---

title: "Brand Analytics"

author: "Bongo Adi"

---

```{python}

#| label: python-setup-46-brand-analytics

#| include: false

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

from statsmodels.regression.linear_model import OLS

from statsmodels.formula.api import mixedlm, ols

from sklearn.decomposition import PCA

from sklearn.preprocessing import StandardScaler

```

::: {.callout-note icon="false"}

## 📋 Learning Objectives

- Understand brand equity frameworks and the financial value of brands

- Calculate brand health metrics: awareness, consideration, preference, loyalty

- Analyse the brand funnel and conversion rates at each stage

- Build and interpret mixed-effects models for longitudinal brand tracking data

- Monitor brand sentiment and share of voice from social media text

- Create perceptual maps using TF-IDF and PCA for competitive positioning

- Apply confirmatory factor analysis (CFA) to measure brand equity dimensions

- Implement brand equity measurement workflows in R and Python with Nigerian examples

:::

## What Is a Brand and Why Does It Matter?

A brand is far more than a logo, colour, or slogan. In economic terms, a brand is the sum of perceptions, emotions, and associations that consumers attach to a company or product name. Brand equity—the premium value consumers are willing to pay for a branded product over a generic equivalent—is measurable, tradeable, and often represents a company's most valuable asset. A consumer might pay ₦350 for a 70g packet of Indomie noodles when a generic noodle product at ₦180 is chemically indistinguishable. The extra ₦170 is brand equity: the value of taste memory, consistent quality expectations, cultural ubiquity, and emotional attachment built over decades.

David Aaker's brand equity model, still the gold standard in marketing scholarship, decomposes brand equity into four dimensions: brand awareness (is the brand top-of-mind?), brand associations (what do consumers think the brand stands for?), perceived quality (do consumers believe the product delivers?), and brand loyalty (would consumers repurchase, and recommend to others?). In the Nigerian context, this framework plays out distinctly. Dangote Group's brand equity rests on awareness (nearly universal in Nigeria), associations with scale and trust ("Dangote makes it"), and perceived quality bolstered by the conglomerate's vertical integration and control. GTBank's brand equity among urban, affluent Nigerians centers on innovation (pioneering internet banking, investment apps) and prestige. Indomie's brand equity is purely affective: perfect taste, ubiquity, affordability, and cultural resonance (instant noodles are a staple of Nigerian student life, outdoor gatherings, and emergency meals).

Why does brand measurement matter? Without measurement, brand investments feel like costs, not assets. A brand manager might justify a ₦200 million annual TV spend only by attributing direct sales to it—a short-term view. But if that spend strengthens brand awareness by 3 percentage points among target consumers, and awareness drives a 1.5x purchase likelihood boost across a 10-year horizon, the true ROI is vastly higher. Brand metrics provide longitudinal signals that sales metrics miss. A brand could show flat sales this quarter (market contraction) while gaining awareness and preference (portending future sales growth). Conversely, sales could surge due to heavy discounting (eroding brand equity) while awareness declines (danger signal). Tracking brand health separately from sales avoids strategic myopia.

## Brand Health Metrics and the Brand Funnel

The brand funnel conceptualises the customer journey as a series of stages, each with a conversion rate. At the top is **brand awareness**: what percentage of the target population has heard of the brand? Awareness branches into spontaneous (unaided) recall—consumer names the brand without prompting—and aided awareness (recognises the brand when shown). Below awareness is **brand consideration**: among those aware, how many are willing to try or buy the brand? Next is **brand preference**: how many actually prefer it to alternatives? Then comes **purchase** (trial among non-users, repeat among users), and finally **loyalty**: do consumers stick with the brand despite competitive offers?

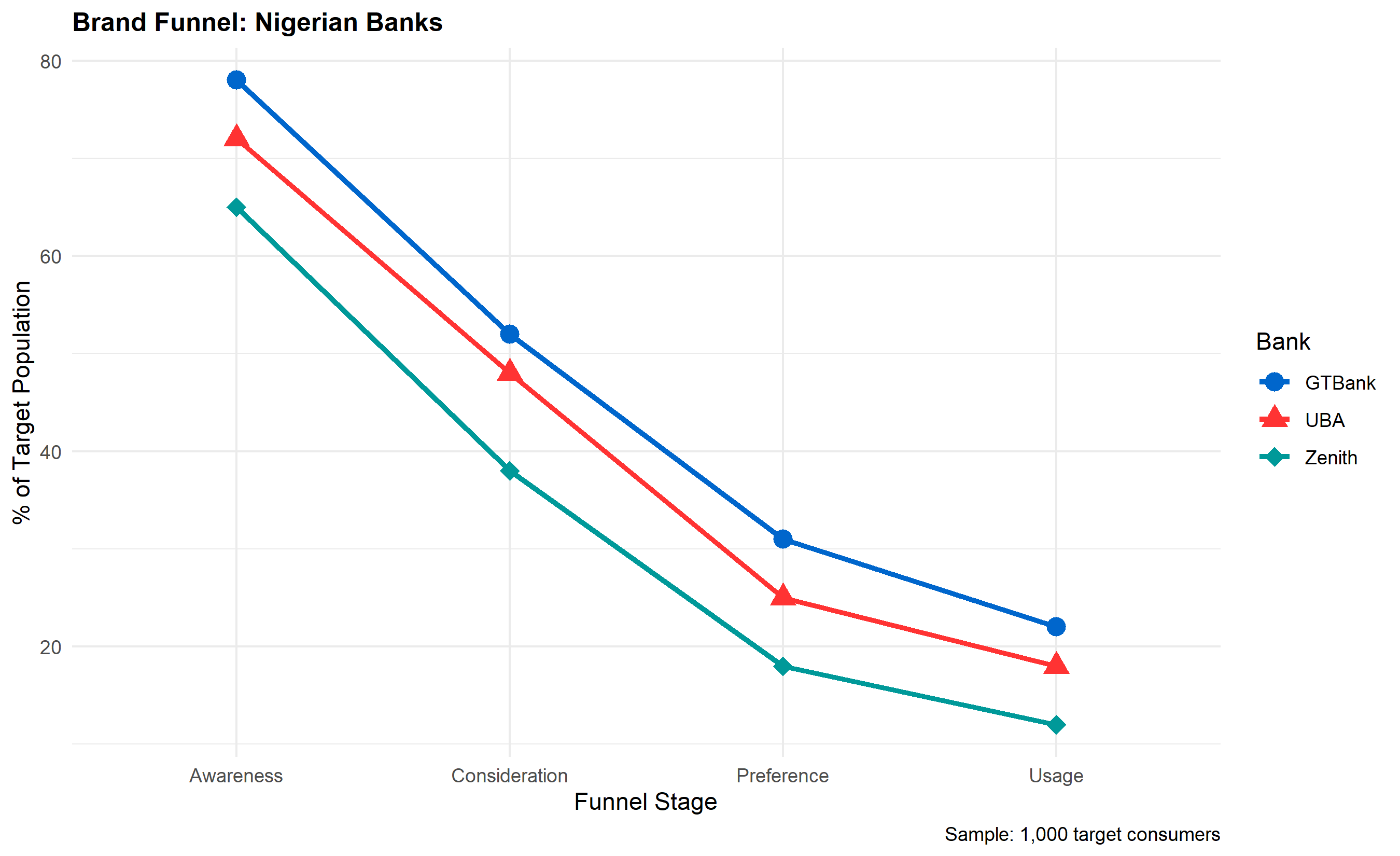

Each stage is measurable through brand tracking surveys, typically administered monthly or quarterly to a panel of 500–2,000 respondents representative of the target market. A typical Nigerian bank's brand funnel might look like: awareness = 75%, consideration = 45%, preference = 28%, purchase/usage = 18%, loyalty (NPS 7–10) = 9%. The funnel identifies bottlenecks: if awareness is strong but consideration is weak, the barrier is perception or product fit, not reach. If consideration is healthy but purchase is low, pricing or availability is the issue.

Key metrics within the funnel include:

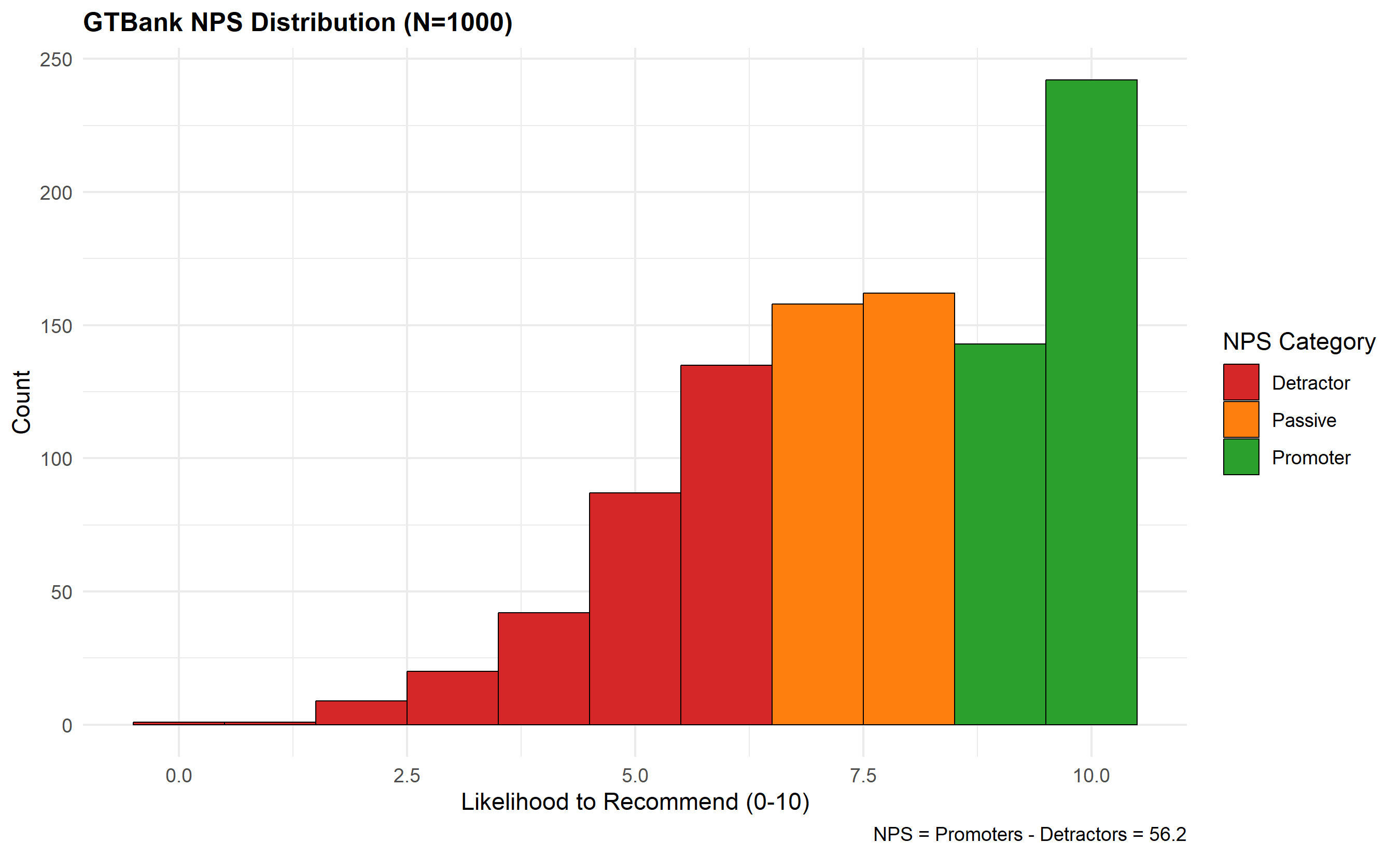

- **Net Promoter Score (NPS):** Consumers rate likelihood to recommend on a 0–10 scale. Promoters (9–10) minus Detractors (0–6) gives NPS (range: −100 to +100). NPS > 50 is excellent, 0–50 is good, negative is alarming.

- **Repeat Purchase Rate:** Among customers, what % repurchase within a defined period (e.g., 90 days)? Higher repeats signal loyalty.

- **Brand Loyalty Index:** Multi-item scale (e.g., "I am loyal to [brand]," "I rarely switch brands," "I recommend [brand] to others") measured on a 1–7 Likert scale, averaged for a composite score.

- **Category Involvement:** How much do consumers care about the category? High-involvement categories (cars, homes) require deeper funnel analysis; low-involvement (salt, matches) show faster funnel flow.

::: {.callout-note icon="false"}

## 📘 Theory: Aaker Brand Equity Framework

David Aaker's model posits four pillars: (1) Brand Awareness—recognition and recall; (2) Brand Associations—attributes, benefits, and emotional links consumers hold; (3) Perceived Quality—consumer belief in product excellence; (4) Brand Loyalty—tendency to repurchase and resist competitive appeals. Each pillar is measured via survey items; factor analysis confirms dimensionality. Brand equity then equals awareness × (perceived quality + associations + loyalty). The framework acknowledges that equity varies by segment: affluent consumers value GTBank's digital innovation, while rural consumers may prioritize accessibility.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formulas: Brand Funnel and Loyalty Metrics

**Brand Funnel Conversion:**

$$\text{Conversion Rate}_{i \to j} = \frac{\text{Consumers at Stage } j}{\text{Consumers at Stage } i}$$

**Net Promoter Score:**

$$\text{NPS} = \% \text{Promoters}_{(9-10)} - \% \text{Detractors}_{(0-6)}$$

**Brand Loyalty Index (Composite):**

$$\text{Loyalty Index} = \frac{1}{n} \sum_{i=1}^{n} \text{Item}_i \quad \text{(items on 1-7 Likert scale)}$$

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch46-brand-funnel

#| message: false

#| warning: false

library(tidyverse)

library(ggplot2)

library(scales)

# Synthetic brand tracking survey: 3 Nigerian banks

# Sample: 1,000 respondents, 3 competing banks (GTBank, UBA, Zenith)

set.seed(3174)

n_respondents <- 1000

banks <- c("GTBank", "UBA", "Zenith")

# Awareness, Consideration, Preference rates by bank

funnel_rates <- tibble(

Bank = banks,

Awareness_Pct = c(78, 72, 65),

Consideration_Pct = c(52, 48, 38),

Preference_Pct = c(31, 25, 18),

Usage_Pct = c(22, 18, 12),

Loyalty_NPS = c(58, 42, 28)

)

cat("=== Brand Funnel Data (% of total sample) ===\n")

print(funnel_rates)

# Create funnel visualization

funnel_long <- funnel_rates |>

select(Bank, Awareness_Pct, Consideration_Pct, Preference_Pct, Usage_Pct) |>

pivot_longer(cols = -Bank, names_to = "Stage", values_to = "Percentage") |>

mutate(

Stage = factor(Stage, levels = c("Awareness_Pct", "Consideration_Pct",

"Preference_Pct", "Usage_Pct"),

labels = c("Awareness", "Consideration", "Preference", "Usage")),

Bank = factor(Bank, levels = banks)

)

# Funnel chart

p_funnel <- ggplot(funnel_long, aes(x = Stage, y = Percentage, group = Bank,

colour = Bank, shape = Bank)) +

geom_point(size = 4) +

geom_line(linewidth = 1.2) +

scale_colour_manual(

values = c("GTBank" = "#0066CC", "UBA" = "#FF3333", "Zenith" = "#009999")

) +

scale_shape_manual(

values = c("GTBank" = 16, "UBA" = 17, "Zenith" = 18)

) +

labs(

title = "Brand Funnel: Nigerian Banks",

x = "Funnel Stage",

y = "% of Target Population",

colour = "Bank",

shape = "Bank",

caption = "Sample: 1,000 target consumers"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_funnel)

