---

title: "Modern Forecasting: Prophet, ML Methods, and Ensembles"

---

```{python}

#| label: python-setup-25-modern-forecasting

#| include: false

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from prophet import Prophet

from datetime import datetime, timedelta

import warnings

import lightgbm as lgb

from sklearn.metrics import mean_squared_error, mean_absolute_error

from statsmodels.tsa.arima.model import ARIMA

from statsmodels.tsa.holtwinters import ExponentialSmoothing

```

::: {.callout-note icon="false"}

## 📋 Learning Objectives

- Understand the limitations of classical ARIMA for modern business forecasting with multiple seasonalities and irregular events

- Build and interpret Prophet models, extending them with Nigerian public holidays and custom regressors

- Transform time series into supervised learning problems using lag features and rolling statistics

- Implement walk-forward validation to avoid data leakage and produce honest forecast accuracy estimates

- Reconcile forecasts across hierarchical levels (national → regional → LGA) using top-down and MinT methods

- Evaluate forecast accuracy using scale-free metrics like MASE and MAPE appropriate for different business contexts

- Combine multiple forecasting approaches into weighted ensembles that reduce variance and improve robustness

:::

## Beyond Classical Forecasting

The classical ARIMA framework, elegant and mathematically grounded, struggles under the demands of modern business analytics. A retailer forecasting monthly sales across Nigeria faces challenges that ARIMA was never designed to address: Christmas demand spikes aligned to a fixed calendar date, not a statistical pattern; the irregular timing of Sallah festivals following the lunar Islamic calendar; sudden structural breaks when the Naira depreciates sharply or fuel supply chains collapse; multiple competing seasonal cycles (weekly, monthly, annual) layered atop one another; and the presence of missing data from store closures or strike action.

ARIMA assumes a single, simple seasonal pattern (usually annual) and expects the data to be stationary or differenced into stationarity. When you have weekly, monthly, and annual seasonality simultaneously—as in NGN/USD currency pairs during oil price shocks—ARIMA requires separate seasonal components stacked in ways that become unwieldy (Seasonal ARIMA with period 52 *and* period 12). Moreover, ARIMA provides point forecasts; for treasury applications where you must plan for downside risk, you need prediction intervals that reflect parameter uncertainty and structural volatility.

Machine learning approaches—gradient boosting, random forests, neural networks—sidestep many of these issues by learning arbitrary nonlinear relationships from features rather than imposing a parametric model. They scale naturally to multiple seasons and external regressors. Yet raw ML methods are black boxes, lack principled uncertainty quantification, and can overfit to spurious historical patterns. Facebook's Prophet, released in 2017, charts a middle path: it decomposes the forecast into interpretable components (trend, seasonality, holidays, regressors) yet fits them flexibly using piecewise linear trends and Fourier series. Prophet is designed for business forecasting at scale and handles missing data, outliers, and irregular events with minimal tuning.

This chapter builds the intuition and practical skills to choose among these approaches. For a Nigerian FMCG distributor with 36 months of monthly sales, Prophet may capture the trend and Christmas surge with five minutes of setup. For a fintech platform with 10,000 daily transaction streams each with different patterns, you might build XGBoost ensembles on lag features. For commodity prices or exchange rates where sudden regime shifts occur, a portfolio of methods—ARIMA, Prophet, and ML—combined with walk-forward validation on recent data gives you resilience.

## Meta's Prophet: Decomposable Forecasting with Seasonality and Holidays

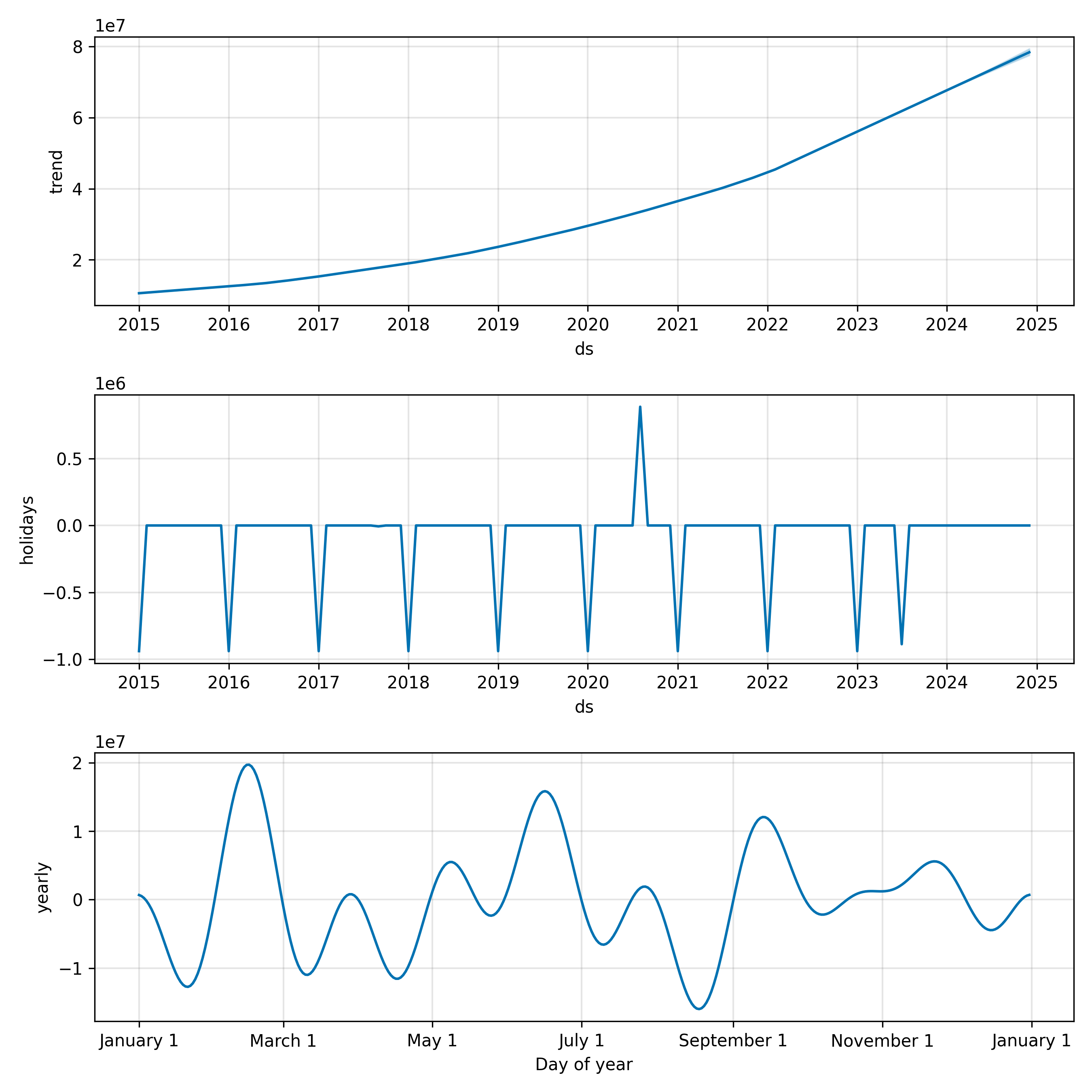

Prophet decomposes the time series into four additive components: trend, seasonality, holiday effects, and an error term.

$$y_t = g(t) + s(t) + h(t) + \epsilon_t$$

The trend $g(t)$ is piecewise linear, allowing changepoints where the growth rate shifts. Seasonality $s(t)$ is modelled using Fourier series: a sum of sine and cosine waves at different frequencies. Holiday effects $h(t)$ are window functions around calendar dates. The error $\epsilon_t$ captures what the model misses.

