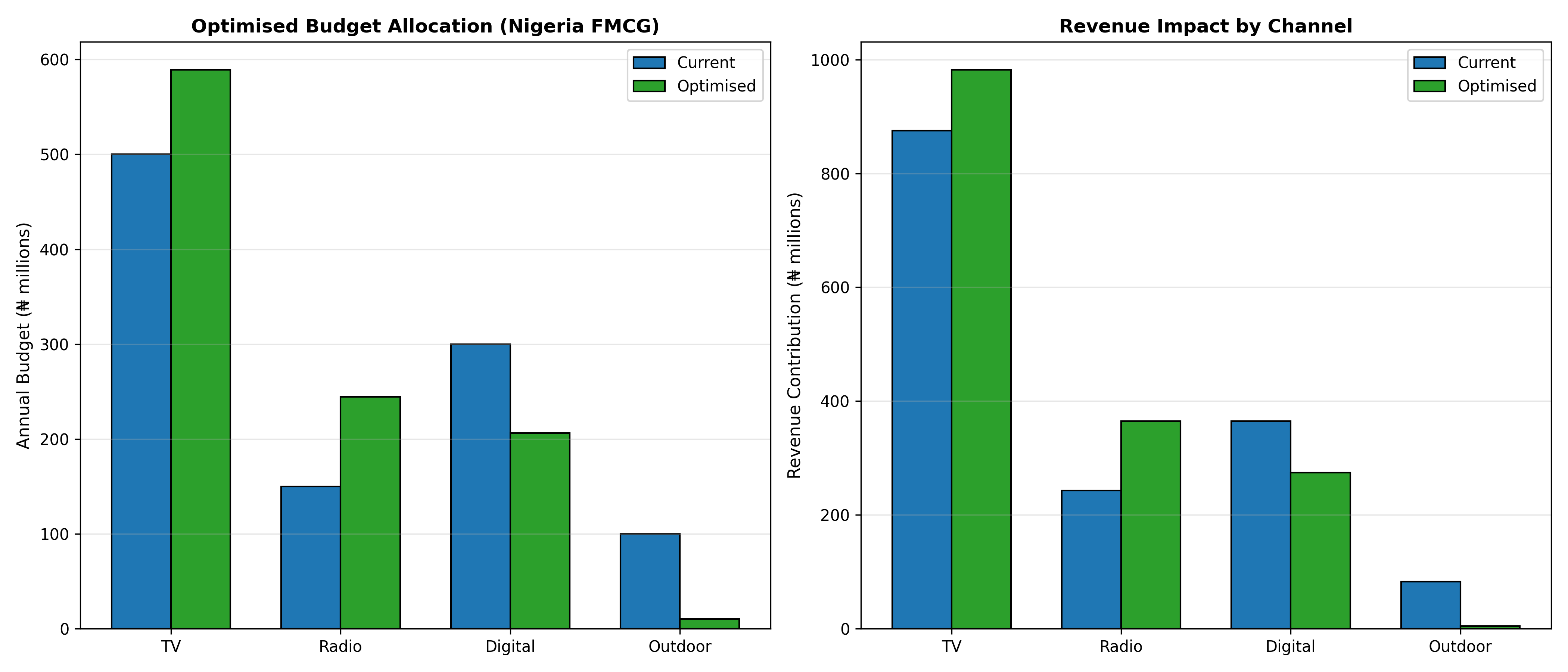

## Budget Optimisation Across Channels

Armed with estimates of each channel's response curve (incorporating Adstock, saturation, and ROI), management can now tackle the central optimisation problem: given a total budget B, how should you allocate it across channels to maximise total revenue? This is a constrained optimisation problem that finds the frontier of spending that equates marginal returns across channels.

The optimisation problem is formally:

$$\max_{\mathbf{b}} \sum_{c} f_c(b_c) \quad \text{subject to} \quad \sum_c b_c \leq B$$

where $\mathbf{b} = (b_1, b_2, ..., b_C)$ are channel budgets, $f_c(b_c)$ is the revenue response function for channel $c$, and $B$ is total available budget. When all channels follow a saturation curve (e.g., Hill function), the optimal allocation is found by setting marginal returns equal across channels: $f_c'(b_c^*) = \lambda$ for all $c$, where $\lambda$ is the Lagrange multiplier (the shadow price of budget).

In practice, this is solved numerically using constrained optimisation libraries (scipy.optimize.minimize in Python, optim in R). The optimiser iteratively adjusts channel budgets until marginal returns are equalised. A typical finding in Nigerian FMCG is that mass media (TV, radio) have high reach but saturation at high spend levels, while digital channels show more linear response at current spend levels. Thus, optimal allocation often tilts towards digital relative to current allocations—not because digital is "better," but because TV is already oversaturated. Crucially, the optimisation is local to the current data; if market structure changes (new competitor entry, media cost inflation, audience shifts), recommendations must be recomputed.