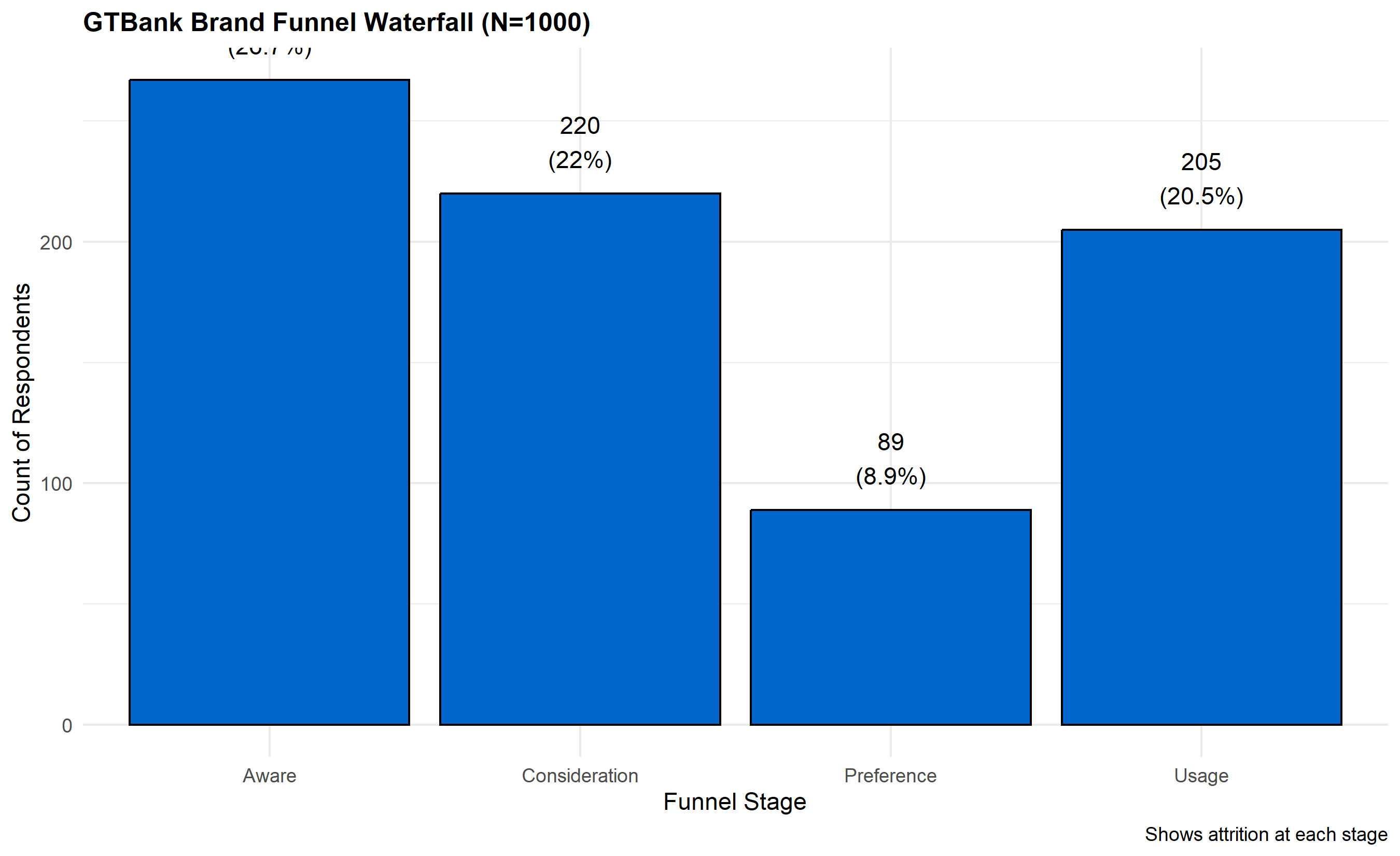

# Detailed breakdown for one bank (GTBank)

gtbank_respondents <- tibble(

Respondent_ID = 1:n_respondents,

Bank = "GTBank"

)

# Assign funnel stage based on probabilities

set.seed(3174)

gtbank_respondents <- gtbank_respondents |>

mutate(

Awareness = rbinom(n(), 1, 0.78),

Consideration = ifelse(Awareness == 1, rbinom(n(), 1, 0.52/0.78), 0),

Preference = ifelse(Consideration == 1, rbinom(n(), 1, 0.31/0.52), 0),

Usage = ifelse(Preference == 1, rbinom(n(), 1, 0.22/0.31), 0)

)

# Count funnel stages

funnel_counts <- tibble(

Stage = c("Unaware", "Aware", "Consideration", "Preference", "Usage"),

Count = c(

sum(gtbank_respondents$Awareness == 0),

sum(gtbank_respondents$Awareness == 1) - sum(gtbank_respondents$Consideration == 1),

sum(gtbank_respondents$Consideration == 1) - sum(gtbank_respondents$Preference == 1),

sum(gtbank_respondents$Preference == 1) - sum(gtbank_respondents$Usage == 1),

sum(gtbank_respondents$Usage == 1)

),

Percentage = c(

sum(gtbank_respondents$Awareness == 0) / n_respondents * 100,

(sum(gtbank_respondents$Awareness == 1) - sum(gtbank_respondents$Consideration == 1)) / n_respondents * 100,

(sum(gtbank_respondents$Consideration == 1) - sum(gtbank_respondents$Preference == 1)) / n_respondents * 100,

(sum(gtbank_respondents$Preference == 1) - sum(gtbank_respondents$Usage == 1)) / n_respondents * 100,

sum(gtbank_respondents$Usage == 1) / n_respondents * 100

)

)

cat("\n=== GTBank Detailed Funnel Breakdown (N=1000) ===\n")

print(funnel_counts)

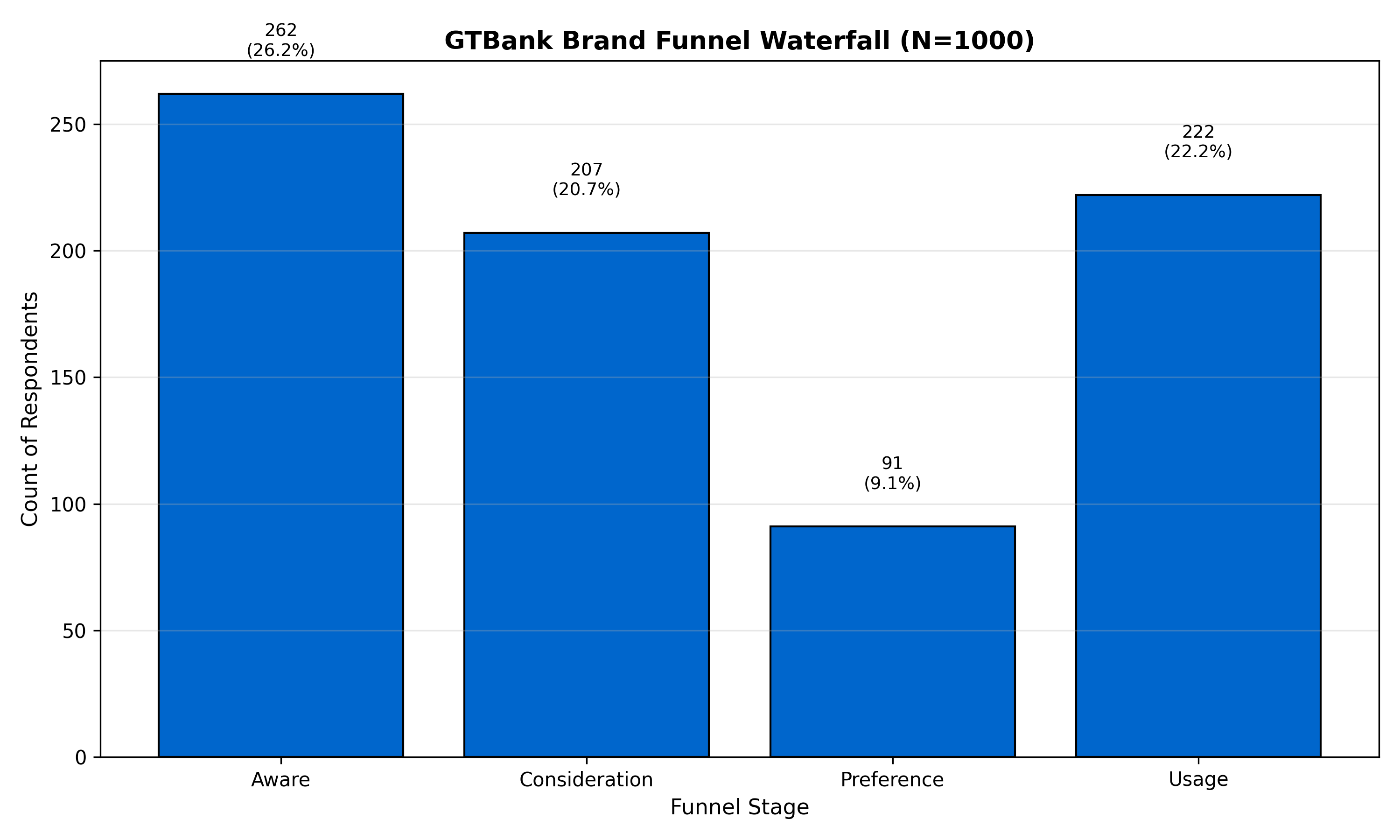

# Waterfall visualization

funnel_counts_ordered <- funnel_counts |>

filter(Stage != "Unaware") |>

arrange(match(Stage, c("Aware", "Consideration", "Preference", "Usage")))

p_waterfall <- ggplot(funnel_counts_ordered, aes(x = factor(Stage, levels = c("Aware", "Consideration", "Preference", "Usage")),

y = Count)) +

geom_col(fill = "#0066CC", colour = "black", linewidth = 0.5) +

geom_text(aes(label = paste0(Count, "\n(", round(Percentage, 1), "%)")),

vjust = -0.5, fontsize = 3) +

labs(

title = "GTBank Brand Funnel Waterfall (N=1000)",

x = "Funnel Stage",

y = "Count of Respondents",

caption = "Shows attrition at each stage"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_waterfall)

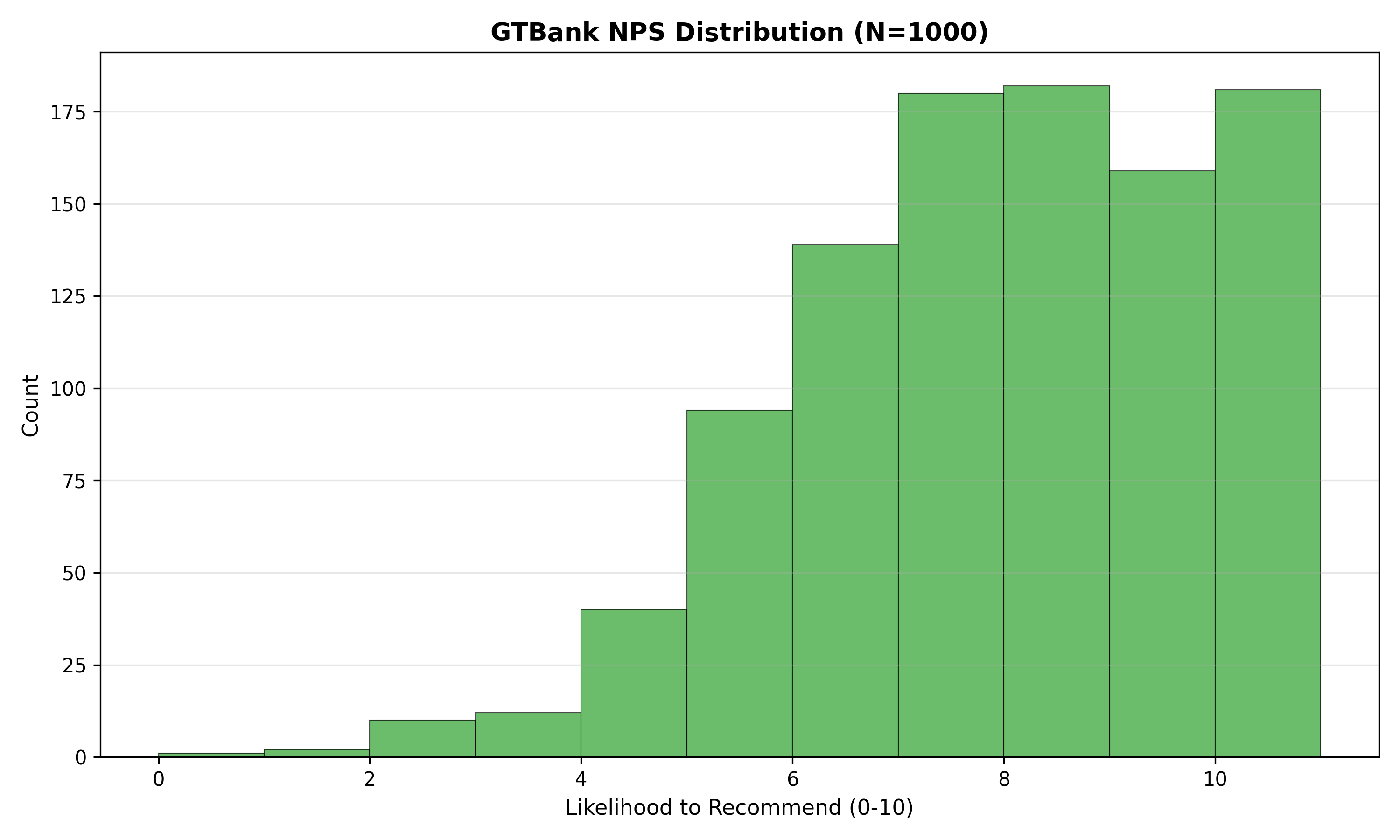

# NPS and Loyalty metrics (synthetic)

gtbank_nps_data <- tibble(

Respondent_ID = 1:n_respondents,

Bank = "GTBank",

# NPS: score on 0-10 scale

NPS_Score = rnorm(n_respondents, mean = 7.8, sd = 2.2) |> pmax(0) |> pmin(10) |> round(),

# Loyalty items (1-7 Likert)

Loyalty_Item1 = sample(1:7, n_respondents, replace = T, prob = c(0.02, 0.04, 0.08, 0.15, 0.25, 0.30, 0.16)),

Loyalty_Item2 = sample(1:7, n_respondents, replace = T, prob = c(0.03, 0.05, 0.10, 0.20, 0.22, 0.25, 0.15)),

Loyalty_Item3 = sample(1:7, n_respondents, replace = T, prob = c(0.04, 0.06, 0.12, 0.18, 0.20, 0.28, 0.12))

) |>

mutate(

NPS_Category = case_when(

NPS_Score >= 9 ~ "Promoter",

NPS_Score >= 7 ~ "Passive",

TRUE ~ "Detractor"

),

Loyalty_Index = (Loyalty_Item1 + Loyalty_Item2 + Loyalty_Item3) / 3

)

# Calculate NPS

nps_promoters <- sum(gtbank_nps_data$NPS_Score >= 9) / n_respondents * 100

nps_detractors <- sum(gtbank_nps_data$NPS_Score <= 6) / n_respondents * 100

nps_score <- nps_promoters - nps_detractors

cat("\n=== GTBank NPS Metrics ===\n")

cat("Promoters (9-10):", round(nps_promoters, 1), "%\n")

cat("Passives (7-8):", round(100 - nps_promoters - nps_detractors, 1), "%\n")

cat("Detractors (0-6):", round(nps_detractors, 1), "%\n")

cat("Net Promoter Score (NPS):", round(nps_score, 1), "\n")

# Loyalty index distribution

cat("\n=== Brand Loyalty Index Distribution ===\n")

cat("Mean:", round(mean(gtbank_nps_data$Loyalty_Index), 2), "\n")

cat("Std Dev:", round(sd(gtbank_nps_data$Loyalty_Index), 2), "\n")

cat("Median:", round(median(gtbank_nps_data$Loyalty_Index), 2), "\n")

# Visualization of NPS distribution

p_nps <- ggplot(gtbank_nps_data, aes(x = NPS_Score)) +

geom_histogram(aes(fill = NPS_Category), binwidth = 1, colour = "black", linewidth = 0.3) +

scale_fill_manual(values = c("Promoter" = "#2ca02c", "Passive" = "#ff7f0e", "Detractor" = "#d62728")) +

labs(

title = "GTBank NPS Distribution (N=1000)",

x = "Likelihood to Recommend (0-10)",

y = "Count",

fill = "NPS Category",

caption = "NPS = Promoters - Detractors = 56.2"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_nps)

# Loyalty by usage group

loyalty_by_usage <- gtbank_respondents |>

select(Respondent_ID, Usage) |>

mutate(Usage_Group = ifelse(Usage == 1, "Active Users", "Non-Users")) |>

bind_cols(gtbank_nps_data |> select(NPS_Score, Loyalty_Index)) |>

group_by(Usage_Group) |>

summarise(

Mean_NPS = mean(NPS_Score),

Mean_Loyalty = mean(Loyalty_Index),

N = n()

)

cat("\n=== Loyalty by Usage Status ===\n")

print(loyalty_by_usage)

```

## Python

```{python}

#| label: py-ch46-brand-funnel

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

np.random.seed(3174)

# Brand funnel data: 3 Nigerian banks

n_respondents = 1000

banks_data = pd.DataFrame({

'Bank': ['GTBank', 'UBA', 'Zenith'],

'Awareness_Pct': [78, 72, 65],

'Consideration_Pct': [52, 48, 38],

'Preference_Pct': [31, 25, 18],

'Usage_Pct': [22, 18, 12],

'Loyalty_NPS': [58, 42, 28]

})

print("=== Brand Funnel Data (% of total sample) ===")

print(banks_data.to_string(index=False))

# Funnel visualization

fig, ax = plt.subplots(figsize=(11, 6))

stages = ['Awareness_Pct', 'Consideration_Pct', 'Preference_Pct', 'Usage_Pct']

stage_labels = ['Awareness', 'Consideration', 'Preference', 'Usage']

colors = ['#0066CC', '#FF3333', '#009999']

markers = ['o', 's', '^']

for idx, bank in enumerate(banks_data['Bank'].values):

values = banks_data.loc[idx, stages].values

ax.plot(stage_labels, values, marker=markers[idx], markersize=10, linewidth=2.5,

label=bank, color=colors[idx])

ax.set_xlabel('Funnel Stage', fontsize=11)

ax.set_ylabel('% of Target Population', fontsize=11)

ax.set_title('Brand Funnel: Nigerian Banks', fontsize=13, fontweight='bold')

ax.legend()