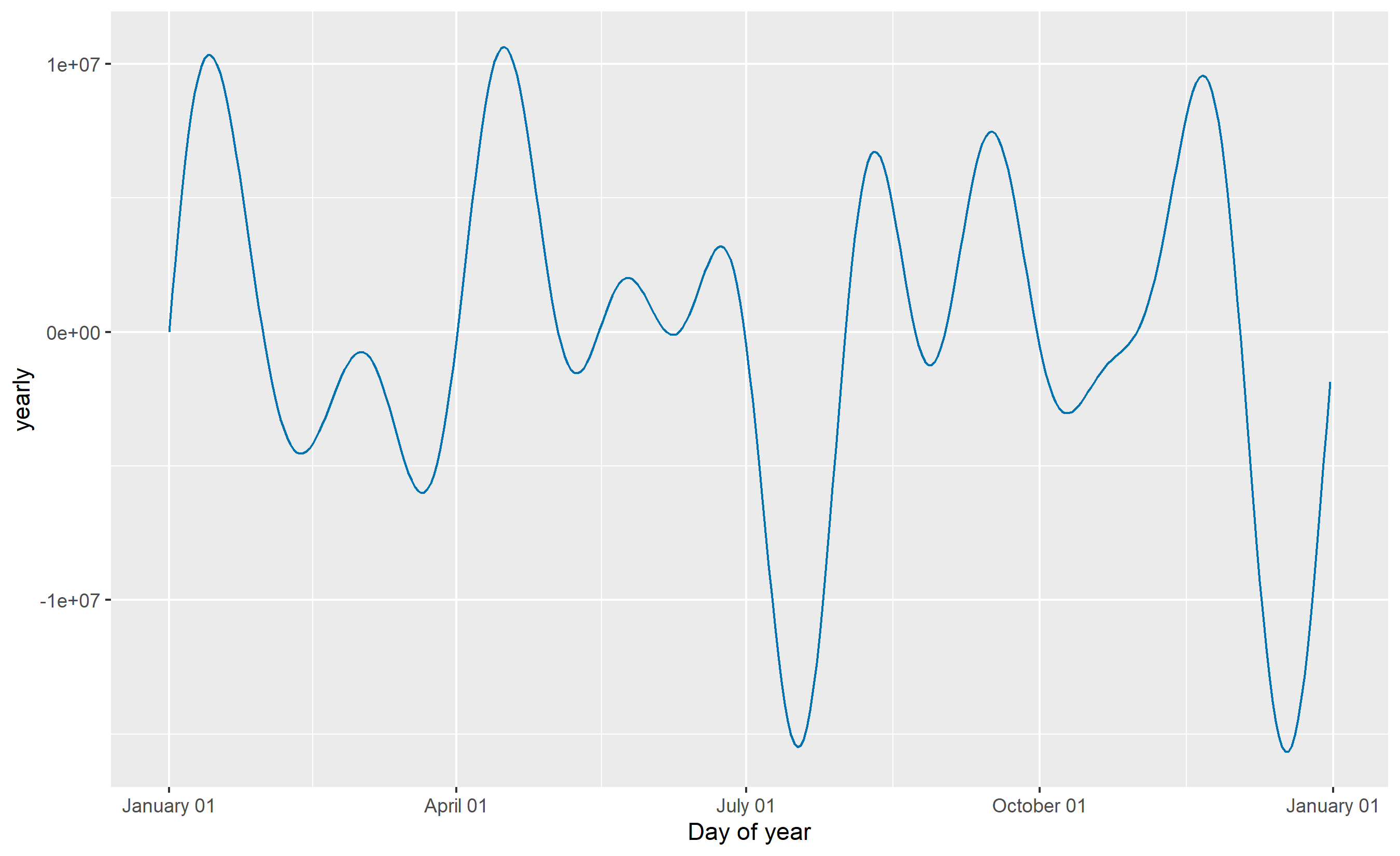

**Fourier Series Intuition**: Imagine sound. A pure tone is a single sine wave at one frequency. A human voice is an infinite sum of sine and cosine waves (the Fourier series) at different frequencies and amplitudes, which together recreate the complex timbre. Seasonality in sales data works the same way. Christmas demand is not a simple repeating pattern; it includes a sharp spike centred on December 25, some lead-in from November, and a tail extending into early January. A Fourier series with dozens of sine/cosine terms can approximate this shape. For annual seasonality, Prophet typically uses 10 Fourier pairs (20 terms), which is enough to capture ripples and asymmetries while remaining interpretable.

Prophet fits these components using Bayesian methods in Stan. Priors on the trend changepoint magnitudes and seasonality smoothness prevent overfitting. The model is implemented in R (from Facebook's official package `prophet`) and Python (`prophet` via PyPI). Let's build a concrete example.