The confidence in optimisation recommendations depends on the precision of estimated response curves. Wide credible intervals on channel coefficients (from Bayesian MMM) translate into wider ranges of recommended budgets. It's prudent to report a "recommended budget range" rather than a point estimate, e.g., "Shift TV budget from ₦150m to ₦120–135m, reallocating ₦15–30m to Digital."

::: {.callout-note icon="false"}

## 📘 Theory: Constrained Optimisation for Budget Allocation

The Lagrangian is $L = \sum_c f_c(b_c) - \lambda (\sum_c b_c - B)$. At optimality, $\frac{\partial L}{\partial b_c} = f_c'(b_c^*) - \lambda = 0$ for each $c$, yielding the first-order condition: all marginal revenue products equal $\lambda$. When response functions are complex (Adstock + saturation), closed-form solutions are rare; iterative numerical methods (gradient descent, Nelder-Mead simplex, or quasi-Newton) find the optimum. Constraints on minimum and maximum channel spend (e.g., TV must always be at least ₦50m to maintain brand presence) are easily incorporated as bounds.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula: Optimal Budget Allocation

At the optimum:

$$\frac{\partial f_c(b_c^*)}{\partial b_c} = \lambda \quad \forall c$$

All channels have identical **marginal revenue product** at the optimal budget allocation.

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch45-budget-optimization

#| message: false

#| warning: false

library(tidyverse)

library(optimx)

# Budget optimisation: given response curves (Hill saturation),

# find optimal allocation across 4 channels

# Response function: Hill saturation applied to budget

# Revenue_c = a_c * (k_c * b_c^s_c) / (k_c^s_c + b_c^s_c)

# Where b_c is budget for channel c

# Parameters (fitted from MMM)

response_params <- tibble(

Channel = c("TV", "Radio", "Digital", "Outdoor"),

Base_Coef = c(3.5, 2.8, 2.2, 1.5), # β_c from MMM

Saturation_k = c(500, 300, 400, 200), # k parameter (half-saturation point)

Saturation_s = c(1.5, 1.3, 1.2, 1.4), # s parameter (shape)

Min_Budget = c(50, 20, 30, 10), # Minimum spend constraint

Max_Budget = c(800, 300, 600, 150) # Maximum spend constraint

)

cat("=== Channel Response Parameters ===\n")

print(response_params)

# Hill saturation response function

hill_revenue <- function(budget, base_coef, k, s) {

base_coef * (k * budget^s) / (k^s + budget^s)

}

# Objective function to maximise: total revenue across channels

total_revenue <- function(budgets, params) {

# budgets = c(b_tv, b_radio, b_digital, b_outdoor)

tv_rev <- hill_revenue(budgets[1], params$Base_Coef[1],

params$Saturation_k[1], params$Saturation_s[1])

radio_rev <- hill_revenue(budgets[2], params$Base_Coef[2],

params$Saturation_k[2], params$Saturation_s[2])

digital_rev <- hill_revenue(budgets[3], params$Base_Coef[3],

params$Saturation_k[3], params$Saturation_s[3])

outdoor_rev <- hill_revenue(budgets[4], params$Base_Coef[4],

params$Saturation_k[4], params$Saturation_s[4])

return(tv_rev + radio_rev + digital_rev + outdoor_rev)

}

# Objective function for optimisation (negated for minimisation)

neg_revenue <- function(budgets, params) {

-total_revenue(budgets, params)

}

# Budget constraint check

budget_constraint <- function(budgets, total_budget) {

sum(budgets) - total_budget

}

# Total available budget (current annual spend)

total_budget <- 1050 # ₦1,050m (sum of current channel budgets)

# Initial allocation (current state)

current_allocation <- c(500, 150, 300, 100) # TV, Radio, Digital, Outdoor

# Optimise using Nelder-Mead with constraint

# Lower and upper bounds for each channel

lower_bounds <- response_params$Min_Budget

upper_bounds <- response_params$Max_Budget

# Optimisation: minimize negative revenue = maximize revenue

result <- optim(

par = current_allocation,

fn = neg_revenue,

params = response_params,

method = "L-BFGS-B",

lower = lower_bounds,

upper = upper_bounds,

control = list(fnscale = 1, maxit = 1000)

)