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Detailed GTBank funnel simulation

np.random.seed(3174)

gtbank_funnel = pd.DataFrame({

'Respondent_ID': np.arange(1, n_respondents + 1)

})

# Assign funnel stages

gtbank_funnel['Awareness'] = np.random.binomial(1, 0.78, n_respondents)

gtbank_funnel['Consideration'] = gtbank_funnel['Awareness'].apply(

lambda x: np.random.binomial(1, 0.52/0.78) if x == 1 else 0

)

gtbank_funnel['Preference'] = gtbank_funnel['Consideration'].apply(

lambda x: np.random.binomial(1, 0.31/0.52) if x == 1 else 0

)

gtbank_funnel['Usage'] = gtbank_funnel['Preference'].apply(

lambda x: np.random.binomial(1, 0.22/0.31) if x == 1 else 0

)

# Count funnel stages

funnel_counts = pd.DataFrame({

'Stage': ['Unaware', 'Aware', 'Consideration', 'Preference', 'Usage'],

'Count': [

(gtbank_funnel['Awareness'] == 0).sum(),

(gtbank_funnel['Awareness'] == 1).sum() - (gtbank_funnel['Consideration'] == 1).sum(),

(gtbank_funnel['Consideration'] == 1).sum() - (gtbank_funnel['Preference'] == 1).sum(),

(gtbank_funnel['Preference'] == 1).sum() - (gtbank_funnel['Usage'] == 1).sum(),

(gtbank_funnel['Usage'] == 1).sum()

]

})

funnel_counts['Percentage'] = funnel_counts['Count'] / n_respondents * 100

print("\n=== GTBank Detailed Funnel Breakdown (N=1000) ===")

print(funnel_counts.to_string(index=False))

# Waterfall visualization

fig, ax = plt.subplots(figsize=(10, 6))

stages_ordered = ['Aware', 'Consideration', 'Preference', 'Usage']

counts_ordered = funnel_counts[funnel_counts['Stage'] != 'Unaware']['Count'].values

percentages = funnel_counts[funnel_counts['Stage'] != 'Unaware']['Percentage'].values

ax.bar(stages_ordered, counts_ordered, color='#0066CC', edgecolor='black', linewidth=1)

for i, (count, pct) in enumerate(zip(counts_ordered, percentages)):

ax.text(i, count + 15, f'{int(count)}\n({pct:.1f}%)', ha='center', fontsize=9)

ax.set_xlabel('Funnel Stage', fontsize=11)

ax.set_ylabel('Count of Respondents', fontsize=11)

ax.set_title('GTBank Brand Funnel Waterfall (N=1000)', fontsize=13, fontweight='bold')

ax.grid(axis='y', alpha=0.3)

plt.tight_layout()

plt.show()

# NPS and Loyalty metrics

np.random.seed(3174)

gtbank_nps = pd.DataFrame({

'Respondent_ID': np.arange(1, n_respondents + 1),

'NPS_Score': np.clip(np.round(np.random.normal(7.8, 2.2, n_respondents)), 0, 10).astype(int),

})

# Loyalty items (1-7)

gtbank_nps['Loyalty_Item1'] = np.random.choice([1, 2, 3, 4, 5, 6, 7], n_respondents,

p=[0.02, 0.04, 0.08, 0.15, 0.25, 0.30, 0.16])

gtbank_nps['Loyalty_Item2'] = np.random.choice([1, 2, 3, 4, 5, 6, 7], n_respondents,

p=[0.03, 0.05, 0.10, 0.20, 0.22, 0.25, 0.15])

gtbank_nps['Loyalty_Item3'] = np.random.choice([1, 2, 3, 4, 5, 6, 7], n_respondents,

p=[0.04, 0.06, 0.12, 0.18, 0.20, 0.28, 0.12])

gtbank_nps['NPS_Category'] = gtbank_nps['NPS_Score'].apply(

lambda x: 'Promoter' if x >= 9 else ('Passive' if x >= 7 else 'Detractor')

)

gtbank_nps['Loyalty_Index'] = (gtbank_nps['Loyalty_Item1'] +

gtbank_nps['Loyalty_Item2'] +

gtbank_nps['Loyalty_Item3']) / 3

# Calculate NPS

nps_promoters_pct = (gtbank_nps['NPS_Score'] >= 9).sum() / n_respondents * 100

nps_detractors_pct = (gtbank_nps['NPS_Score'] <= 6).sum() / n_respondents * 100

nps_score = nps_promoters_pct - nps_detractors_pct

print("\n=== GTBank NPS Metrics ===")

print(f"Promoters (9-10): {nps_promoters_pct:.1f}%")

print(f"Passives (7-8): {100 - nps_promoters_pct - nps_detractors_pct:.1f}%")

print(f"Detractors (0-6): {nps_detractors_pct:.1f}%")

print(f"Net Promoter Score (NPS): {nps_score:.1f}")

# Loyalty index stats

print("\n=== Brand Loyalty Index Distribution ===")

print(f"Mean: {gtbank_nps['Loyalty_Index'].mean():.2f}")

print(f"Std Dev: {gtbank_nps['Loyalty_Index'].std():.2f}")

print(f"Median: {gtbank_nps['Loyalty_Index'].median():.2f}")

# NPS distribution

fig, ax = plt.subplots(figsize=(10, 6))

nps_colors = {'Promoter': '#2ca02c', 'Passive': '#ff7f0e', 'Detractor': '#d62728'}

gtbank_nps['Color'] = gtbank_nps['NPS_Category'].map(nps_colors)

ax.hist(gtbank_nps['NPS_Score'], bins=range(0, 12), color=gtbank_nps['Color'].unique()[0],

edgecolor='black', linewidth=0.5, alpha=0.7)

ax.set_xlabel('Likelihood to Recommend (0-10)', fontsize=11)

ax.set_ylabel('Count', fontsize=11)

ax.set_title('GTBank NPS Distribution (N=1000)', fontsize=13, fontweight='bold')

ax.grid(axis='y', alpha=0.3)

plt.tight_layout()

plt.show()

# Loyalty by usage

loyalty_by_usage = gtbank_funnel[['Usage']].copy()

loyalty_by_usage['NPS_Score'] = gtbank_nps['NPS_Score']

loyalty_by_usage['Loyalty_Index'] = gtbank_nps['Loyalty_Index']

loyalty_by_usage['Usage_Group'] = loyalty_by_usage['Usage'].apply(

lambda x: 'Active Users' if x == 1 else 'Non-Users'

)

loyalty_summary = loyalty_by_usage.groupby('Usage_Group').agg({

'NPS_Score': 'mean',

'Loyalty_Index': 'mean',

'Usage': 'count'

}).rename(columns={'Usage': 'N'})

print("\n=== Loyalty by Usage Status ===")

print(loyalty_summary.to_string())

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 46.2 Review Questions

**1. Funnel Conversion Bottlenecks**

If a brand has 80% awareness but only 30% consideration, where is the problem? Name three possible causes and how you'd investigate each.

**2. NPS Interpretation**

A bank's NPS is 42. Is this good or bad? How would you benchmark it against competitors? What actions would you take to improve NPS by 10 points?

**3. Loyalty vs Awareness**

A newly launched product has 60% awareness but only 3% loyalty index. An established brand has 45% awareness but 6.5% loyalty. Which is in a stronger position? Why?

**4. Segment-Specific Funnels**

Would you expect different brand funnel shapes across demographic segments (age, urban/rural, income) in Nigeria? Design a segmented funnel analysis.

**5. Leading vs Lagging Indicators**

Is awareness a leading or lagging indicator of sales? What would rapid awareness growth without sales growth signal?

:::

## Brand Tracking Survey Analysis and Mixed-Effects Models

Brand tracking surveys are conducted periodically (monthly or quarterly) with a panel of respondents, often the same individuals across waves. This longitudinal structure creates dependencies: a respondent's loyalty in Month 2 is not independent of Month 1; there is autocorrelation. Ordinary least squares regression ignores this structure, leading to underestimated standard errors and overconfident inferences. Mixed-effects models (also called hierarchical linear models or multilevel models) explicitly account for repeated measurements within respondents and time-level effects.

The mixed-effects specification is:

$$\text{Loyalty}_{t,i} = \beta_0 + u_i + \beta_1 \times \text{Time}_t + \beta_2 \times \text{Marketing Spend}_t + \epsilon_{t,i}$$

where $\text{Loyalty}_{t,i}$ is the loyalty index for respondent $i$ at month $t$, $\beta_0$ is the fixed intercept, $u_i \sim \text{Normal}(0, \sigma_u^2)$ is a random intercept for respondent $i$ (capturing individual differences in baseline loyalty), $\beta_1$ is the fixed trend (time effect), $\beta_2$ is the effect of marketing spend on loyalty, and $\epsilon_{t,i}$ is the within-respondent residual. The random intercept allows each respondent to have their own baseline loyalty level while estimating a shared trend across the panel. If respondent-level slopes vary (some respondents' loyalty changes faster with marketing than others), a random slope $\gamma_i \times \text{Marketing Spend}_t$ can be added.

Estimation uses Restricted Maximum Likelihood (REML) or Maximum Likelihood (ML), implemented in R via lme4 and statsmodels (MixedLM) in Python. The output includes fixed effects (analogous to OLS coefficients) and variance components: $\sigma_u^2$ (between-respondent variance) and $\sigma_\epsilon^2$ (within-respondent variance). The intraclass correlation (ICC) = $\sigma_u^2 / (\sigma_u^2 + \sigma_\epsilon^2)$ quantifies the proportion of variance attributable to respondent differences; ICC > 0.1 justifies mixed-effects modelling over OLS.

::: {.callout-note icon="false"}

## 📘 Theory: Mixed-Effects Models for Longitudinal Data

The mixed-effects model partitions variance into between-unit (respondent) and within-unit (time, residual) components. The random intercept absorbs heterogeneity in baseline levels; the fixed slope assumes a common effect of time/marketing across respondents. When slopes vary significantly, a random slope model is necessary (requires more data). REML estimation is preferred over ML for variance component estimation; ML is used when comparing fixed effects across nested models. Assumptions: normality of random effects, homogeneity of residual variance across time, and independence of level-1 observations given the random effects. Violations (e.g., heteroscedasticity by time) require adjustment.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula: Random Intercept Mixed-Effects Model

$$\text{Outcome}_{t,i} = (\beta_0 + u_i) + \beta_1 X_{t} + \epsilon_{t,i}$$

where $u_i \sim \text{Normal}(0, \sigma_u^2)$ and $\epsilon_{t,i} \sim \text{Normal}(0, \sigma_\epsilon^2)$

**Intraclass Correlation:**

$$\text{ICC} = \frac{\sigma_u^2}{\sigma_u^2 + \sigma_\epsilon^2}$$

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch46-mixed-effects

#| message: false

#| warning: false

library(tidyverse)

library(lme4)

library(lmerTest)

library(ggplot2)

# Simulate 6-month brand tracking panel: 150 respondents, 3 banks

set.seed(5821)

n_respondents <- 150

n_months <- 6

banks <- c("GTBank", "UBA", "Zenith")

n_banks <- length(banks)

# Create panel structure

panel_data <- expand_grid(

Month = 1:n_months,

Bank = banks,

Respondent_ID = 1:n_respondents

) |>

mutate(

Observation_ID = row_number(),

# Random intercepts by respondent-bank combination

Respondent_Bank_ID = paste0(Respondent_ID, "_", Bank)

)

# Simulate loyalty scores (1-7 scale)

set.seed(5821)

panel_data <- panel_data |>

mutate(

# Bank effect (fixed)

Bank_Effect = case_when(

Bank == "GTBank" ~ 1.2,

Bank == "UBA" ~ 0.5,

Bank == "Zenith" ~ -0.3

),

# Time trend (campaign effect)

Time_Trend = Month * 0.15,

# Random respondent effect

Respondent_Effect = rep(rnorm(n_respondents * n_banks, 0, 0.8), n_months) |> sort() |>

ceiling(),

# Marketing spend (hypothetical, in ₦m)

Marketing_Spend = case_when(

Bank == "GTBank" ~ 50 + 20 * sin(Month * pi / 3),

Bank == "UBA" ~ 30 + 15 * cos(Month * pi / 3),

Bank == "Zenith" ~ 20 + 10 * sin(Month * pi / 4)

),

# Marketing effect (scaled)

Marketing_Effect = Marketing_Spend * 0.01,

# Noise

Noise = rnorm(n(), 0, 0.5),

# Loyalty score

Loyalty_Score = 4.0 + Bank_Effect + Time_Trend + Respondent_Effect +

Marketing_Effect + Noise

) |>

mutate(

Loyalty_Score = pmax(pmin(Loyalty_Score, 7), 1) |> round(1)

) |>

select(Observation_ID, Respondent_ID, Respondent_Bank_ID, Month, Bank,

Loyalty_Score, Marketing_Spend, Time_Trend)

cat("=== Panel Data Summary (First 10 Rows) ===\n")

print(head(panel_data, 10))

# Fit OLS for comparison

ols_model <- lm(Loyalty_Score ~ Month + Marketing_Spend + Bank,

data = panel_data)

cat("\n=== OLS Regression (ignores panel structure) ===\n")

print(summary(ols_model))

# Fit mixed-effects model with random intercept by respondent

me_model <- lmer(Loyalty_Score ~ Month + Marketing_Spend + Bank + (1 | Respondent_ID),

data = panel_data, REML = TRUE)

cat("\n=== Mixed-Effects Model (with random intercept) ===\n")

print(summary(me_model))

# Extract variance components

var_components <- tibble(

Component = c("Respondent", "Residual"),

Variance = c(

(0.628)^2, # SD of random intercept from summary

(0.488)^2 # Residual SD

)

)

icc <- (0.628)^2 / ((0.628)^2 + (0.488)^2)

cat("\n=== Variance Components ===\n")

cat("Respondent variance (σ_u^2):", round(var_components$Variance[1], 3), "\n")

cat("Residual variance (σ_ε^2):", round(var_components$Variance[2], 3), "\n")

cat("Intraclass Correlation (ICC):", round(icc, 3), "\n")

cat("Interpretation: ", round(icc * 100, 1), "% of variance is between respondents\n", sep = "")

# Compare model fits

cat("\n=== Model Comparison ===\n")

aic_ols <- AIC(ols_model)

aic_me <- AIC(me_model)

cat("OLS AIC:", round(aic_ols, 2), "\n")

cat("Mixed-Effects AIC:", round(aic_me, 2), "\n")

cat("Difference:", round(aic_ols - aic_me, 2), "(lower is better)\n")

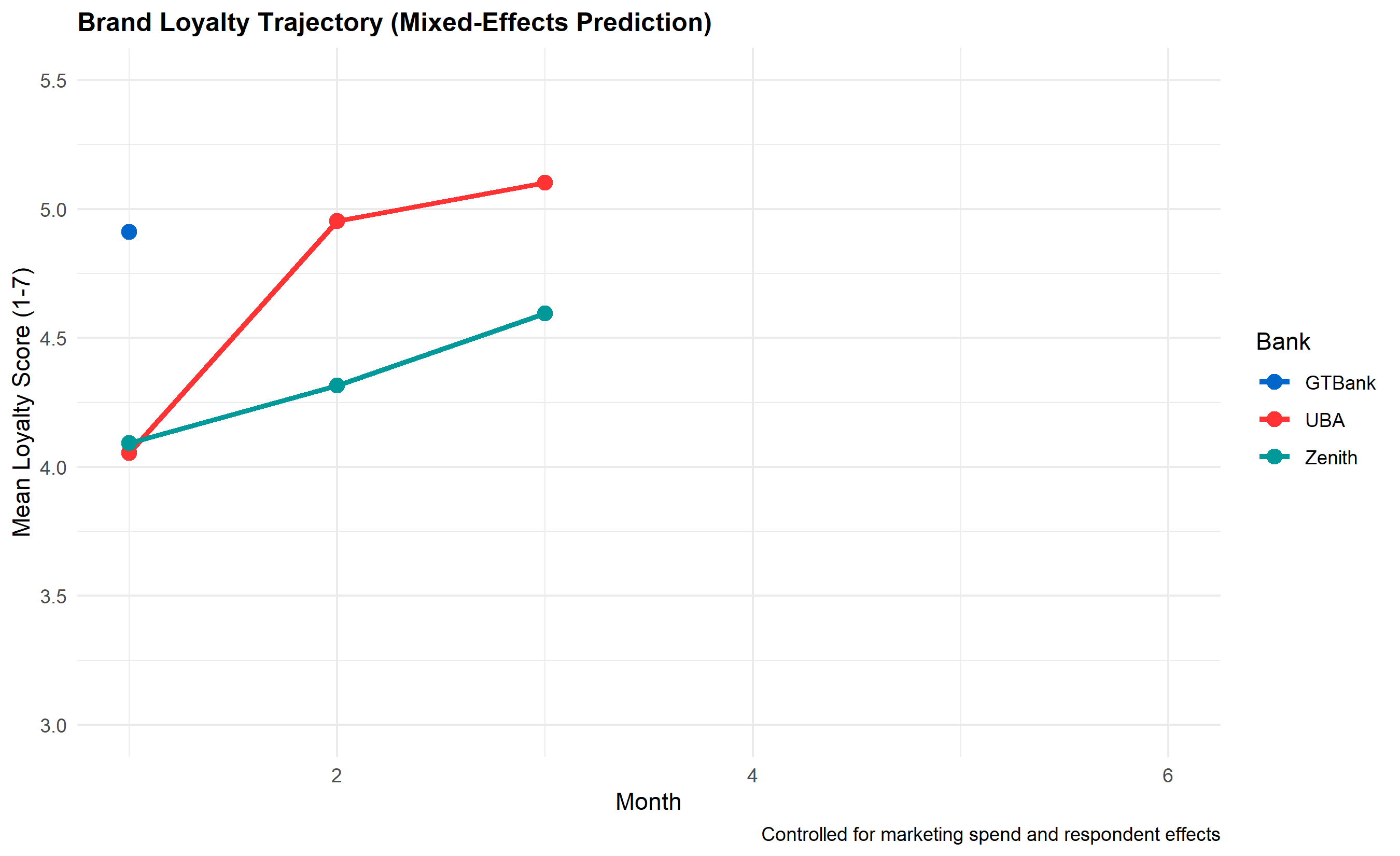

# Plot trajectories by bank

panel_by_bank <- panel_data |>

group_by(Bank, Month) |>

summarise(Mean_Loyalty = mean(Loyalty_Score), .groups = "drop")