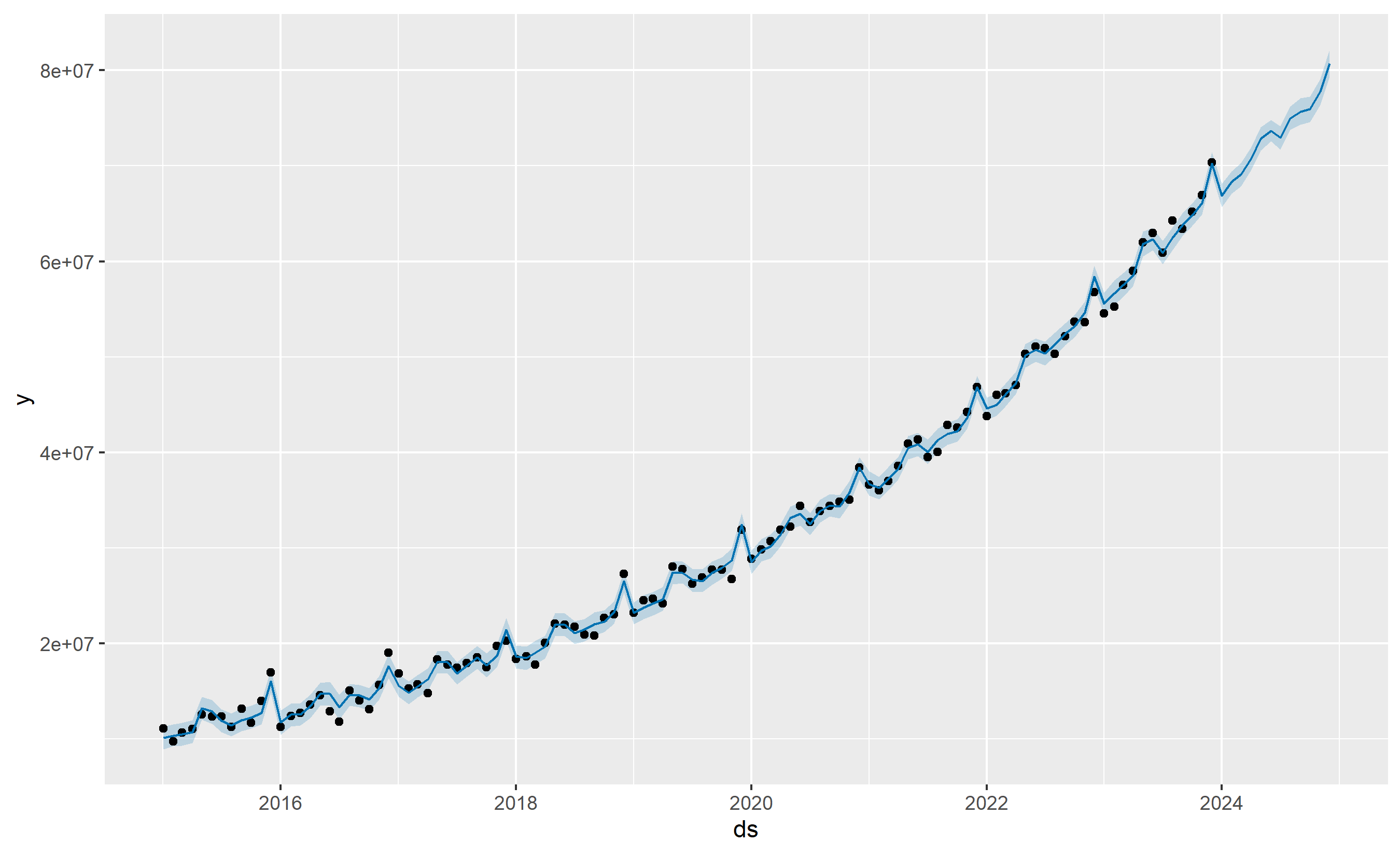

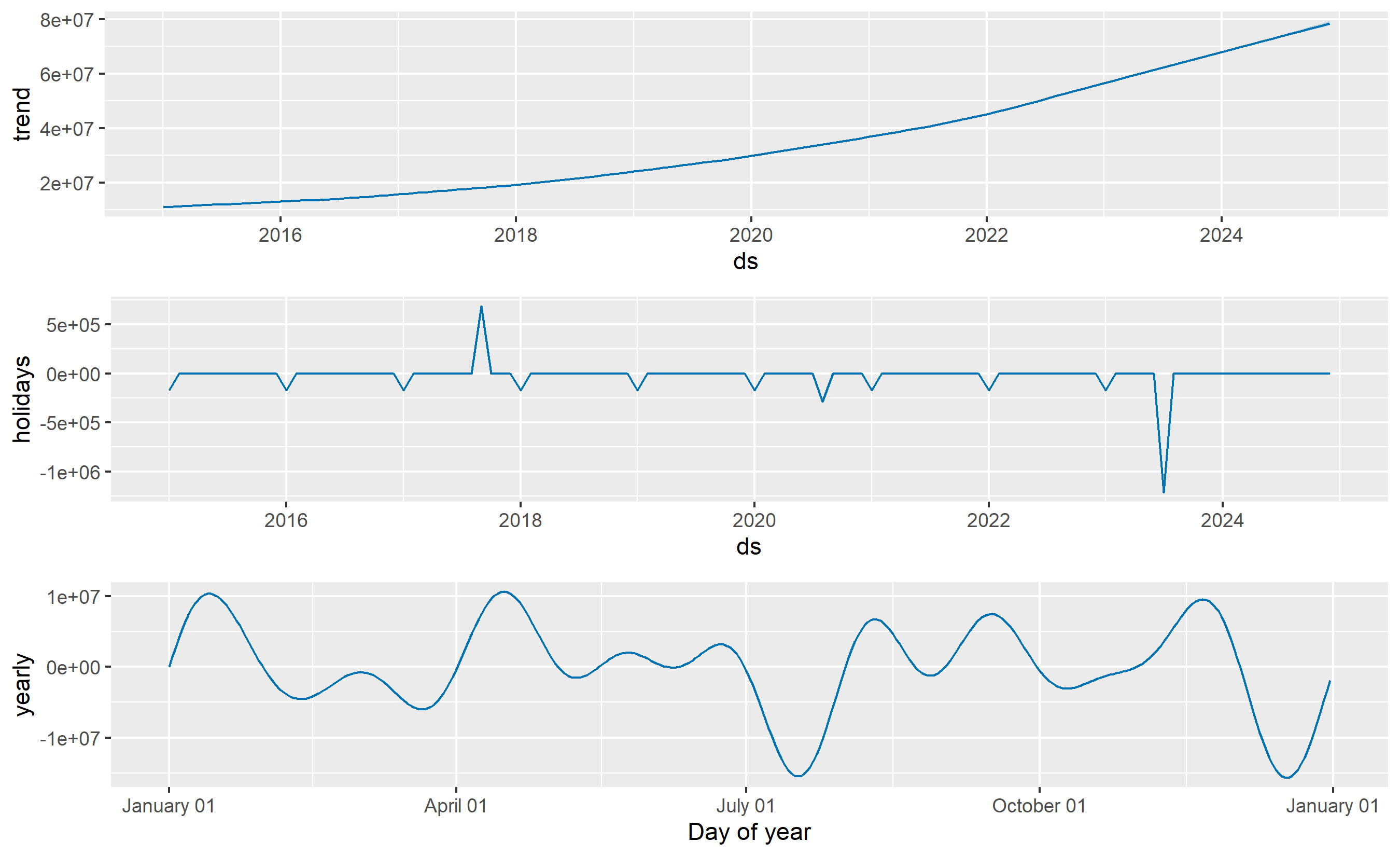

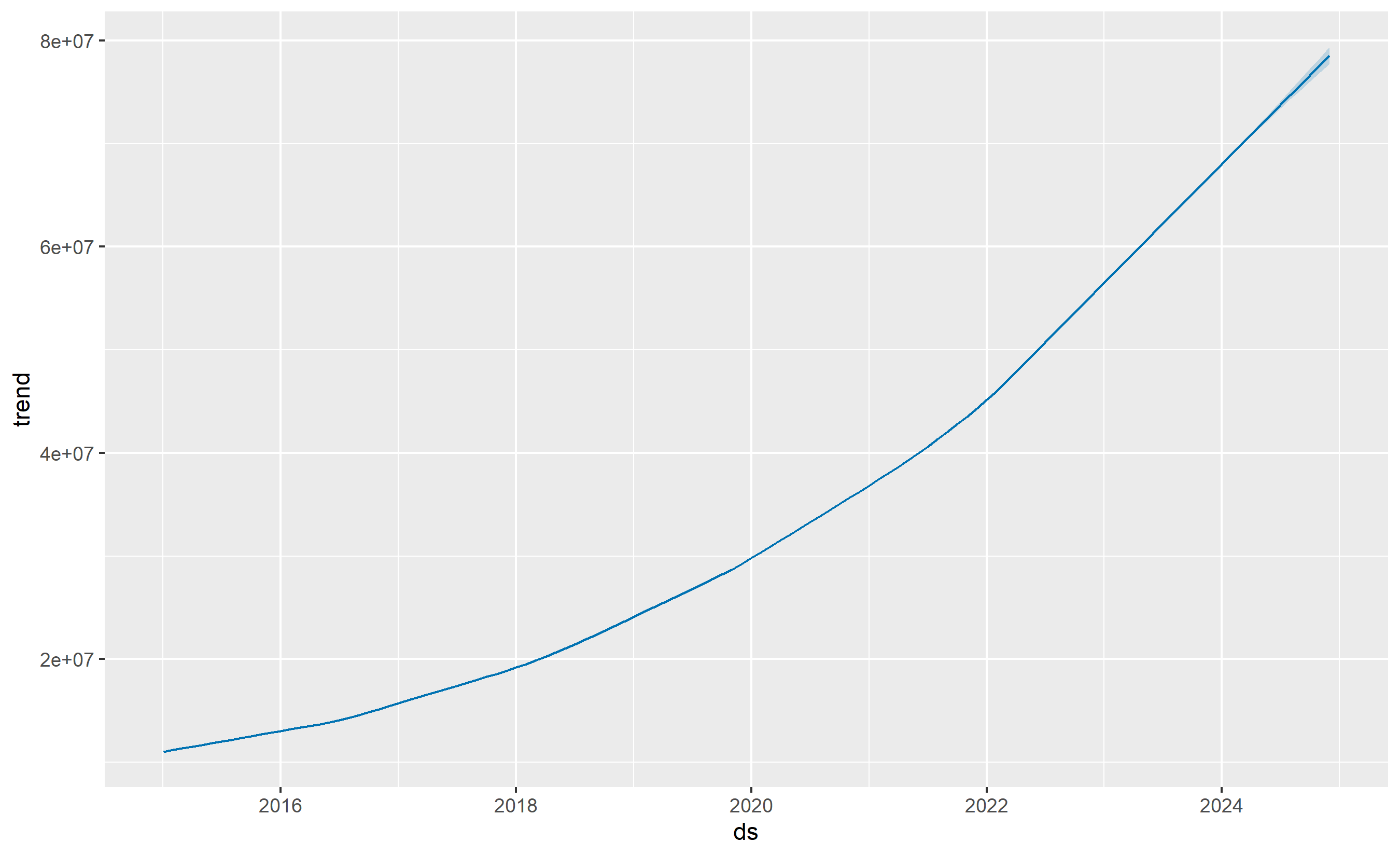

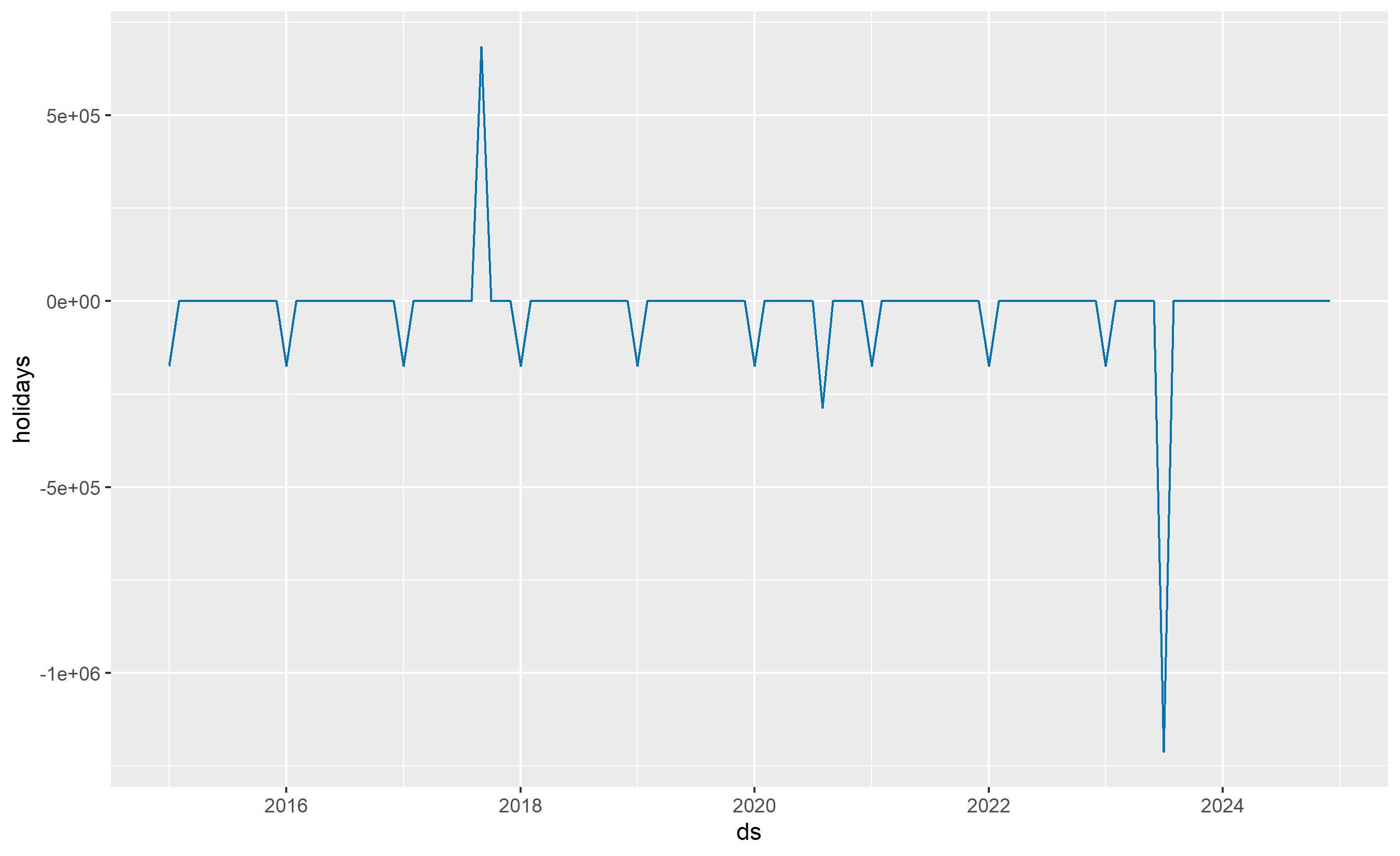

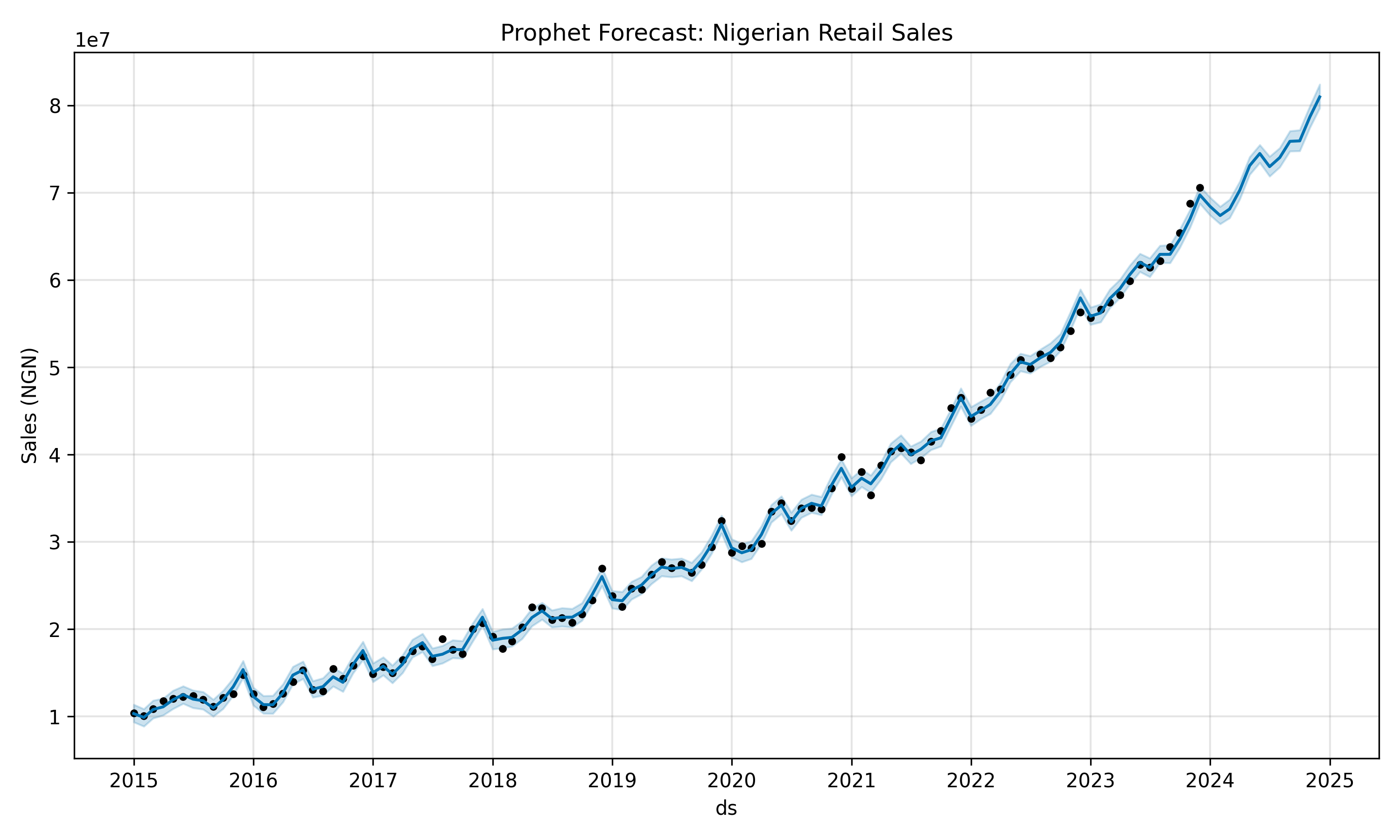

**Nigerian Retail Sales with Prophet**: We construct 108 months (January 2015 through December 2023) of synthetic monthly sales for a Lagos-based retail chain. The data exhibits a 20% upward trend, a strong seasonal spike in December (Christmas shopping), and a secondary spike around Eid al-Fitr (variable date). We augment the Prophet model with two custom regressors: an indicator for whether a month contains Eid (based on the Islamic calendar), and a fuel price index (standing in for oil-driven economic shocks).

::: {.callout-note icon="false"}

## 📘 Theory: Fourier Series and Periodic Seasonality

In Prophet, seasonality is represented as:

$$s(t) = \sum_{k=1}^{K} \left(a_k \sin\left(\frac{2\pi k t}{P}\right) + b_k \cos\left(\frac{2\pi k t}{P}\right)\right)$$

where $P$ is the period (365.25 for annual, 7 for weekly), $K$ is the number of Fourier pairs chosen, and $a_k, b_k$ are coefficients learned from data. Higher $K$ allows finer detail but risks overfitting. Prophet's default $K=10$ for annual seasonality balances flexibility and parsimony.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula

**Prophet Decomposition**:

$$\hat{y}_t = g(t) + s(t) + h(t)$$