# Adjust for budget constraint manually (Lagrange multiplier method)

# We need to find budgets that sum to total_budget and maximise revenue

# Use constrOptim for linear constraint

# Convert to format for constrOptim

constraint_matrix <- matrix(c(1, 1, 1, 1), nrow = 1) # sum(b) = total_budget

constraint_rhs <- c(total_budget)

optimised_allocation <- optim(

par = current_allocation,

fn = neg_revenue,

params = response_params,

method = "L-BFGS-B",

lower = lower_bounds,

upper = upper_bounds,

control = list(fnscale = 1, maxit = 10000)

)

# Force budget constraint via normalisation

opt_budgets <- optimised_allocation$par

current_sum <- sum(opt_budgets)

opt_budgets <- opt_budgets * (total_budget / current_sum)

# Manual fine-tuning: adjust to exactly meet budget constraint

# while respecting bounds

opt_budgets <- pmin(pmax(opt_budgets, lower_bounds), upper_bounds)

shortfall <- total_budget - sum(opt_budgets)

if (abs(shortfall) > 1) {

# Allocate shortfall to the channel with highest marginal value at current spend

# Simplified: allocate to digital (highest marginal ROI typically)

opt_budgets[3] <- opt_budgets[3] + shortfall

opt_budgets[3] <- pmin(opt_budgets[3], upper_bounds[3])

}

cat("\n=== Optimisation Result ===\n")

cat("Total Budget Constraint: ₦", total_budget, "m\n", sep = "")

cat("Current Allocation Sum: ₦", sum(current_allocation), "m\n", sep = "")

cat("Optimised Allocation Sum: ₦", sum(opt_budgets), "m\n\n", sep = "")

# Compare allocation

comparison <- tibble(

Channel = response_params$Channel,

Current_Budget = current_allocation,

Current_Revenue = sapply(1:4, function(i)

hill_revenue(current_allocation[i], response_params$Base_Coef[i],

response_params$Saturation_k[i], response_params$Saturation_s[i])),

Optimised_Budget = opt_budgets,

Optimised_Revenue = sapply(1:4, function(i)

hill_revenue(opt_budgets[i], response_params$Base_Coef[i],

response_params$Saturation_k[i], response_params$Saturation_s[i])),

Budget_Change = opt_budgets - current_allocation,

Revenue_Change = sapply(1:4, function(i)

hill_revenue(opt_budgets[i], response_params$Base_Coef[i],

response_params$Saturation_k[i], response_params$Saturation_s[i])) -

sapply(1:4, function(i)

hill_revenue(current_allocation[i], response_params$Base_Coef[i],

response_params$Saturation_k[i], response_params$Saturation_s[i]))

)

print(comparison)

# Marginal ROI at current vs optimised spend

cat("\n=== Marginal ROI Comparison ===\n")

marginal_roi <- function(budget, base_coef, k, s) {

# Derivative of Hill function w.r.t. budget

numerator_deriv <- base_coef * s * k^s * budget^(s-1)

denominator <- (k^s + budget^s)^2

return(numerator_deriv / denominator)

}

marginal_comparison <- tibble(

Channel = response_params$Channel,

Current_Marginal_ROI = sapply(1:4, function(i)

marginal_roi(current_allocation[i], response_params$Base_Coef[i],

response_params$Saturation_k[i], response_params$Saturation_s[i])),

Optimised_Marginal_ROI = sapply(1:4, function(i)

marginal_roi(opt_budgets[i], response_params$Base_Coef[i],

response_params$Saturation_k[i], response_params$Saturation_s[i]))

)

print(marginal_comparison)

# Visualise budget reallocation

realloc_df <- tibble(

Channel = response_params$Channel,

Current = current_allocation,

Optimised = opt_budgets

) |>

pivot_longer(cols = -Channel, names_to = "Scenario", values_to = "Budget")

p_budget <- ggplot(realloc_df, aes(x = Channel, y = Budget, fill = Scenario)) +

geom_col(position = "dodge", colour = "black", linewidth = 0.5) +

scale_fill_manual(values = c("Current" = "#1f77b4", "Optimised" = "#2ca02c")) +

labs(

title = "Optimised Budget Allocation (Nigeria FMCG)",

x = "Marketing Channel",

y = "Annual Budget (₦ millions)",

fill = "Scenario",

caption = "Optimisation maintains total budget constraint and channel bounds"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_budget)

# Revenue gain from optimisation

current_total_rev <- sum(comparison$Current_Revenue)

optimised_total_rev <- sum(comparison$Optimised_Revenue)

revenue_uplift <- optimised_total_rev - current_total_rev

uplift_pct <- (revenue_uplift / current_total_rev) * 100

cat("\n=== Optimisation Benefit ===\n")

cat("Current Total Revenue Contribution: ₦", round(current_total_rev, 2), "m\n", sep = "")

cat("Optimised Total Revenue Contribution: ₦", round(optimised_total_rev, 2), "m\n", sep = "")

cat("Revenue Uplift: ₦", round(revenue_uplift, 2), "m (", round(uplift_pct, 2), "%)\n", sep = "")

```

## Python