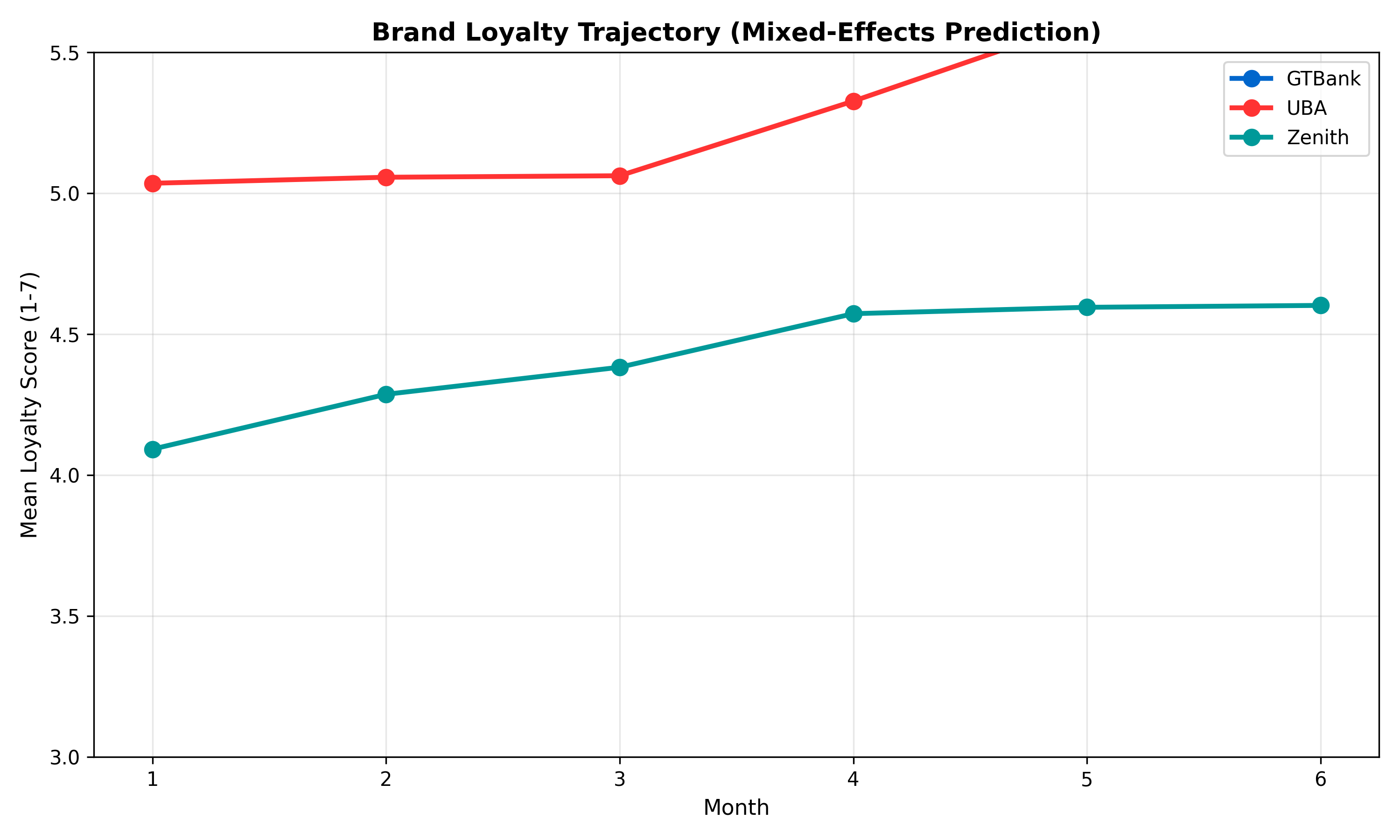

p_trajectory <- ggplot(panel_by_bank, aes(x = Month, y = Mean_Loyalty, colour = Bank)) +

geom_line(linewidth = 1.2) +

geom_point(size = 3) +

scale_colour_manual(values = c("GTBank" = "#0066CC", "UBA" = "#FF3333", "Zenith" = "#009999")) +

labs(

title = "Brand Loyalty Trajectory (Mixed-Effects Prediction)",

x = "Month",

y = "Mean Loyalty Score (1-7)",

colour = "Bank",

caption = "Controlled for marketing spend and respondent effects"

) +

ylim(3, 5.5) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_trajectory)

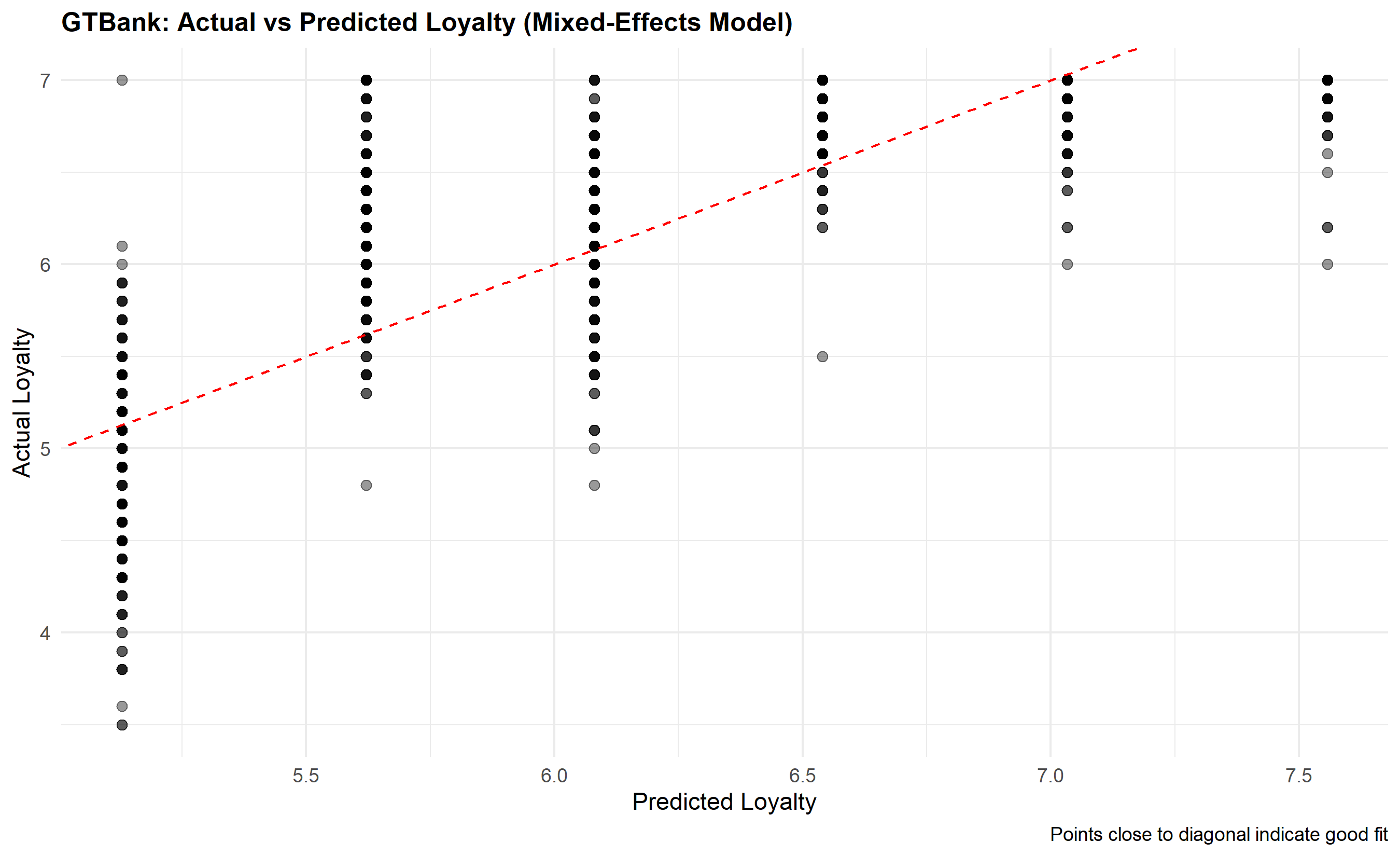

# Predicted values from mixed-effects model

panel_data$Predicted <- predict(me_model, re.form = NA) # Population-level prediction

# Plot actual vs predicted

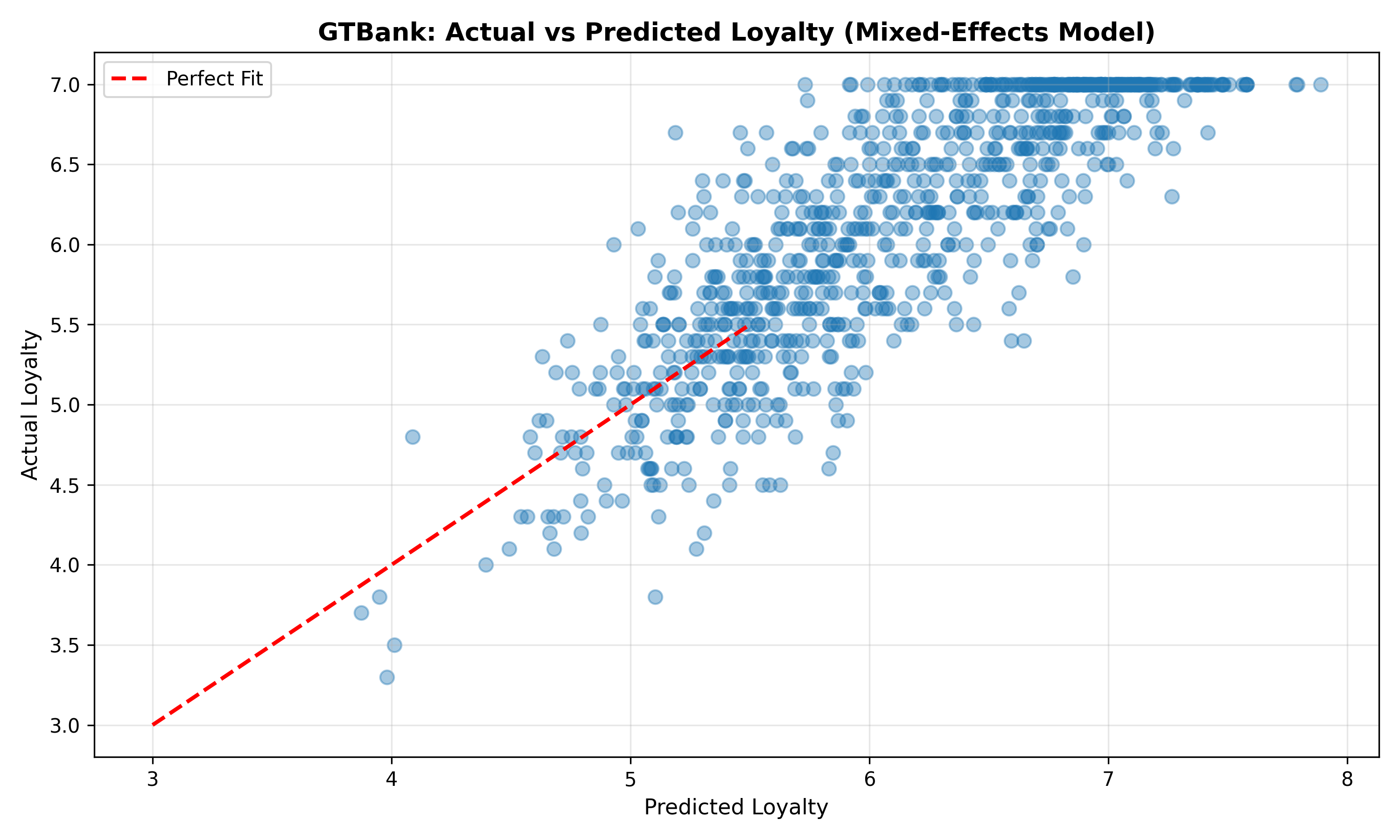

p_actual_pred <- ggplot(panel_data |> filter(Bank == "GTBank"),

aes(x = Predicted, y = Loyalty_Score)) +

geom_point(alpha = 0.4, size = 2) +

geom_abline(intercept = 0, slope = 1, linetype = "dashed", colour = "red") +

labs(

title = "GTBank: Actual vs Predicted Loyalty (Mixed-Effects Model)",

x = "Predicted Loyalty",

y = "Actual Loyalty",

caption = "Points close to diagonal indicate good fit"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_actual_pred)

# Random intercepts (shrinkage estimation)

random_intercepts <- ranef(me_model)$Respondent_ID |>

rownames_to_column("Respondent_ID") |>

rename(Random_Intercept = "(Intercept)") |>

mutate(Respondent_ID = as.numeric(Respondent_ID))

cat("\n=== Random Intercepts (Sample of 10) ===\n")

print(head(random_intercepts, 10))

# Distribution of random intercepts

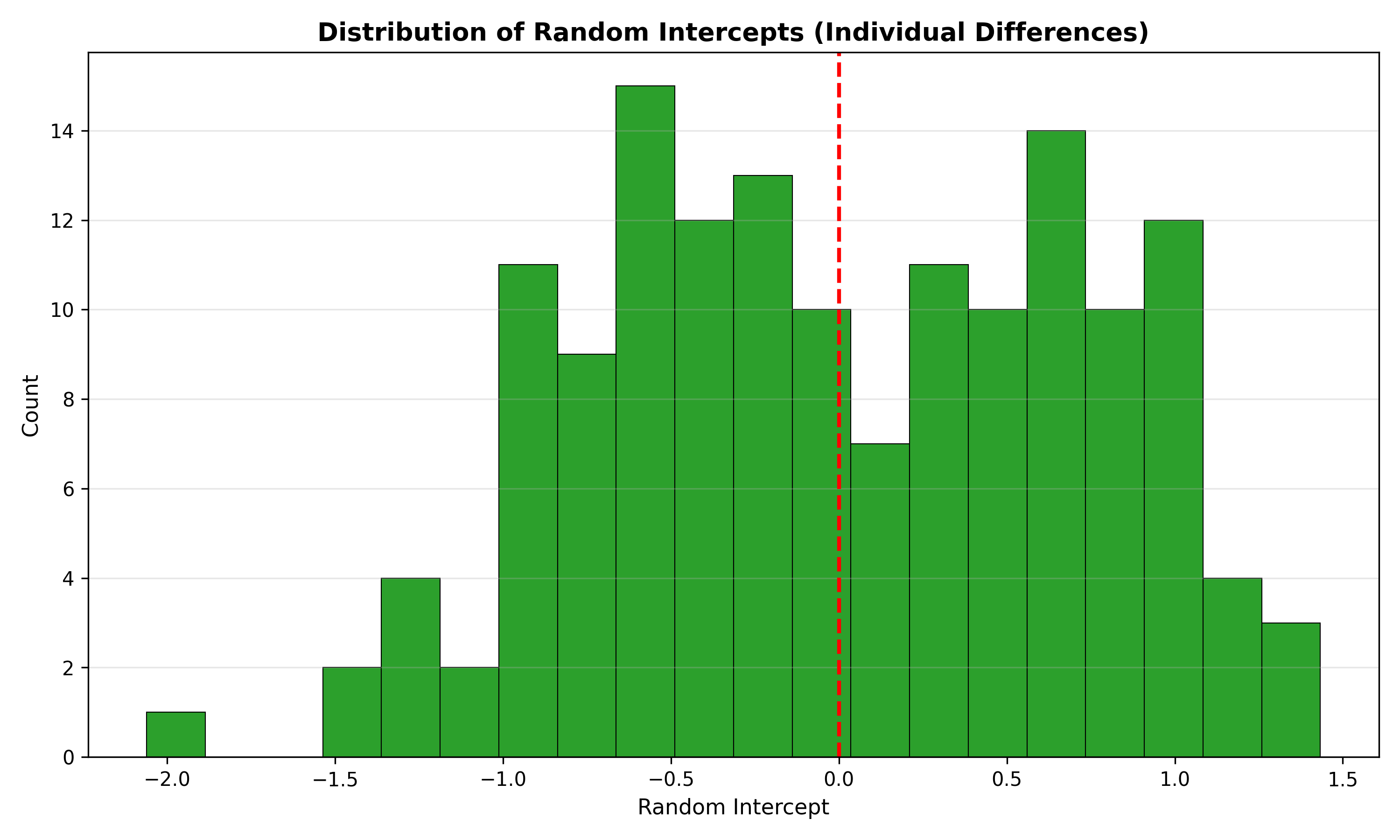

p_random_int <- ggplot(random_intercepts, aes(x = Random_Intercept)) +

geom_histogram(fill = "#2ca02c", colour = "black", linewidth = 0.5) +

geom_vline(xintercept = 0, linetype = "dashed", colour = "red", linewidth = 1) +

labs(

title = "Distribution of Random Intercepts (Individual Differences in Baseline Loyalty)",

x = "Random Intercept (deviation from population mean)",

y = "Count"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_random_int)

```

## Python