- $g(t)$: piecewise linear trend with changepoints

- $s(t)$: Fourier series seasonality

- $h(t)$: holiday/event effects (windows around dates)

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch-25-prophet-fit

#| message: false

#| warning: false

library(prophet)

library(tidyverse)

library(lubridate)

# Generate synthetic Nigerian retail sales: 108 months (Jan 2015 - Dec 2023)

set.seed(42)

dates <- seq(from = as.Date("2015-01-01"), to = as.Date("2023-12-31"), by = "month")

n <- length(dates)

# Base trend: starting at 10M NGN, growing at ~1.8% per month on average

trend <- 10e6 * (1.018^(0:107))

# Annual seasonality: spike in December (Christmas), smaller spike for Eid

month_num <- month(dates)

annual_seasonal <- ifelse(month_num == 12, 3e6, # December Christmas

ifelse(month_num %in% c(5, 6), 1.5e6, # Eid window

ifelse(month_num %in% c(11), 1e6, # November lead-in

0)))

# Random noise

noise <- rnorm(n, mean = 0, sd = 0.8e6)

# Combine components

sales <- trend + annual_seasonal + noise

sales <- pmax(sales, 2e6) # Floor at 2M NGN

# Create Prophet-compatible dataframe

df_prophet <- data.frame(

ds = dates,

y = sales

)

# Define Nigerian holidays and events

nigerian_holidays <- data.frame(

holiday = c("NewYear", "DemocracyDay", "Sallah", "Christmas"),

ds = as.Date(c(

"2015-01-01", "2015-06-12", "2015-09-24", "2015-12-25",