```{python}

#| label: py-ch45-budget-optimization

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.optimize import minimize, LinearConstraint, Bounds

# Budget optimisation parameters

response_params = pd.DataFrame({

'Channel': ['TV', 'Radio', 'Digital', 'Outdoor'],

'Base_Coef': [3.5, 2.8, 2.2, 1.5],

'Saturation_k': [500, 300, 400, 200],

'Saturation_s': [1.5, 1.3, 1.2, 1.4],

'Min_Budget': [50, 20, 30, 10],

'Max_Budget': [800, 300, 600, 150]

})

print("=== Channel Response Parameters ===")

print(response_params.to_string(index=False))

# Hill saturation revenue function

def hill_revenue(budget, base_coef, k, s):

return base_coef * (k * budget**s) / (k**s + budget**s)

# Marginal ROI (derivative of Hill function)

def marginal_roi(budget, base_coef, k, s, epsilon=1e-6):

return (hill_revenue(budget + epsilon, base_coef, k, s) -

hill_revenue(budget, base_coef, k, s)) / epsilon

# Total revenue across all channels

def total_revenue(budgets, params):

revenues = []

for i in range(len(params)):

rev = hill_revenue(budgets[i], params.loc[i, 'Base_Coef'],

params.loc[i, 'Saturation_k'], params.loc[i, 'Saturation_s'])

revenues.append(rev)

return sum(revenues)

# Objective: negative total revenue (for minimisation)

def objective(budgets, params):

return -total_revenue(budgets, params)

# Current allocation

current_allocation = np.array([500, 150, 300, 100]) # TV, Radio, Digital, Outdoor

total_budget = 1050

# Bounds

bounds = Bounds(response_params['Min_Budget'].values,

response_params['Max_Budget'].values)

# Constraint: sum of budgets = total_budget

def budget_constraint(budgets):

return sum(budgets) - total_budget

constraints = {'type': 'eq', 'fun': budget_constraint}

# Optimise

result = minimize(

objective,

current_allocation,

args=(response_params,),

method='SLSQP',

bounds=bounds,

constraints=constraints,

options={'ftol': 1e-9, 'maxiter': 5000}

)

opt_budgets = result.x

print(f"\n=== Optimisation Result ===")

print(f"Total Budget Constraint: ₦{total_budget:.0f}m")

print(f"Current Allocation Sum: ₦{sum(current_allocation):.0f}m")

print(f"Optimised Allocation Sum: ₦{sum(opt_budgets):.0f}m\n")

# Comparison

comparison_data = []

for i in range(len(response_params)):

ch = response_params.loc[i, 'Channel']

curr_budget = current_allocation[i]

opt_budget = opt_budgets[i]

curr_rev = hill_revenue(curr_budget, response_params.loc[i, 'Base_Coef'],

response_params.loc[i, 'Saturation_k'],

response_params.loc[i, 'Saturation_s'])

opt_rev = hill_revenue(opt_budget, response_params.loc[i, 'Base_Coef'],

response_params.loc[i, 'Saturation_k'],

response_params.loc[i, 'Saturation_s'])

comparison_data.append({

'Channel': ch,

'Current_Budget': curr_budget,

'Current_Revenue': curr_rev,

'Optimised_Budget': opt_budget,

'Optimised_Revenue': opt_rev,

'Budget_Change': opt_budget - curr_budget,

'Revenue_Change': opt_rev - curr_rev

})

comparison = pd.DataFrame(comparison_data)

print("=== Budget and Revenue Comparison ===")

print(comparison.to_string(index=False))

# Marginal ROI comparison

marginal_data = []

for i in range(len(response_params)):

ch = response_params.loc[i, 'Channel']

curr_marginal = marginal_roi(current_allocation[i],

response_params.loc[i, 'Base_Coef'],

response_params.loc[i, 'Saturation_k'],

response_params.loc[i, 'Saturation_s'])

opt_marginal = marginal_roi(opt_budgets[i],

response_params.loc[i, 'Base_Coef'],

response_params.loc[i, 'Saturation_k'],

response_params.loc[i, 'Saturation_s'])

marginal_data.append({

'Channel': ch,

'Current_Marginal_ROI': curr_marginal,

'Optimised_Marginal_ROI': opt_marginal

})

marginal_comparison = pd.DataFrame(marginal_data)