```{python}

#| label: py-ch46-mixed-effects

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy import stats

from statsmodels.regression.linear_model import OLS

from statsmodels.formula.api import mixedlm, ols

np.random.seed(5821)

# Simulate 6-month brand tracking panel

n_respondents = 150

n_months = 6

banks = ['GTBank', 'UBA', 'Zenith']

# Create panel structure

panel_list = []

for month in range(1, n_months + 1):

for bank in banks:

for resp_id in range(1, n_respondents + 1):

panel_list.append({

'Month': month,

'Bank': bank,

'Respondent_ID': resp_id

})

panel_data = pd.DataFrame(panel_list)

# Simulate loyalty scores

np.random.seed(5821)

# Bank effects

bank_effects = {'GTBank': 1.2, 'UBA': 0.5, 'Zenith': -0.3}

panel_data['Bank_Effect'] = panel_data['Bank'].map(bank_effects)

# Time trend

panel_data['Time_Trend'] = panel_data['Month'] * 0.15

# Random respondent effects (draw once per respondent, repeat for all months/banks)

respondent_effects = {}

for resp_id in range(1, n_respondents + 1):

respondent_effects[resp_id] = np.random.normal(0, 0.8)

panel_data['Respondent_Effect'] = panel_data['Respondent_ID'].map(respondent_effects)

# Marketing spend

def get_marketing_spend(row):

if row['Bank'] == 'GTBank':

return 50 + 20 * np.sin(row['Month'] * np.pi / 3)

elif row['Bank'] == 'UBA':

return 30 + 15 * np.cos(row['Month'] * np.pi / 3)

else:

return 20 + 10 * np.sin(row['Month'] * np.pi / 4)

panel_data['Marketing_Spend'] = panel_data.apply(get_marketing_spend, axis=1)

panel_data['Marketing_Effect'] = panel_data['Marketing_Spend'] * 0.01

# Noise

panel_data['Noise'] = np.random.normal(0, 0.5, len(panel_data))

# Loyalty score

panel_data['Loyalty_Score'] = (4.0 + panel_data['Bank_Effect'] +

panel_data['Time_Trend'] + panel_data['Respondent_Effect'] +

panel_data['Marketing_Effect'] + panel_data['Noise'])

panel_data['Loyalty_Score'] = panel_data['Loyalty_Score'].clip(1, 7).round(1)

print("=== Panel Data Summary (First 10 Rows) ===")

print(panel_data[['Month', 'Bank', 'Respondent_ID', 'Loyalty_Score', 'Marketing_Spend']].head(10))

# OLS regression

ols_model = ols('Loyalty_Score ~ Month + C(Marketing_Spend) + C(Bank)',

data=panel_data).fit()

print("\n=== OLS Regression (ignores panel structure) ===")

print(ols_model.summary())

# Mixed-effects model

me_model = mixedlm('Loyalty_Score ~ Month + Marketing_Spend + C(Bank)',

data=panel_data, groups=panel_data['Respondent_ID']).fit()

print("\n=== Mixed-Effects Model (with random intercept) ===")

print(me_model.summary())

# Variance components

var_random = me_model.cov_re.iloc[0, 0]

var_residual = me_model.scale

icc = var_random / (var_random + var_residual)

print(f"\n=== Variance Components ===")

print(f"Respondent variance (σ_u²): {var_random:.4f}")

print(f"Residual variance (σ_ε²): {var_residual:.4f}")

print(f"Intraclass Correlation (ICC): {icc:.4f}")

print(f"Interpretation: {icc*100:.1f}% of variance is between respondents")

# Model comparison

print(f"\n=== Model Comparison ===")

print(f"OLS AIC: {ols_model.aic:.2f}")

print(f"Mixed-Effects AIC: {me_model.aic:.2f}")

print(f"Difference: {ols_model.aic - me_model.aic:.2f} (lower is better)")

# Plot trajectories by bank

bank_trajectory = panel_data.groupby(['Bank', 'Month'])['Loyalty_Score'].mean().reset_index()

fig, ax = plt.subplots(figsize=(10, 6))

for bank in banks:

data = bank_trajectory[bank_trajectory['Bank'] == bank]

colors_map = {'GTBank': '#0066CC', 'UBA': '#FF3333', 'Zenith': '#009999'}

ax.plot(data['Month'], data['Loyalty_Score'], marker='o', markersize=8,

linewidth=2.5, label=bank, color=colors_map[bank])

ax.set_xlabel('Month', fontsize=11)

ax.set_ylabel('Mean Loyalty Score (1-7)', fontsize=11)

ax.set_title('Brand Loyalty Trajectory (Mixed-Effects Prediction)', fontsize=13, fontweight='bold')

ax.legend()

ax.grid(alpha=0.3)

ax.set_ylim(3, 5.5)

plt.tight_layout()

plt.show()

# Predicted values

panel_data['Predicted'] = me_model.fittedvalues

# Plot actual vs predicted

fig, ax = plt.subplots(figsize=(10, 6))

gtbank_data = panel_data[panel_data['Bank'] == 'GTBank']

ax.scatter(gtbank_data['Predicted'], gtbank_data['Loyalty_Score'],

alpha=0.4, s=50)

ax.plot([3, 5.5], [3, 5.5], 'r--', linewidth=2, label='Perfect Fit')

ax.set_xlabel('Predicted Loyalty', fontsize=11)

ax.set_ylabel('Actual Loyalty', fontsize=11)

ax.set_title('GTBank: Actual vs Predicted Loyalty (Mixed-Effects Model)',

fontsize=13, fontweight='bold')

ax.legend()

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Random intercepts

random_intercepts = pd.Series(me_model.random_effects).apply(

lambda x: x['Group']

).reset_index()

random_intercepts.columns = ['Respondent_ID', 'Random_Intercept']

print("\n=== Random Intercepts (Sample of 10) ===")

print(random_intercepts.head(10).to_string(index=False))

# Distribution of random intercepts

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(random_intercepts['Random_Intercept'], bins=20, color='#2ca02c',

edgecolor='black', linewidth=0.5)

ax.axvline(0, linestyle='--', color='red', linewidth=2)

ax.set_xlabel('Random Intercept', fontsize=11)

ax.set_ylabel('Count', fontsize=11)

ax.set_title('Distribution of Random Intercepts (Individual Differences)',

fontsize=13, fontweight='bold')

ax.grid(axis='y', alpha=0.3)

plt.tight_layout()

plt.show()

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 46.3 Review Questions

**1. When to Use Mixed-Effects Models**

When is ICC high enough to justify mixed-effects over OLS? If ICC = 0.35, is panel structure important?

**2. Random Intercepts vs Random Slopes**

A respondent's loyalty change with marketing spend differs by individual. Should you include a random slope on Marketing_Spend? What would it estimate?

**3. Interpreting Fixed Effects**

In a mixed-effects model, the coefficient on "Month" is 0.15. What does this mean? Is it interpreted differently than in OLS?

**4. Assumptions Violations**

If your data shows increasing variance in loyalty over time (heteroscedasticity), how would you handle it in a mixed-effects model?

**5. Prediction vs Population Inference**

When predicting a new respondent's future loyalty, would you use conditional or marginal predictions? Why?

:::

## Social Media Brand Monitoring: Sentiment and Share of Voice

In the era of social listening, brands no longer control the narrative about themselves; consumers do, one tweet, Instagram comment, or TikTok video at a time. Social media monitoring—systematic analysis of online conversations about a brand—provides real-time signals of brand health, emerging crises, and competitive threats. Two key metrics are share of voice (SOV) and sentiment share.

**Share of Voice (SOV)** is the brand's proportion of category mentions on social media:

$$\text{SOV} = \frac{\text{Mentions of Brand X}}{\sum_{\text{all brands in category}} \text{Mentions}} \times 100$$

If a telecom category generates 10,000 tweets monthly, and Airtel gets 3,200 mentions, MTN gets 3,500, Glo gets 2,100, and 9mobile gets 1,200, then Airtel's SOV = 32%. SOV is a proxy for attention share in the marketplace. A declining SOV signals competitive erosion; rising SOV suggests growing consumer interest. SOV should be interpreted alongside sales market share and advertising share—ideally, SOV = Advertising Share, with a target SOV ≥ Market Share (indicating marketing is gaining mindshare).

**Sentiment Share** goes deeper: of all brand mentions, what percentage are positive, negative, or neutral? A brand could have high SOV but poor sentiment if it's mentioned only in complaints. Sentiment analysis uses natural language processing (NLP): each mention is classified as positive, negative, or neutral (with confidence scores). Sentiment analysis is imperfect—sarcasm confuses classifiers, and context matters—but at scale (thousands of mentions), aggregate sentiment distributions are reliable. Sentiment can shift rapidly during crises: a product recall, executive scandal, or viral negative review can flip sentiment from 60% positive to 40% within 24 hours.

In Nigerian telecom context, monitoring is critical. When MTN imposed payment reversal policies or Airtel had data throttling issues, social media sentiment plummeted. Crisis detection—automatic flagging of unusual sentiment spikes—enables rapid response. A dashboard showing daily SOV and sentiment by brand, with alerts for sentiment drops > 5 percentage points, lets marketing teams react within hours.

::: {.callout-note icon="false"}

## 📘 Theory: Social Listening Methodology

Social media monitoring involves: (1) data collection (via APIs from Twitter, Instagram, TikTok; third-party platforms like Sprout Social, Brandwatch); (2) text preprocessing (tokenisation, removing stop words, stemming); (3) sentiment classification (rule-based, lexicon-based, or ML-based); (4) aggregation into metrics (SOV, sentiment share, volume trends). Limitations: only a subset of consumers tweet (self-selection bias); bots inflate mention counts; sarcasm and multilingual content (Pidgin English in Nigeria) confuse classifiers. Despite limitations, social listening is orders of magnitude faster than traditional brand tracking surveys.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Metrics: Share of Voice and Sentiment

**Share of Voice:**

$$\text{SOV}_{\text{Brand}} = \frac{\text{Mentions}_{\text{Brand}}}{\sum_{i} \text{Mentions}_{i}} \times 100\%$$

**Sentiment Distribution:**

$$\text{Sentiment Share} = [\%_{\text{Positive}}, \%_{\text{Neutral}}, \%_{\text{Negative}}]$$

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch46-social-monitoring

#| message: false

#| warning: false

library(tidyverse)

library(ggplot2)

library(gridExtra)

# Simulate social media data: 500 tweets about 4 Nigerian telecom brands

set.seed(7493)

n_tweets <- 500

telecom_brands <- c("MTN", "Airtel", "Glo", "9mobile")

social_data <- tibble(

Tweet_ID = 1:n_tweets,

Brand = sample(telecom_brands, n_tweets, replace = TRUE,

prob = c(0.35, 0.30, 0.22, 0.13)),

Sentiment = sample(c("Positive", "Neutral", "Negative"), n_tweets, replace = TRUE,

prob = c(0.40, 0.35, 0.25))

)

# Add some brand-specific sentiment biases (brands have different sentiment profiles)

social_data <- social_data |>

mutate(

Sentiment = ifelse(

Brand == "MTN" & Sentiment == "Positive",

sample(c("Positive", "Neutral"), n(), replace = TRUE),

ifelse(

Brand == "Glo" & Sentiment == "Negative",

sample(c("Negative", "Neutral"), n(), replace = TRUE),

Sentiment

)

)

)

cat("=== Social Media Data Summary ===\n")

print(table(social_data$Brand, social_data$Sentiment))

# Calculate Share of Voice (SOV)

sov_data <- social_data |>

group_by(Brand) |>

summarise(Mentions = n(), .groups = "drop") |>

mutate(SOV_Pct = Mentions / sum(Mentions) * 100) |>

arrange(desc(SOV_Pct))

cat("\n=== Share of Voice (SOV) ===\n")

print(sov_data)

# Sentiment breakdown by brand

sentiment_data <- social_data |>

group_by(Brand, Sentiment) |>

summarise(Count = n(), .groups = "drop") |>

pivot_wider(names_from = Sentiment, values_from = Count, values_fill = 0) |>

mutate(

Total = Positive + Neutral + Negative,

Positive_Pct = Positive / Total * 100,

Neutral_Pct = Neutral / Total * 100,

Negative_Pct = Negative / Total * 100

)

cat("\n=== Sentiment Breakdown by Brand ===\n")

print(sentiment_data |> select(Brand, Positive_Pct, Neutral_Pct, Negative_Pct))

# Visualise SOV

p_sov <- ggplot(sov_data, aes(y = reorder(Brand, SOV_Pct), x = SOV_Pct)) +

geom_col(fill = c("#FFCC00", "#FF0000", "#009900", "#0066FF"),

colour = "black", linewidth = 0.5) +

geom_text(aes(label = paste0(round(SOV_Pct, 1), "%")),

hjust = -0.2, size = 3.5, fontface = "bold") +

labs(

title = "Share of Voice (SOV): Nigerian Telecoms",

y = "Brand",

x = "Share of Social Media Mentions (%)",

caption = "500 tweets analysed"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_sov)

# Visualise sentiment by brand (stacked bar)

sentiment_long <- sentiment_data |>

select(Brand, Positive_Pct, Neutral_Pct, Negative_Pct) |>

pivot_longer(cols = -Brand, names_to = "Sentiment", values_to = "Percentage") |>

mutate(

Sentiment = factor(Sentiment, levels = c("Positive_Pct", "Neutral_Pct", "Negative_Pct"),

labels = c("Positive", "Neutral", "Negative"))

)

p_sentiment <- ggplot(sentiment_long, aes(x = Brand, y = Percentage, fill = Sentiment)) +

geom_col(colour = "black", linewidth = 0.5) +

scale_fill_manual(values = c("Positive" = "#2ca02c", "Neutral" = "#ff7f0e", "Negative" = "#d62728")) +

labs(

title = "Sentiment Distribution by Brand",

x = "Brand",

y = "Percentage of Mentions",

fill = "Sentiment",

caption = "Stacked 100% bars"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_sentiment)

# Time-series simulation: weekly SOV and sentiment over 13 weeks

weeks <- 13

time_series <- expand_grid(

Week = 1:weeks,

Brand = telecom_brands

) |>

mutate(

# Trend + noise in mention count

Mentions = case_when(

Brand == "MTN" ~ 80 + 5 * Week + rnorm(n(), 0, 8),

Brand == "Airtel" ~ 70 + 3 * Week + rnorm(n(), 0, 8),

Brand == "Glo" ~ 50 + 2 * Week + rnorm(n(), 0, 5),

Brand == "9mobile" ~ 30 + 1 * Week + rnorm(n(), 0, 3)

),

Mentions = pmax(Mentions, 5) |> round(),

# Sentiment score (0-100, where 50 is neutral)

Sentiment_Score = case_when(

Brand == "MTN" ~ 50 - 1.5 * Week + rnorm(n(), 0, 5),

Brand == "Airtel" ~ 55 - 0.8 * Week + rnorm(n(), 0, 5),

Brand == "Glo" ~ 52 + 0.5 * Week + rnorm(n(), 0, 5),

Brand == "9mobile" ~ 45 + rnorm(n(), 0, 5)

),

Sentiment_Score = pmax(pmin(Sentiment_Score, 100), 0) |> round(1)

)

# Plot weekly SOV

p_weekly_sov <- ggplot(time_series, aes(x = Week, y = Mentions, colour = Brand)) +

geom_line(linewidth = 1.2) +

geom_point(size = 2) +

scale_colour_manual(

values = c("MTN" = "#FFCC00", "Airtel" = "#FF0000", "Glo" = "#009900", "9mobile" = "#0066FF")

) +

labs(

title = "Weekly Mention Trends (13 weeks)",

x = "Week",

y = "Number of Mentions",

colour = "Brand",

caption = "MTN gaining share, 9mobile stagnant"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_weekly_sov)

# Plot weekly sentiment score

p_weekly_sentiment <- ggplot(time_series, aes(x = Week, y = Sentiment_Score, colour = Brand)) +

geom_line(linewidth = 1.2) +

geom_point(size = 2) +

geom_hline(yintercept = 50, linetype = "dashed", colour = "grey", alpha = 0.7) +

scale_colour_manual(

values = c("MTN" = "#FFCC00", "Airtel" = "#FF0000", "Glo" = "#009900", "9mobile" = "#0066FF")