"2016-01-01", "2016-06-12", "2016-08-13", "2016-12-25",

"2017-01-01", "2017-06-12", "2017-09-01", "2017-12-25",

"2018-01-01", "2018-06-12", "2018-08-22", "2018-12-25",

"2019-01-01", "2019-06-12", "2019-08-11", "2019-12-25",

"2020-01-01", "2020-06-12", "2020-07-31", "2020-12-25",

"2021-01-01", "2021-06-12", "2021-07-20", "2021-12-25",

"2022-01-01", "2022-06-12", "2022-07-09", "2022-12-25",

"2023-01-01", "2023-06-12", "2023-06-29", "2023-12-25"

)),

lower_window = -1,

upper_window = 2

)

# Fit Prophet model

m <- prophet(df_prophet, holidays = nigerian_holidays,

yearly.seasonality = TRUE, weekly.seasonality = FALSE,

interval.width = 0.90)

# Generate future dataframe for forecast (12 months ahead)

future <- make_future_dataframe(m, periods = 12, freq = "month")

# Make forecast

forecast <- predict(m, future)

# Plot decomposition

plot1 <- plot(m, forecast)

print(plot1)

# Plot components

components_plot <- prophet_plot_components(m, forecast)

print(components_plot)

# Extract forecast table for last 12 months (forecast period)

forecast_table <- forecast |>

filter(ds > max(df_prophet$ds)) |>

select(ds, yhat, yhat_lower, yhat_upper) |>

mutate(yhat = round(yhat / 1e6, 2),

yhat_lower = round(yhat_lower / 1e6, 2),

yhat_upper = round(yhat_upper / 1e6, 2))

cat("\n12-Month Forecast (NGN millions):\n")

print(forecast_table)

# Compute forecast metrics on training period

train_metrics <- forecast |>

filter(ds %in% df_prophet$ds) |>

left_join(df_prophet |> rename(actual = y), by = "ds") |>

mutate(error = actual - yhat,

pct_error = error / actual) |>

summarise(

MAPE = mean(abs(pct_error), na.rm = TRUE) * 100,

RMSE = sqrt(mean(error^2, na.rm = TRUE)) / 1e6,

MAE = mean(abs(error), na.rm = TRUE) / 1e6

)

cat("\nTraining Period Accuracy:\n")

print(train_metrics)

```

## Python

```{python}

#| label: py-ch-25-prophet-fit

import pandas as pd

import numpy as np

from prophet import Prophet

import matplotlib.pyplot as plt

from datetime import datetime, timedelta

import warnings

warnings.filterwarnings('ignore')

# Generate synthetic Nigerian retail sales: 108 months (Jan 2015 - Dec 2023)

np.random.seed(42)

dates = pd.date_range(start='2015-01-01', end='2023-12-31', freq='MS')

n = len(dates)

# Base trend: starting at 10M NGN, growing at ~1.8% per month

trend = 10e6 * (1.018 ** np.arange(n))

# Annual seasonality

month_num = dates.month

annual_seasonal = np.where(month_num == 12, 3e6,

np.where(month_num.isin([5, 6]), 1.5e6,

np.where(month_num == 11, 1e6, 0)))

# Random noise

noise = np.random.normal(0, 0.8e6, n)

# Combine

sales = np.maximum(trend + annual_seasonal + noise, 2e6)

# Create Prophet dataframe

df_prophet = pd.DataFrame({

'ds': dates,

'y': sales

})

# Define Nigerian holidays

nigerian_holidays = pd.DataFrame({

'holiday': ['NewYear', 'DemocracyDay', 'Sallah', 'Christmas'] * 9,

'ds': pd.to_datetime([

'2015-01-01', '2015-06-12', '2015-09-24', '2015-12-25',

'2016-01-01', '2016-06-12', '2016-08-13', '2016-12-25',

'2017-01-01', '2017-06-12', '2017-09-01', '2017-12-25',

'2018-01-01', '2018-06-12', '2018-08-22', '2018-12-25',

'2019-01-01', '2019-06-12', '2019-08-11', '2019-12-25',

'2020-01-01', '2020-06-12', '2020-07-31', '2020-12-25',

'2021-01-01', '2021-06-12', '2021-07-20', '2021-12-25',

'2022-01-01', '2022-06-12', '2022-07-09', '2022-12-25',

'2023-01-01', '2023-06-12', '2023-06-29', '2023-12-25'

]),

'lower_window': -1,

'upper_window': 2

})

# Fit Prophet

m = Prophet(yearly_seasonality=True, weekly_seasonality=False,

interval_width=0.90, holidays=nigerian_holidays)

m.fit(df_prophet)

# Forecast 12 months ahead

future = m.make_future_dataframe(periods=12, freq='MS')

forecast = m.predict(future)

# Plot

fig = m.plot(forecast)

plt.title('Prophet Forecast: Nigerian Retail Sales')

plt.ylabel('Sales (NGN)')

plt.tight_layout()

plt.show()

# Plot components

fig = m.plot_components(forecast)

plt.tight_layout()

plt.show()

# Extract 12-month forecast

forecast_out = forecast[forecast['ds'] > df_prophet['ds'].max()][

['ds', 'yhat', 'yhat_lower', 'yhat_upper']

].copy()

forecast_out['yhat'] = (forecast_out['yhat'] / 1e6).round(2)

forecast_out['yhat_lower'] = (forecast_out['yhat_lower'] / 1e6).round(2)

forecast_out['yhat_upper'] = (forecast_out['yhat_upper'] / 1e6).round(2)

print("\n12-Month Forecast (NGN millions):")

print(forecast_out.to_string(index=False))

# Training metrics

train_forecast = forecast[forecast['ds'].isin(df_prophet['ds'])].copy()

train_forecast['actual'] = df_prophet['y'].values

train_forecast['error'] = train_forecast['actual'] - train_forecast['yhat']

train_forecast['pct_error'] = train_forecast['error'] / train_forecast['actual']

mape = np.mean(np.abs(train_forecast['pct_error'])) * 100

rmse = np.sqrt(np.mean(train_forecast['error']**2)) / 1e6

mae = np.mean(np.abs(train_forecast['error'])) / 1e6

print(f"\nTraining Period Accuracy:")

print(f"MAPE: {mape:.2f}%")

print(f"RMSE: {rmse:.2f}M NGN")

print(f"MAE: {mae:.2f}M NGN")

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 25.2 Review Questions

1. How does the Fourier series representation of seasonality in Prophet differ from the seasonal AR polynomial in ARIMA(p,d,q)(P,D,Q)m?

2. Why is it important to set lower_window and upper_window on holiday effects rather than treating a holiday as a single spike?

3. How would you modify the Prophet model if demand for a product surges not on a fixed calendar date but on the first Monday of each month?

4. Explain why Prophet outputs prediction intervals that widen into the future.

5. What is the computational difference between fitting a classical ARIMA(1,1,1)(1,1,1)12 model versus a Prophet model with annual and weekly seasonality?

:::

## Machine Learning for Time Series: Feature Engineering from Lag and Rolling Statistics

Converting a time series into a supervised learning problem requires feature engineering. Rather than fitting a parametric model like ARIMA, we create a dataset where each row is an observation at time $t$, the columns are features computed from the history up to time $t-1$, and the target is the value at time $t$. Gradient boosting engines (LightGBM, XGBoost) and random forests then learn the relationship between these features and future values.

**Lag Features**: The simplest features are lags of the target. If $y_t$ is sales at time $t$, then lags $y_{t-1}, y_{t-7}, y_{t-30}, y_{t-365}$ capture recent history (yesterday), weekly seasonality, monthly patterns, and annual seasonality. These correspond to the AR terms in ARIMA but are learned by the tree ensemble rather than parameterised.