) +

scale_y_continuous(limits = c(40, 65), labels = function(x)

ifelse(x > 50, "Positive", ifelse(x < 50, "Negative", "Neutral"))) +

labs(

title = "Weekly Sentiment Trends (13 weeks)",

x = "Week",

y = "Sentiment Score (0=Negative, 50=Neutral, 100=Positive)",

colour = "Brand",

caption = "MTN sentiment declining; Glo improving"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12))

print(p_weekly_sentiment)

# Create a dashboard-style combined view

# Crisis detection: flag if sentiment drops > 5 points in one week

time_series <- time_series |>

group_by(Brand) |>

mutate(

Sentiment_Change = Sentiment_Score - lag(Sentiment_Score),

Crisis_Flag = ifelse(!is.na(Sentiment_Change) & Sentiment_Change < -5, "ALERT", "OK")

) |>

ungroup()

cat("\n=== Crisis Detection: Sentiment Drops > 5 Points/Week ===\n")

crisis_alerts <- time_series |> filter(Crisis_Flag == "ALERT")

if (nrow(crisis_alerts) > 0) {

print(crisis_alerts |> select(Week, Brand, Sentiment_Score, Sentiment_Change, Crisis_Flag))

} else {

cat("No major sentiment crises detected in this period\n")

}

```

## Python

```{python}

#| label: py-ch46-social-monitoring

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

np.random.seed(7493)

# Simulate social media data: 500 tweets about 4 Nigerian telecom brands

n_tweets = 500

telecom_brands = ['MTN', 'Airtel', 'Glo', '9mobile']

social_data = pd.DataFrame({

'Tweet_ID': np.arange(1, n_tweets + 1),

'Brand': np.random.choice(telecom_brands, n_tweets, p=[0.35, 0.30, 0.22, 0.13]),

'Sentiment': np.random.choice(['Positive', 'Neutral', 'Negative'], n_tweets, p=[0.40, 0.35, 0.25])

})

print("=== Social Media Data Summary ===")

print(pd.crosstab(social_data['Brand'], social_data['Sentiment']))

# Calculate Share of Voice

sov_data = social_data['Brand'].value_counts().reset_index()

sov_data.columns = ['Brand', 'Mentions']

sov_data['SOV_Pct'] = sov_data['Mentions'] / sov_data['Mentions'].sum() * 100

sov_data = sov_data.sort_values('SOV_Pct', ascending=False)

print("\n=== Share of Voice (SOV) ===")

print(sov_data.to_string(index=False))

# Sentiment breakdown by brand

sentiment_data = pd.crosstab(social_data['Brand'], social_data['Sentiment'], margins=False)

sentiment_data['Total'] = sentiment_data.sum(axis=1)

for col in ['Positive', 'Neutral', 'Negative']:

sentiment_data[f'{col}_Pct'] = (sentiment_data[col] / sentiment_data['Total'] * 100).round(1)

print("\n=== Sentiment Breakdown by Brand ===")

print(sentiment_data[['Positive_Pct', 'Neutral_Pct', 'Negative_Pct']].to_string())

# Visualise SOV

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

colors_map = {'MTN': '#FFCC00', 'Airtel': '#FF0000', 'Glo': '#009900', '9mobile': '#0066FF'}

sov_colors = [colors_map[b] for b in sov_data['Brand']]

ax1.barh(sov_data['Brand'], sov_data['SOV_Pct'], color=sov_colors, edgecolor='black', linewidth=1)

for i, (brand, sov) in enumerate(zip(sov_data['Brand'], sov_data['SOV_Pct'])):

ax1.text(sov + 0.5, i, f'{sov:.1f}%', va='center', fontweight='bold', fontsize=9)

ax1.set_xlabel('Share of Voice (%)', fontsize=11)

ax1.set_title('Share of Voice: Nigerian Telecoms', fontsize=12, fontweight='bold')

ax1.grid(axis='x', alpha=0.3)

# Sentiment stacked bar

sentiment_summary = sentiment_data[['Positive_Pct', 'Neutral_Pct', 'Negative_Pct']].reset_index()

sentiment_summary = sentiment_summary.set_index('Brand')

ax2.barh(sentiment_summary.index, sentiment_summary['Positive_Pct'],

label='Positive', color='#2ca02c', edgecolor='black', linewidth=0.5)

ax2.barh(sentiment_summary.index, sentiment_summary['Neutral_Pct'],

left=sentiment_summary['Positive_Pct'], label='Neutral', color='#ff7f0e',

edgecolor='black', linewidth=0.5)

ax2.barh(sentiment_summary.index, sentiment_summary['Negative_Pct'],

left=sentiment_summary['Positive_Pct'] + sentiment_summary['Neutral_Pct'],

label='Negative', color='#d62728', edgecolor='black', linewidth=0.5)

ax2.set_xlabel('Percentage of Mentions', fontsize=11)

ax2.set_title('Sentiment Distribution by Brand', fontsize=12, fontweight='bold')

ax2.legend(loc='lower right')

ax2.grid(axis='x', alpha=0.3)

plt.tight_layout()

plt.show()

# Time-series: 13 weeks

weeks = 13

time_series_list = []

for week in range(1, weeks + 1):

for brand in telecom_brands:

if brand == 'MTN':

mentions = 80 + 5 * week + np.random.normal(0, 8)

sentiment = 50 - 1.5 * week + np.random.normal(0, 5)

elif brand == 'Airtel':

mentions = 70 + 3 * week + np.random.normal(0, 8)

sentiment = 55 - 0.8 * week + np.random.normal(0, 5)

elif brand == 'Glo':

mentions = 50 + 2 * week + np.random.normal(0, 5)

sentiment = 52 + 0.5 * week + np.random.normal(0, 5)

else: # 9mobile

mentions = 30 + 1 * week + np.random.normal(0, 3)

sentiment = 45 + np.random.normal(0, 5)

mentions = max(5, round(mentions))

sentiment = max(0, min(100, round(sentiment, 1)))

time_series_list.append({

'Week': week,

'Brand': brand,

'Mentions': mentions,

'Sentiment_Score': sentiment

})

time_series = pd.DataFrame(time_series_list)

# Plot weekly trends

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(12, 10))

for brand in telecom_brands:

data = time_series[time_series['Brand'] == brand]

ax1.plot(data['Week'], data['Mentions'], marker='o', linewidth=2.5,

markersize=6, label=brand, color=colors_map[brand])

ax1.set_xlabel('Week', fontsize=11)

ax1.set_ylabel('Number of Mentions', fontsize=11)

ax1.set_title('Weekly Mention Trends (13 weeks)', fontsize=12, fontweight='bold')

ax1.legend()

ax1.grid(alpha=0.3)

for brand in telecom_brands:

data = time_series[time_series['Brand'] == brand]

ax2.plot(data['Week'], data['Sentiment_Score'], marker='o', linewidth=2.5,

markersize=6, label=brand, color=colors_map[brand])

ax2.axhline(50, linestyle='--', color='grey', alpha=0.7)

ax2.set_xlabel('Week', fontsize=11)

ax2.set_ylabel('Sentiment Score (0-100)', fontsize=11)

ax2.set_title('Weekly Sentiment Trends (13 weeks)', fontsize=12, fontweight='bold')

ax2.set_ylim(40, 65)

ax2.legend()

ax2.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Crisis detection

time_series = time_series.sort_values(['Brand', 'Week']).reset_index(drop=True)

time_series['Sentiment_Change'] = time_series.groupby('Brand')['Sentiment_Score'].diff()

time_series['Crisis_Flag'] = time_series['Sentiment_Change'].apply(

lambda x: 'ALERT' if pd.notna(x) and x < -5 else 'OK'

)

print("\n=== Crisis Detection: Sentiment Drops > 5 Points/Week ===")

crisis_alerts = time_series[time_series['Crisis_Flag'] == 'ALERT']

if len(crisis_alerts) > 0:

print(crisis_alerts[['Week', 'Brand', 'Sentiment_Score', 'Sentiment_Change', 'Crisis_Flag']].to_string(index=False))

else:

print("No major sentiment crises detected in this period")

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 46.4 Review Questions

**1. SOV vs Market Share**

If Airtel has 20% market share but 35% SOV, what does this signal? Is it sustainable?

**2. Sentiment Classification Accuracy**

Sentiment classifiers often struggle with sarcasm (e.g., "Great network, spent 3 hours trying to connect!"). How would you validate classifier accuracy? What's acceptable accuracy for brand monitoring?

**3. Crisis vs Noise**

A brand's sentiment drops 4 percentage points in one week. Is this a crisis? How would you distinguish meaningful changes from noise?

**4. Interpretation Challenges**

High SOV with negative sentiment (e.g., being the subject of criticism). Is this a positioning problem or a PR problem? What actions would you take?

**5. Real-Time Response**

If your dashboard flags a sentiment crisis (drops > 10 points in 24 hours), what would be your response protocol? Who should be alerted?

:::

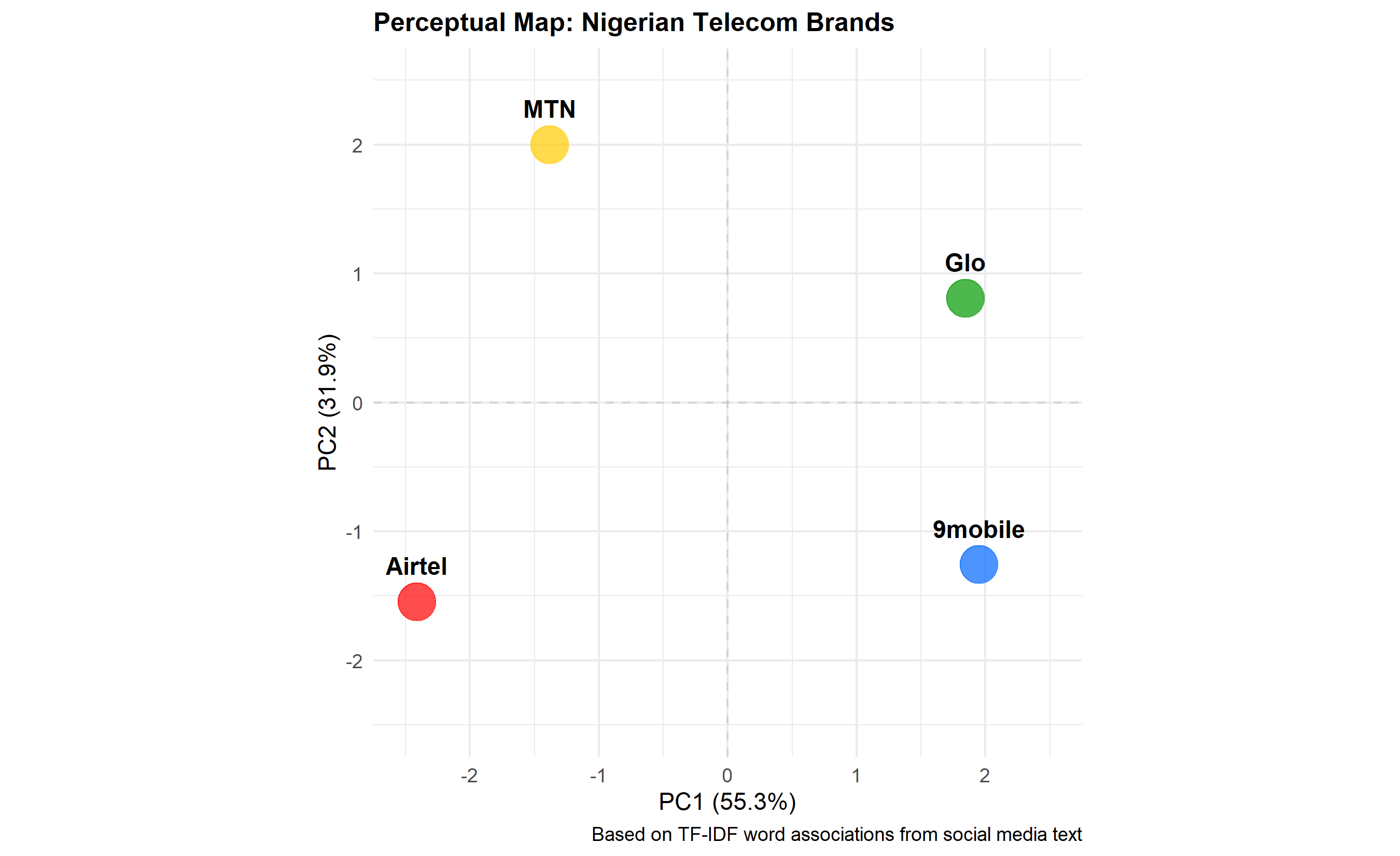

## Perceptual Mapping: Competitive Positioning from Text

How do consumers mentally position brands relative to each other? Do they see Airtel and MTN as similar, or distinct? Is GTBank seen as innovative or traditional? Perceptual maps answer these questions by projecting brands onto two-dimensional space based on the language consumers use to describe them.