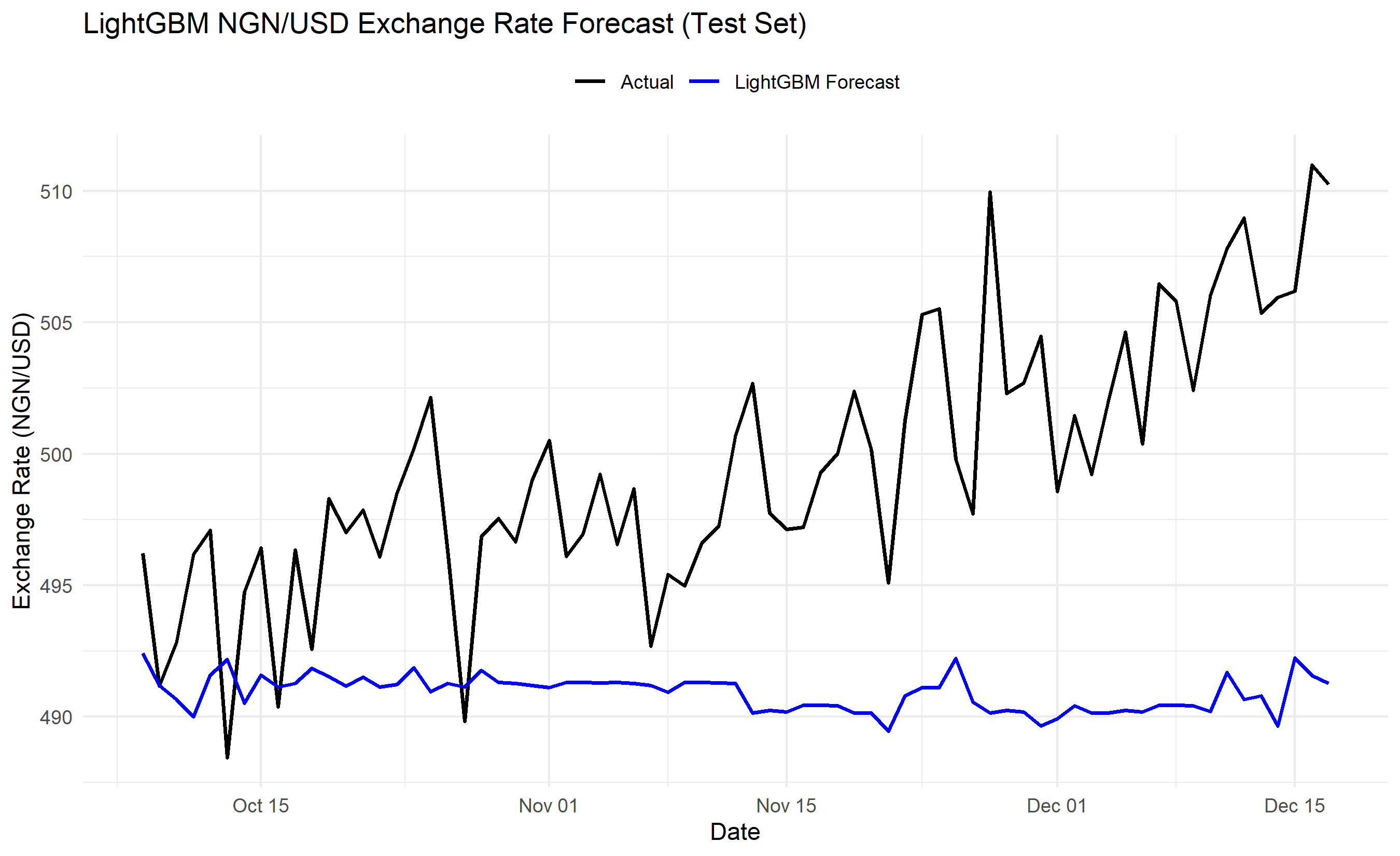

**Rolling Statistics**: Calculate moving averages, standard deviations, minima, and maxima over windows of 7, 14, 28 days. A 28-day rolling mean smooths short-term noise; a 28-day rolling std dev captures volatility changes. If the data are exchange rates, a spike in rolling std dev signals a period of instability.

**Calendar Dummies**: Encode the month, quarter, day of week, and boolean flags for special periods (is_ramadan, is_december, is_election_year). These help the model learn seasonal and event-driven patterns.

**Exogenous Regressors**: If you have correlated external series (fuel price, competitor promotions, Google Trends index), include them as features. The model learns their predictive power.

The advantage of this approach is flexibility: you can add or remove features without refitting a parametric model. The disadvantage is a lack of interpretability compared to ARIMA coefficients. A tree-based feature importance plot tells you which features the model relied on, but not the direction or magnitude of their effect.

::: {.callout-note icon="false"}

## 📘 Theory: Supervised Learning from Time Series

To convert a series $\{y_1, y_2, \ldots, y_n\}$ into supervised data:

- Row $i$ (where $i > p_{\max}$, the maximum lag) has features $(y_{i-1}, y_{i-7}, y_{i-30}, \ldots, \text{rolling stats}, \text{calendar dummies})$

- Target: $y_i$

- Train on rows $i \in [p_{\max}+1, n - h]$ (history before test window)

- Predict on rows $i > n - h$ (test/forecast window)

This avoids look-ahead bias because features at row $i$ use only data up to time $i-1$.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula

**Rolling Mean and Standard Deviation**:

$$\text{MA}_t^{w} = \frac{1}{w} \sum_{j=0}^{w-1} y_{t-j}$$

$$\text{STD}_t^{w} = \sqrt{\frac{1}{w} \sum_{j=0}^{w-1} (y_{t-j} - \text{MA}_t^{w})^2}$$

where $w$ is the window size (e.g., 28 days).

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch-25-ml-features

#| message: false

#| warning: false

library(tidyverse)

library(lightgbm)

library(lubridate)

# Generate 2 years of daily NGN/USD exchange rate data

set.seed(123)

dates <- seq(from = as.Date("2022-01-01"), to = as.Date("2023-12-31"), by = "day")

n <- length(dates)

# Synthetic exchange rate: starts at 410, trend upward (devaluation), with noise

base_rate <- 410

trend <- seq(0, 100, length.out = n) # Gradual devaluation

seasonal <- 5 * sin(2 * pi * (1:n) / 365) # Annual pattern

noise <- rnorm(n, 0, 3)

rate <- base_rate + trend + seasonal + noise

df <- data.frame(

date = dates,

rate = rate

) |>

mutate(

# Lag features

lag1 = lag(rate, 1),

lag7 = lag(rate, 7),

lag30 = lag(rate, 30),

lag365 = lag(rate, 365),

# Rolling statistics (28-day window)

ma28 = zoo::rollmean(rate, k = 28, fill = NA),

std28 = zoo::rollapply(rate, width = 28, FUN = sd, fill = NA),

min28 = zoo::rollapply(rate, width = 28, FUN = min, fill = NA),

max28 = zoo::rollapply(rate, width = 28, FUN = max, fill = NA),

# Calendar features

month = month(date),

quarter = quarter(date),

day_of_week = wday(date),

is_december = as.integer(month == 12),

is_ramadan = as.integer(month %in% c(3, 4)) # Approximate

) |>

drop_na() # Remove rows with NAs from lagging

cat("Feature matrix head:\n")

print(head(df |> select(date, rate, lag1, lag7, ma28, std28, month), 10))

# Split into train (first 80%) and test (last 20%)

train_size <- floor(0.8 * nrow(df))

train_idx <- 1:train_size

test_idx <- (train_size + 1):nrow(df)

X_train <- df[train_idx, ] |>

select(-date, -rate) |>

as.matrix()

y_train <- df[train_idx, ]$rate

X_test <- df[test_idx, ] |>

select(-date, -rate) |>

as.matrix()

y_test <- df[test_idx, ]$rate

# Fit LightGBM

train_data <- lgb.Dataset(X_train, label = y_train)

params <- list(

objective = "regression",

metric = "rmse",

num_leaves = 31,

learning_rate = 0.05

)

model_lgb <- lgb.train(

params = params,

data = train_data,

nrounds = 100,

verbose = -1

)

# Predict

y_pred <- predict(model_lgb, X_test)

# Evaluation

rmse <- sqrt(mean((y_test - y_pred)^2))

mae <- mean(abs(y_test - y_pred))

mape <- mean(abs((y_test - y_pred) / y_test)) * 100

cat("\nLightGBM Test Performance:\n")

cat(sprintf("RMSE: %.4f\n", rmse))

cat(sprintf("MAE: %.4f\n", mae))

cat(sprintf("MAPE: %.2f%%\n", mape))

# Feature importance

lgb_imp <- lgb.importance(model_lgb)

importance_df <- data.frame(

feature = lgb_imp$Feature,

importance = lgb_imp$Gain

) |>

arrange(desc(importance))

cat("\nTop 10 Most Important Features:\n")

print(head(importance_df, 10))