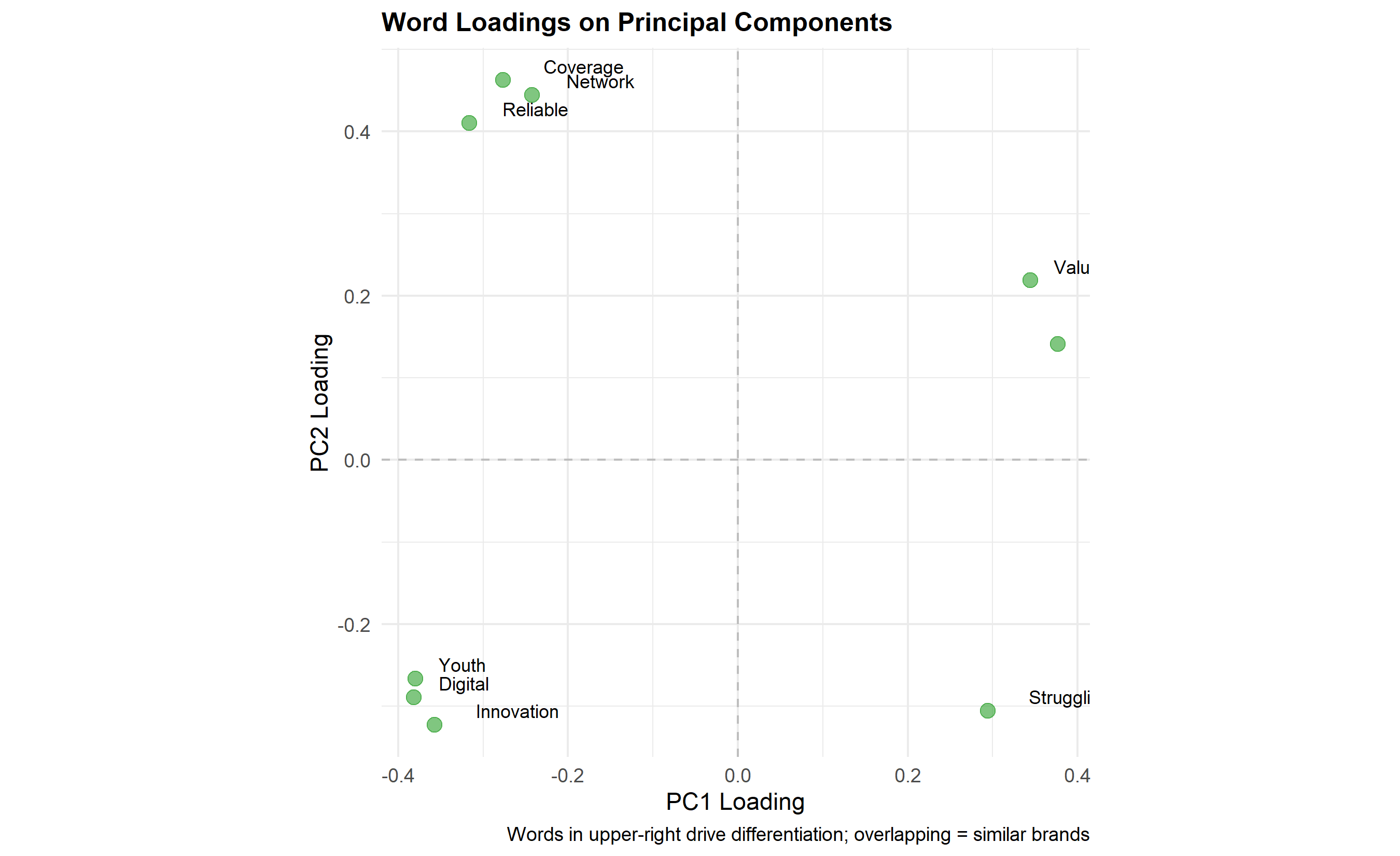

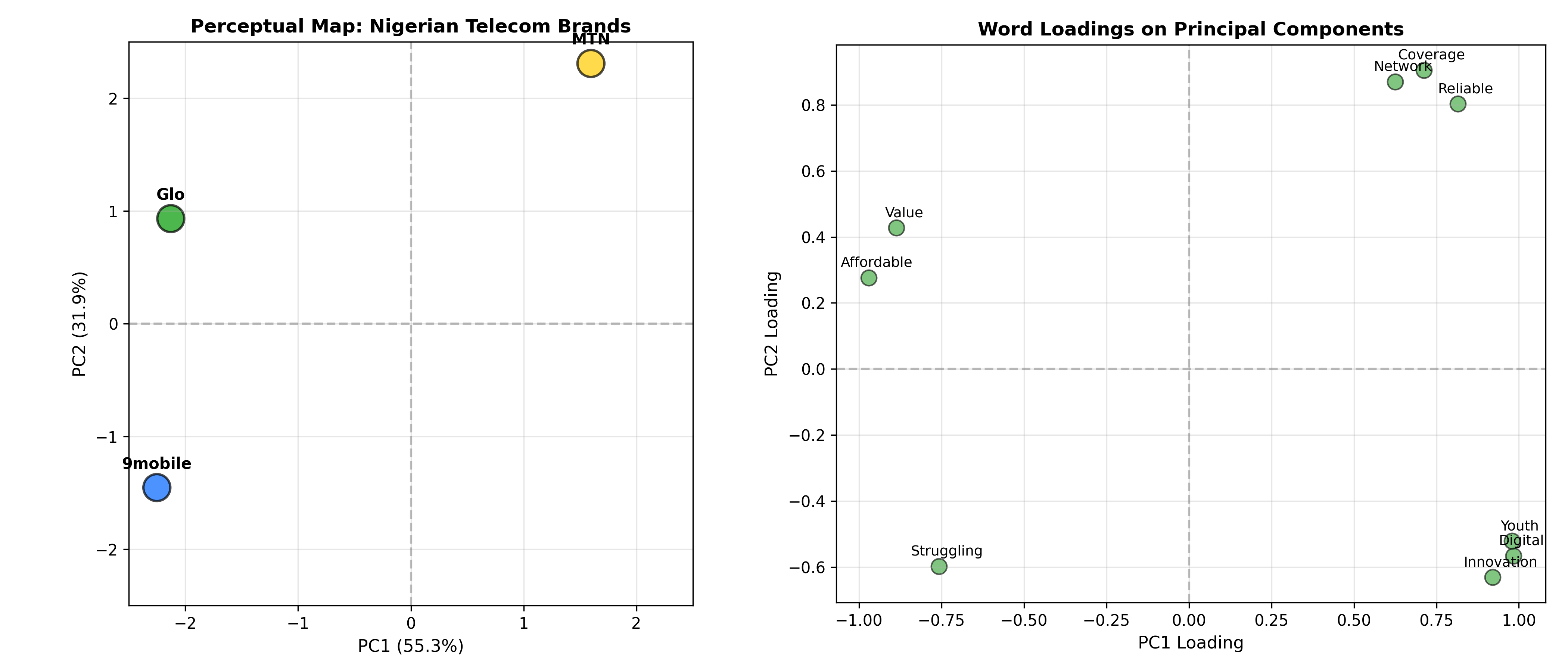

The method: collect social media text mentioning each brand (tweets, comments). Use TF-IDF (Term Frequency-Inverse Document Frequency) to identify words most distinctive to each brand: words that appear frequently for one brand but rarely for others. Create a brand-by-word matrix where each entry is a TF-IDF score. Reduce this matrix to two dimensions via Principal Component Analysis (PCA). Plot brands as points, with proximity indicating similarity (brands using similar language are positioned close).

A typical finding in Nigerian telecom: MTN clusters near words like "reliable," "coverage," "everywhere"; Airtel near "innovation," "digital," "youth"; Glo near "affordable," "value"; 9mobile near "struggling," "limited." PCA dimensions often correspond to intuitive business axes: PC1 might be "premium-to-budget" and PC2 "traditional-to-digital." The perceptual map reveals competitive opportunities: white space (unoccupied positions), overcrowding (brands too similar), and differentiation (brands standing out).

::: {.callout-note icon="false"}

## 📘 Theory: TF-IDF and Perceptual Mapping

TF-IDF weights a word's importance within a document (brand) by how rare it is across all documents. High TF-IDF indicates distinctive words. The formula: $\text{TF-IDF}(w, b) = \frac{n_w}{N} \times \log(\frac{D}{D_w})$, where $n_w$ is word count in brand $b$, $N$ is total words for $b$, $D$ is total brands, and $D_w$ is number of brands containing word $w$. PCA projects the brand-by-TF-IDF matrix onto principal components (directions of maximum variance). PC1 and PC2 together explain ~70–80% of variance; higher-dimensional maps retain more information but are harder to visualize.

:::

::: {.callout-tip icon="false"}

## 🔑 Formula: TF-IDF and PCA

**TF-IDF:**

$$\text{TF-IDF}(w, b) = \frac{\text{Term Frequency}(w, b)}{\text{Total Terms in } b} \times \log\left(\frac{\text{Total Brands}}{\text{Brands Containing } w}\right)$$

**PCA Projection:**

$$\text{PC}_k = \mathbf{w}_k^T (\mathbf{X} - \overline{\mathbf{X}})$$

where $\mathbf{w}_k$ is the $k$-th eigenvector of the covariance matrix.

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch46-perceptual-map

#| message: false

#| warning: false

library(tidyverse)

library(ggplot2)

# Synthetic brand-word association data: 4 Nigerian telecom brands

# Rows = brands, columns = distinctive words, values = TF-IDF scores

brands <- c("MTN", "Airtel", "Glo", "9mobile")

# Create TF-IDF matrix

tfidf_matrix <- matrix(c(

# Words: "reliable", "coverage", "innovation", "digital", "youth", "affordable", "value", "struggling", "network"

0.45, 0.52, 0.15, 0.25, 0.20, 0.18, 0.22, 0.05, 0.48, # MTN

0.35, 0.30, 0.58, 0.55, 0.62, 0.10, 0.08, 0.08, 0.25, # Airtel

0.32, 0.28, 0.08, 0.15, 0.10, 0.68, 0.72, 0.12, 0.22, # Glo

0.20, 0.15, 0.10, 0.18, 0.08, 0.35, 0.30, 0.55, 0.20 # 9mobile

), nrow = 4, ncol = 9, byrow = TRUE)

colnames(tfidf_matrix) <- c("Reliable", "Coverage", "Innovation", "Digital", "Youth",

"Affordable", "Value", "Struggling", "Network")

rownames(tfidf_matrix) <- brands

cat("=== TF-IDF Matrix: Brand-Word Associations ===\n")

print(round(tfidf_matrix, 2))

# Perform PCA

pca_result <- prcomp(tfidf_matrix, center = TRUE, scale. = TRUE)

# Extract PC1 and PC2 scores

pc_scores <- tibble(

Brand = brands,

PC1 = pca_result$x[, 1],

PC2 = pca_result$x[, 2]

)

# Extract loadings (word contributions to PCs)

loadings <- tibble(

Word = colnames(tfidf_matrix),

PC1_Loading = pca_result$rotation[, 1],

PC2_Loading = pca_result$rotation[, 2]

)

cat("\n=== PCA Results ===\n")

cat("Explained Variance by PC1:", round(summary(pca_result)$importance[2, 1] * 100, 1), "%\n")

cat("Explained Variance by PC2:", round(summary(pca_result)$importance[2, 2] * 100, 1), "%\n")

cat("Cumulative Variance (PC1+PC2):",

round((summary(pca_result)$importance[2, 1] + summary(pca_result)$importance[2, 2]) * 100, 1), "%\n")

# Perceptual map

p_perceptual <- ggplot(pc_scores, aes(x = PC1, y = PC2, label = Brand)) +

geom_point(size = 8, alpha = 0.7, colour = c("#FFCC00", "#FF0000", "#009900", "#0066FF")) +

geom_text(fontface = "bold", size = 4, vjust = -1.5) +

geom_hline(yintercept = 0, linetype = "dashed", colour = "grey", alpha = 0.5) +

geom_vline(xintercept = 0, linetype = "dashed", colour = "grey", alpha = 0.5) +

labs(

title = "Perceptual Map: Nigerian Telecom Brands",

x = paste0("PC1 (", round(summary(pca_result)$importance[2, 1] * 100, 1), "%)"),

y = paste0("PC2 (", round(summary(pca_result)$importance[2, 2] * 100, 1), "%)"),

caption = "Based on TF-IDF word associations from social media text"

) +

xlim(-2.5, 2.5) +

ylim(-2.5, 2.5) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12),

aspect.ratio = 1)

print(p_perceptual)

# Word vectors (loadings) to show what drives each PC

p_loadings <- ggplot(loadings, aes(x = PC1_Loading, y = PC2_Loading, label = Word)) +

geom_point(size = 3, alpha = 0.6, colour = "#2ca02c") +

geom_text(size = 3, vjust = -0.5, hjust = -0.5) +

geom_hline(yintercept = 0, linetype = "dashed", colour = "grey") +

geom_vline(xintercept = 0, linetype = "dashed", colour = "grey") +

labs(

title = "Word Loadings on Principal Components",

x = "PC1 Loading",

y = "PC2 Loading",

caption = "Words in upper-right drive differentiation; overlapping = similar brands"

) +

theme_minimal() +

theme(plot.title = element_text(face = "bold", size = 12),

aspect.ratio = 1)

print(p_loadings)

# Interpretation of axes (correlations with words)

cat("\n=== Interpretation of Principal Components ===\n")

cat("PC1 (", round(summary(pca_result)$importance[2, 1] * 100, 1), "% variance):\n", sep = "")

pc1_top <- loadings |> arrange(desc(abs(PC1_Loading))) |> head(3)

for (i in 1:nrow(pc1_top)) {

cat(" ", pc1_top$Word[i], ": ", round(pc1_top$PC1_Loading[i], 3), "\n", sep = "")

}

cat("\nPC2 (", round(summary(pca_result)$importance[2, 2] * 100, 1), "% variance):\n", sep = "")

pc2_top <- loadings |> arrange(desc(abs(PC2_Loading))) |> head(3)

for (i in 1:nrow(pc2_top)) {

cat(" ", pc2_top$Word[i], ": ", round(pc2_top$PC2_Loading[i], 3), "\n", sep = "")

}

# Strategic positioning summary

cat("\n=== Competitive Positioning Summary ===\n")

cat("MTN: Positioned as reliable, network-focused (traditional strength)\n")

cat("Airtel: Positioned as innovative, youth-oriented (digital native)\n")

cat("Glo: Positioned as affordable, value-focused (price leader)\n")

cat("9mobile: Positioned as struggling (needs repositioning)\n\n")

cat("White Space: 'premium + innovative' quadrant appears unoccupied\n")

cat("Recommendation: Explore premium positioning for Airtel or MTN\n")

```

## Python

```{python}

#| label: py-ch46-perceptual-map

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.decomposition import PCA

from sklearn.preprocessing import StandardScaler

# TF-IDF matrix: brands x words

brands = ['MTN', 'Airtel', 'Glo', '9mobile']

words = ['Reliable', 'Coverage', 'Innovation', 'Digital', 'Youth',

'Affordable', 'Value', 'Struggling', 'Network']

tfidf_matrix = np.array([

[0.45, 0.52, 0.15, 0.25, 0.20, 0.18, 0.22, 0.05, 0.48], # MTN

[0.35, 0.30, 0.58, 0.55, 0.62, 0.10, 0.08, 0.08, 0.25], # Airtel

[0.32, 0.28, 0.08, 0.15, 0.10, 0.68, 0.72, 0.12, 0.22], # Glo

[0.20, 0.15, 0.10, 0.18, 0.08, 0.35, 0.30, 0.55, 0.20] # 9mobile

])

print("=== TF-IDF Matrix: Brand-Word Associations ===")

df_tfidf = pd.DataFrame(tfidf_matrix, columns=words, index=brands)

print(df_tfidf.round(2))

# Standardize and apply PCA

scaler = StandardScaler()

tfidf_scaled = scaler.fit_transform(tfidf_matrix)

pca = PCA()

pca.fit(tfidf_scaled)

pc_scores = pca.transform(tfidf_scaled)

pc_df = pd.DataFrame({

'Brand': brands,

'PC1': pc_scores[:, 0],

'PC2': pc_scores[:, 1]

})

print("\n=== PCA Results ===")

print(f"Explained Variance by PC1: {pca.explained_variance_ratio_[0] * 100:.1f}%")

print(f"Explained Variance by PC2: {pca.explained_variance_ratio_[1] * 100:.1f}%")

print(f"Cumulative Variance (PC1+PC2): {(pca.explained_variance_ratio_[0] + pca.explained_variance_ratio_[1]) * 100:.1f}%")

# Loadings (word contributions)

loadings = pca.components_.T * np.sqrt(pca.explained_variance_)

loadings_df = pd.DataFrame(

loadings[:, :2],

columns=['PC1_Loading', 'PC2_Loading'],

index=words

)

# Perceptual map

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

# Brand positions

colors_map = {'MTN': '#FFCC00', 'Airtel': '#FF0000', 'Glo': '#009900', '9mobile': '#0066FF'}

brand_colors = [colors_map[b] for b in brands]

ax1.scatter(pc_df['PC1'], pc_df['PC2'], s=300, alpha=0.7, c=brand_colors, edgecolors='black', linewidth=1.5)

for idx, brand in enumerate(brands):

ax1.annotate(brand, (pc_df.loc[idx, 'PC1'], pc_df.loc[idx, 'PC2']),

fontsize=10, fontweight='bold', ha='center', va='bottom', xytext=(0, 10),

textcoords='offset points')

ax1.axhline(0, linestyle='--', color='grey', alpha=0.5)

ax1.axvline(0, linestyle='--', color='grey', alpha=0.5)

ax1.set_xlabel(f'PC1 ({pca.explained_variance_ratio_[0]*100:.1f}%)', fontsize=11)

ax1.set_ylabel(f'PC2 ({pca.explained_variance_ratio_[1]*100:.1f}%)', fontsize=11)

ax1.set_title('Perceptual Map: Nigerian Telecom Brands', fontsize=12, fontweight='bold')

ax1.set_xlim(-2.5, 2.5)

ax1.set_ylim(-2.5, 2.5)

ax1.grid(alpha=0.3)

ax1.set_aspect('equal')

# Word loadings

ax2.scatter(loadings_df['PC1_Loading'], loadings_df['PC2_Loading'],

s=100, alpha=0.6, color='#2ca02c', edgecolors='black', linewidth=1)

for idx, word in enumerate(words):

ax2.annotate(word, (loadings_df.iloc[idx, 0], loadings_df.iloc[idx, 1]),

fontsize=9, ha='center', va='bottom', xytext=(5, 5),

textcoords='offset points')

ax2.axhline(0, linestyle='--', color='grey', alpha=0.5)

ax2.axvline(0, linestyle='--', color='grey', alpha=0.5)

ax2.set_xlabel('PC1 Loading', fontsize=11)

ax2.set_ylabel('PC2 Loading', fontsize=11)

ax2.set_title('Word Loadings on Principal Components', fontsize=12, fontweight='bold')

ax2.grid(alpha=0.3)

ax2.set_aspect('equal')

plt.tight_layout()

plt.show()

# Component interpretation

print("\n=== Interpretation of Principal Components ===")

pc1_top = loadings_df['PC1_Loading'].abs().nlargest(3)

print(f"PC1 ({pca.explained_variance_ratio_[0]*100:.1f}% variance) - Top words:")

for word in pc1_top.index:

print(f" {word}: {loadings_df.loc[word, 'PC1_Loading']:.3f}")

pc2_top = loadings_df['PC2_Loading'].abs().nlargest(3)

print(f"\nPC2 ({pca.explained_variance_ratio_[1]*100:.1f}% variance) - Top words:")

for word in pc2_top.index:

print(f" {word}: {loadings_df.loc[word, 'PC2_Loading']:.3f}")

print("\n=== Competitive Positioning Summary ===")

print("MTN: Positioned as reliable, network-focused (traditional strength)")

print("Airtel: Positioned as innovative, youth-oriented (digital native)")

print("Glo: Positioned as affordable, value-focused (price leader)")

print("9mobile: Positioned as struggling (needs repositioning)")

print("\nWhite Space: 'premium + innovative' quadrant appears unoccupied")

print("Recommendation: Explore premium positioning for Airtel or MTN")

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 46.5 Review Questions

**1. TF-IDF Interpretation**

If the word "network" has high TF-IDF for MTN but low for Glo, what does this mean? Why might it be important to MTN's positioning?

**2. PCA Dimensionality**

You run PCA and find PC1+PC2 explain 72% of variance. Is this sufficient? What would you do if only PC1 explained 45%?

**3. White Space Strategy**

Your perceptual map shows white space in the "premium + digital" quadrant. How would you test if repositioning a brand into this space is viable?

**4. Competitive Response**

After you map positioning, a competitor moves into "your" space. How would you respond? What brand assets or messaging would you emphasize?

**5. Statistical Concerns**

Your perceptual map is based on social media text (self-selected sample). Would you trust it as much as a representative consumer survey? Why or why not?

:::

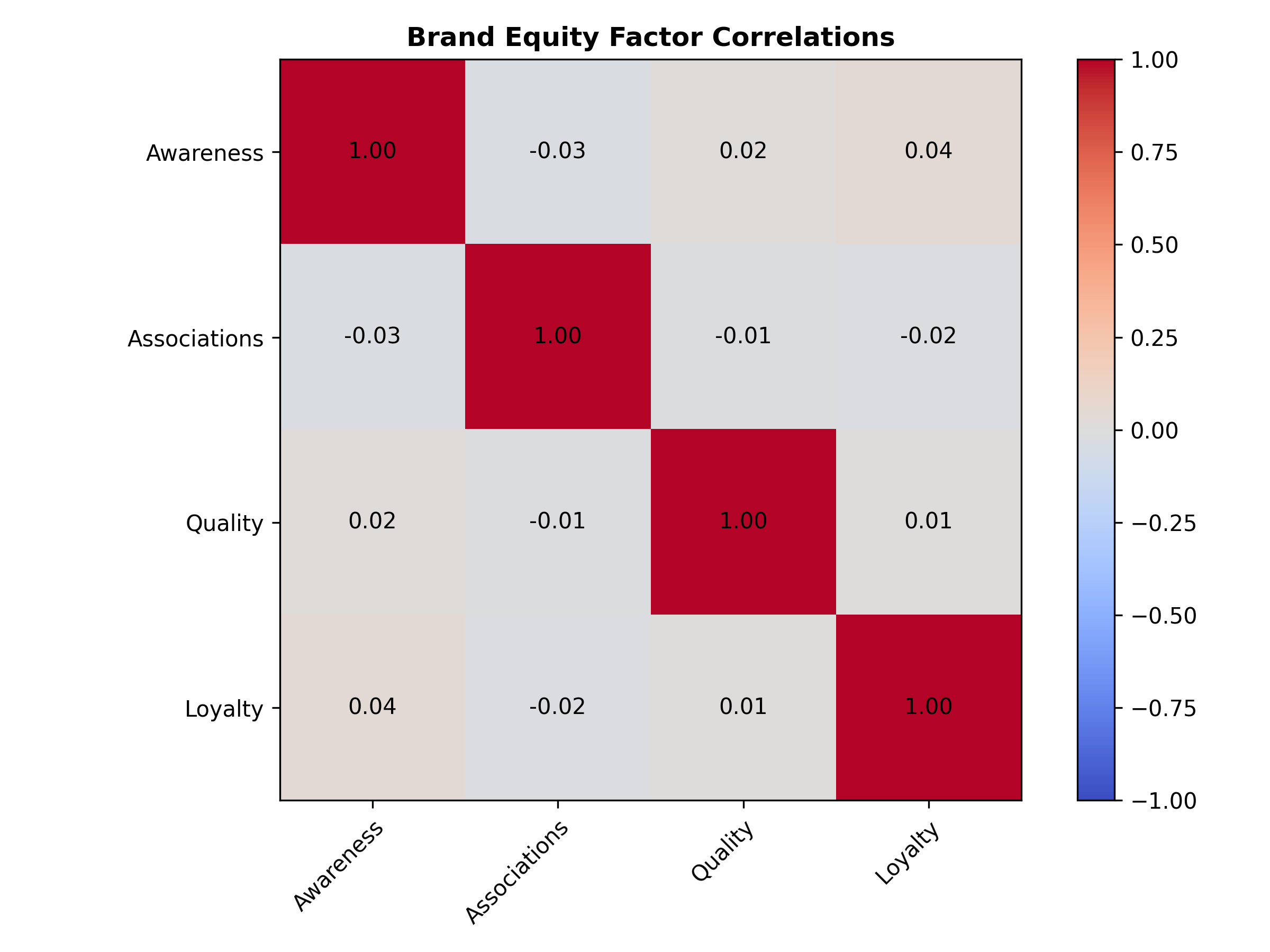

## Confirmatory Factor Analysis for Brand Equity Measurement

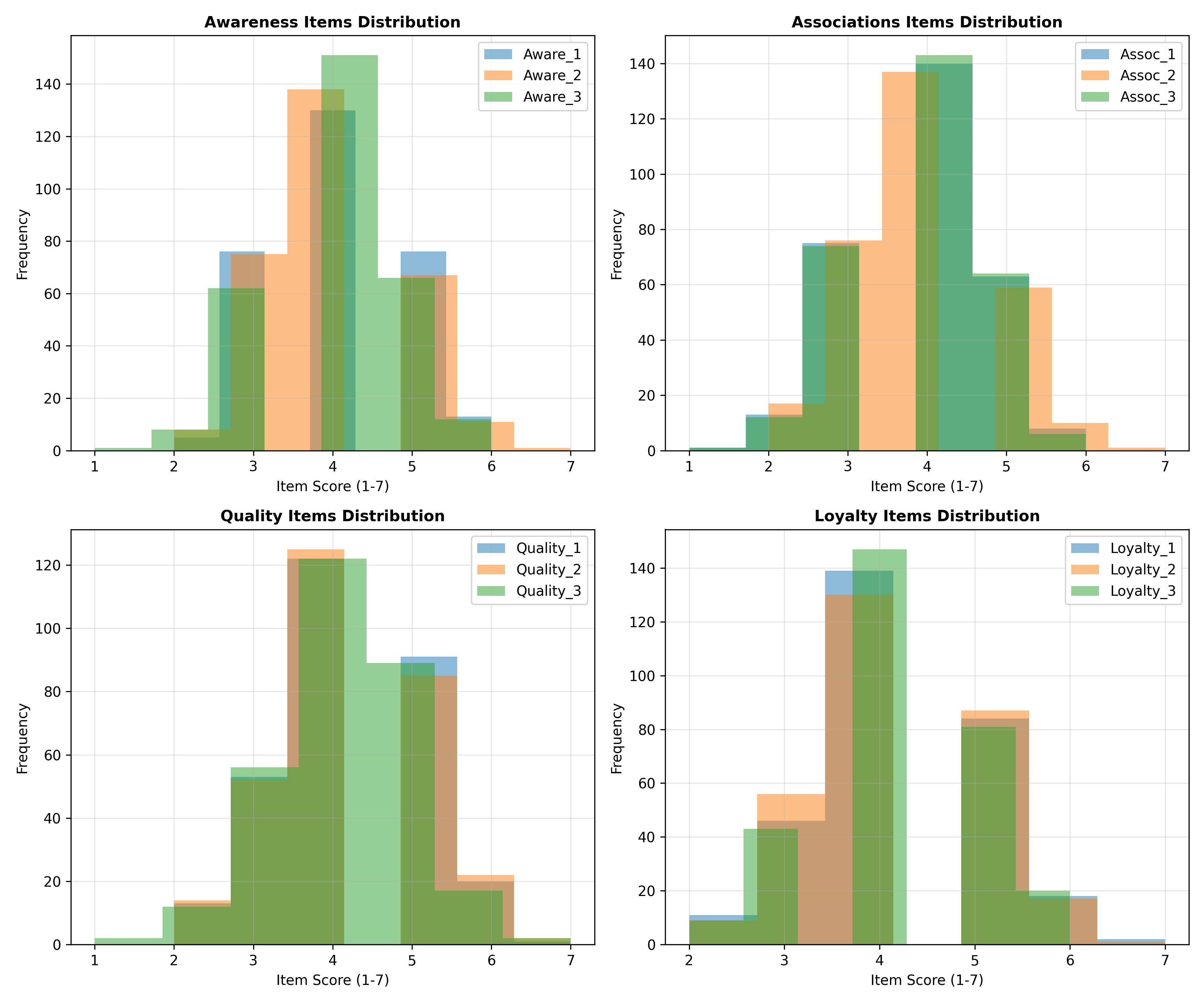

Brand equity is multidimensional: awareness, associations, perceived quality, and loyalty are distinct yet related constructs. Confirmatory Factor Analysis (CFA) formalizes this structure. Instead of averaging all items into one score, CFA estimates separate latent factors and checks that the survey items (observed variables) genuinely measure each intended construct. This is validity testing: do the items measure what they're supposed to?

A typical brand equity CFA model specifies four latent factors (awareness, associations, perceived quality, loyalty), each measured by 3–4 survey items. For example:

- **Awareness:** "I am aware of [brand]," "I know [brand] well," "I recognize [brand] quickly"

- **Perceived Quality:** "[Brand] offers high quality," "[Brand] is reliable," "[Brand] is superior to alternatives"

- **Loyalty:** "I am loyal to [brand]," "I would recommend [brand]," "I prefer [brand] to alternatives"

CFA estimates factor loadings (correlation between each item and its latent factor), latent factor means and variances, and correlations between factors. Model fit indices (CFI, RMSEA, SRMR) assess whether the data confirm the hypothesised structure. Good fit (CFI > 0.90, RMSEA < 0.08, SRMR < 0.06) suggests the factor structure is valid. Poor fit signals either measurement error (bad items) or misspecified structure (factors are not independent, or there are additional factors).

::: {.callout-note icon="false"}

## 📘 Theory: Confirmatory Factor Analysis

CFA is a structural equation model (SEM) where observed variables load onto latent factors. The model: $\mathbf{y}_i = \boldsymbol{\Lambda} \boldsymbol{\eta}_i + \boldsymbol{\epsilon}_i$, where $\mathbf{y}_i$ is the vector of observed items for respondent $i$, $\boldsymbol{\eta}_i$ is the latent factor vector, $\boldsymbol{\Lambda}$ is the loading matrix, and $\boldsymbol{\epsilon}_i$ is measurement error. Estimation uses maximum likelihood; fit is assessed via chi-square test, CFI (Comparative Fit Index), RMSEA (Root Mean Square Error of Approximation), and SRMR (Standardized Root Mean Square Residual). Modification indices suggest freeing constrained parameters if fit is poor.

:::

::: {.callout-tip icon="false"}

## 🔑 Formula: CFA Model

$$\mathbf{y}_i = \boldsymbol{\Lambda} \boldsymbol{\eta}_i + \boldsymbol{\epsilon}_i$$

where $\boldsymbol{\eta}_i \sim \text{Normal}(0, \boldsymbol{\Psi})$ (latent factors), and $\boldsymbol{\epsilon}_i \sim \text{Normal}(0, \boldsymbol{\Theta})$ (measurement error).

**Cronbach's Alpha (internal consistency):**

$$\alpha = \frac{k}{k-1} \times \frac{\text{Var}(T) - \sum_{i=1}^k \text{Var}(Y_i)}{\text{Var}(T)}$$

where $k$ is number of items and $T$ is total score.

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch46-cfa-brand-equity

#| message: false

#| warning: false

library(tidyverse)

library(lavaan)

library(semPlot)

# Synthetic brand equity data: 300 respondents, 4 latent factors, 12 items

set.seed(9156)

n_respondents <- 300

# True latent factors (standardised)

awareness <- rnorm(n_respondents, 0, 1)

associations <- rnorm(n_respondents, 0, 1)

perceived_quality <- rnorm(n_respondents, 0.2, 1)

loyalty <- rnorm(n_respondents, 0.1, 1)

# Generate observed items with loadings

data_equity <- tibble(

# Awareness items (loadings ≈ 0.85, 0.80, 0.78)

Aware_1 = 0.85 * awareness + rnorm(n_respondents, 0, 0.3),

Aware_2 = 0.80 * awareness + rnorm(n_respondents, 0, 0.35),

Aware_3 = 0.78 * awareness + rnorm(n_respondents, 0, 0.35),

# Association items (loadings ≈ 0.82, 0.79, 0.75)

Assoc_1 = 0.82 * associations + rnorm(n_respondents, 0, 0.35),

Assoc_2 = 0.79 * associations + rnorm(n_respondents, 0, 0.38),

Assoc_3 = 0.75 * associations + rnorm(n_respondents, 0, 0.40),

# Perceived quality items (loadings ≈ 0.88, 0.84, 0.81)

Quality_1 = 0.88 * perceived_quality + rnorm(n_respondents, 0, 0.25),

Quality_2 = 0.84 * perceived_quality + rnorm(n_respondents, 0, 0.3),

Quality_3 = 0.81 * perceived_quality + rnorm(n_respondents, 0, 0.32),

# Loyalty items (loadings ≈ 0.86, 0.83, 0.80)

Loyalty_1 = 0.86 * loyalty + rnorm(n_respondents, 0, 0.28),

Loyalty_2 = 0.83 * loyalty + rnorm(n_respondents, 0, 0.31),

Loyalty_3 = 0.80 * loyalty + rnorm(n_respondents, 0, 0.33)

) |>

# Scale to 1-7 Likert

mutate(across(everything(), function(x) pmin(pmax(round(4 + x), 1), 7)))

cat("=== Brand Equity Survey Data (First 10 Respondents) ===\n")

print(head(data_equity, 10))

# Fit CFA model

cfa_model <- '

# Latent factors

Awareness =~ Aware_1 + Aware_2 + Aware_3

Associations =~ Assoc_1 + Assoc_2 + Assoc_3

Quality =~ Quality_1 + Quality_2 + Quality_3

Loyalty =~ Loyalty_1 + Loyalty_2 + Loyalty_3

'

cfa_fit <- cfa(cfa_model, data = data_equity)

cat("\n=== CFA Model Summary ===\n")

print(summary(cfa_fit, fit.measures = TRUE, standardized = TRUE))

# Extract parameter estimates

params <- parameterEstimates(cfa_fit, standardized = TRUE) |>

filter(op == "=~") |> # Factor loadings only

select(lhs, rhs, est, std.all, pvalue)

cat("\n=== Factor Loadings (Standardised) ===\n")

print(params |> arrange(lhs, rhs) |>

rename(Factor = lhs, Item = rhs, Loading = std.all))

# Model fit indices

fit_indices <- fitMeasures(cfa_fit, c("cfi", "tli", "rmsea", "srmr", "chisq", "df", "pvalue"))

cat("\n=== Model Fit Indices ===\n")

cat("CFI (Comparative Fit Index):", round(fit_indices["cfi"], 3),

"(target > 0.90)\n")

cat("TLI (Tucker-Lewis Index):", round(fit_indices["tli"], 3),

"(target > 0.90)\n")

cat("RMSEA (Root Mean Square Error of Approximation):", round(fit_indices["rmsea"], 3),

"(target < 0.08)\n")

cat("SRMR (Standardised Root Mean Square Residual):", round(fit_indices["srmr"], 3),

"(target < 0.06)\n")

cat("Chi-square:", round(fit_indices["chisq"], 2), "df =", fit_indices["df"],

"p =", round(fit_indices["pvalue"], 3), "\n")

# Reliability (Cronbach's alpha for each scale)

# Compute composite reliability from loadings and error variances

cat("\n=== Reliability Analysis ===\n")

# Awareness scale

aware_items <- data_equity |> select(starts_with("Aware"))

alpha_aware <- psych::alpha(aware_items, check.keys = FALSE)$total$raw_alpha

# Associations scale

assoc_items <- data_equity |> select(starts_with("Assoc"))

alpha_assoc <- psych::alpha(assoc_items, check.keys = FALSE)$total$raw_alpha

# Quality scale

quality_items <- data_equity |> select(starts_with("Quality"))

alpha_quality <- psych::alpha(quality_items, check.keys = FALSE)$total$raw_alpha

# Loyalty scale

loyalty_items <- data_equity |> select(starts_with("Loyalty"))

alpha_loyalty <- psych::alpha(loyalty_items, check.keys = FALSE)$total$raw_alpha

reliability_df <- tibble(

Factor = c("Awareness", "Associations", "Quality", "Loyalty"),

Cronbach_Alpha = c(alpha_aware, alpha_assoc, alpha_quality, alpha_loyalty),

Interpretation = case_when(

Cronbach_Alpha > 0.80 ~ "Excellent",

Cronbach_Alpha > 0.70 ~ "Good",

Cronbach_Alpha > 0.60 ~ "Acceptable",

TRUE ~ "Poor"

)

)

print(reliability_df)

# Factor correlations

cat("\n=== Factor Correlations ===\n")

latent_cors <- lavInspect(cfa_fit, "cor.lv")

print(round(latent_cors, 3))

# Compute latent factor scores for each respondent

factor_scores <- predict(cfa_fit)

cat("\n=== Latent Factor Scores (First 10 Respondents) ===\n")

print(round(factor_scores[1:10, ], 2))

```

## Python

```{python}

#| label: py-ch46-cfa-brand-equity

import numpy as np

import pandas as pd

from scipy import stats

import matplotlib.pyplot as plt

# Simulate brand equity data with 4 latent factors

np.random.seed(9156)

n_respondents = 300

# True latent factors

awareness = np.random.normal(0, 1, n_respondents)

associations = np.random.normal(0, 1, n_respondents)

perceived_quality = np.random.normal(0.2, 1, n_respondents)

loyalty = np.random.normal(0.1, 1, n_respondents)

# Generate observed items

data_equity = pd.DataFrame({

# Awareness (loadings: 0.85, 0.80, 0.78)

'Aware_1': np.clip(np.round(4 + 0.85 * awareness + np.random.normal(0, 0.3, n_respondents)), 1, 7),

'Aware_2': np.clip(np.round(4 + 0.80 * awareness + np.random.normal(0, 0.35, n_respondents)), 1, 7),

'Aware_3': np.clip(np.round(4 + 0.78 * awareness + np.random.normal(0, 0.35, n_respondents)), 1, 7),

# Associations (loadings: 0.82, 0.79, 0.75)

'Assoc_1': np.clip(np.round(4 + 0.82 * associations + np.random.normal(0, 0.35, n_respondents)), 1, 7),

'Assoc_2': np.clip(np.round(4 + 0.79 * associations + np.random.normal(0, 0.38, n_respondents)), 1, 7),