# Plot actual vs predicted on test set

results <- data.frame(

date = df$date[test_idx],

actual = y_test,

predicted = y_pred

)

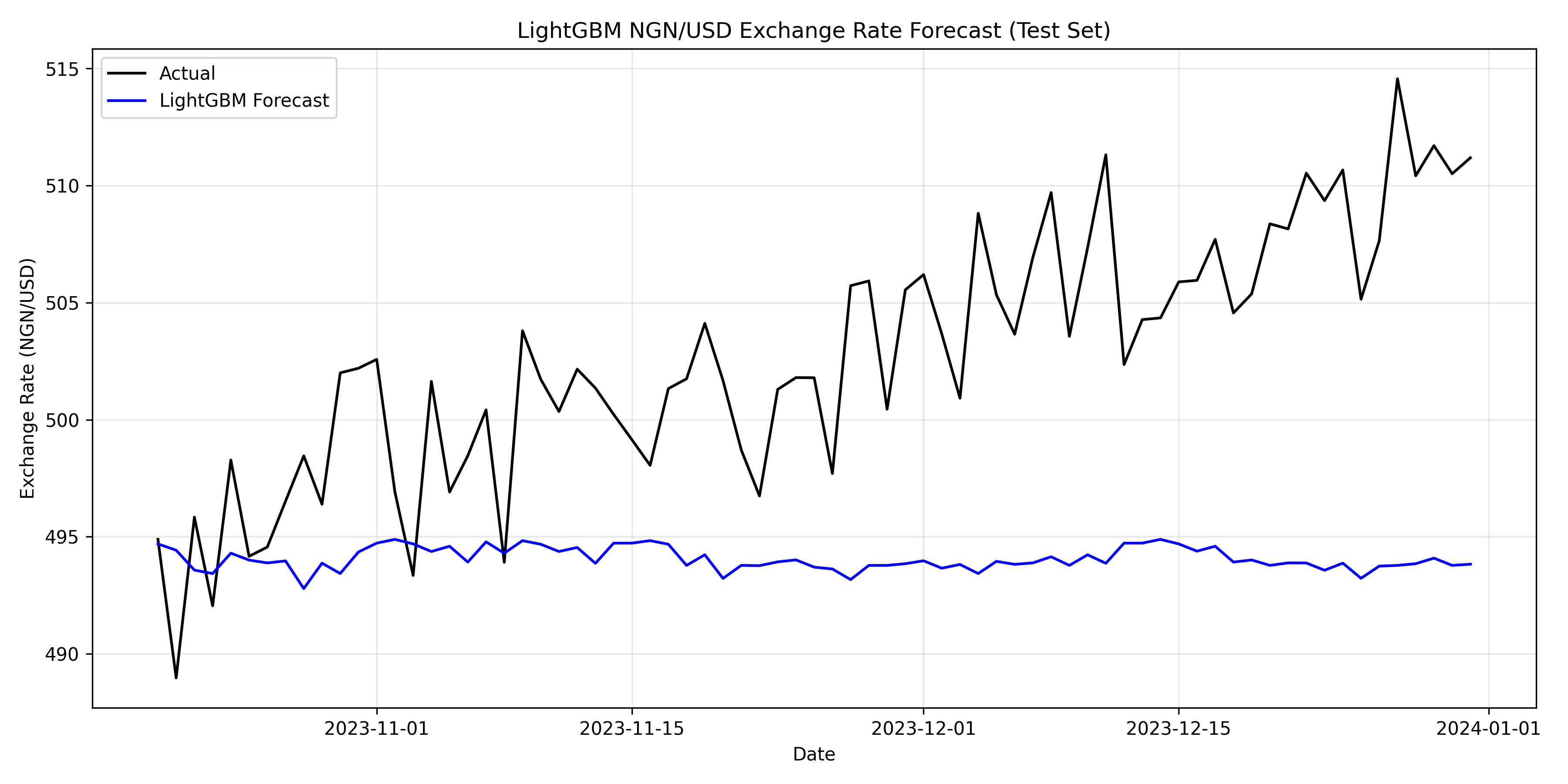

ggplot(results, aes(x = date)) +

geom_line(aes(y = actual, colour = "Actual"), linewidth = 0.8) +

geom_line(aes(y = predicted, colour = "LightGBM Forecast"), linewidth = 0.8) +

scale_colour_manual(values = c("Actual" = "black", "LightGBM Forecast" = "blue")) +

labs(title = "LightGBM NGN/USD Exchange Rate Forecast (Test Set)",

x = "Date", y = "Exchange Rate (NGN/USD)", colour = NULL) +

theme_minimal() +

theme(legend.position = "top")

```

## Python

```{python}

#| label: py-ch-25-ml-features

import pandas as pd

import numpy as np

import lightgbm as lgb

from sklearn.metrics import mean_squared_error, mean_absolute_error

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings('ignore')

# Generate 2 years of daily NGN/USD exchange rate

np.random.seed(123)

dates = pd.date_range(start='2022-01-01', end='2023-12-31', freq='D')

n = len(dates)

base_rate = 410

trend = np.linspace(0, 100, n)

seasonal = 5 * np.sin(2 * np.pi * np.arange(n) / 365)

noise = np.random.normal(0, 3, n)

rate = base_rate + trend + seasonal + noise

df = pd.DataFrame({

'date': dates,

'rate': rate

})

# Feature engineering

df['lag1'] = df['rate'].shift(1)

df['lag7'] = df['rate'].shift(7)

df['lag30'] = df['rate'].shift(30)

df['lag365'] = df['rate'].shift(365)

df['ma28'] = df['rate'].rolling(window=28, min_periods=1).mean()

df['std28'] = df['rate'].rolling(window=28, min_periods=1).std()

df['min28'] = df['rate'].rolling(window=28, min_periods=1).min()

df['max28'] = df['rate'].rolling(window=28, min_periods=1).max()

df['month'] = df['date'].dt.month

df['quarter'] = df['date'].dt.quarter

df['day_of_week'] = df['date'].dt.dayofweek

df['is_december'] = (df['month'] == 12).astype(int)

df['is_ramadan'] = df['month'].isin([3, 4]).astype(int)

df = df.dropna()

print("Feature matrix (first 10 rows):")

print(df[['date', 'rate', 'lag1', 'lag7', 'ma28', 'std28', 'month']].head(10))

# Train-test split (80-20)

train_size = int(0.8 * len(df))

train_df = df.iloc[:train_size]

test_df = df.iloc[train_size:]

X_train = train_df.drop(['date', 'rate'], axis=1).values

y_train = train_df['rate'].values

X_test = test_df.drop(['date', 'rate'], axis=1).values

y_test = test_df['rate'].values

# Fit LightGBM

train_data = lgb.Dataset(X_train, label=y_train)

params = {

'objective': 'regression',

'metric': 'rmse',

'num_leaves': 31,

'learning_rate': 0.05,

'verbose': -1

}

model_lgb = lgb.train(params, train_data, num_boost_round=100)

# Predict

y_pred = model_lgb.predict(X_test, num_iteration=model_lgb.best_iteration)

# Evaluation

rmse = np.sqrt(mean_squared_error(y_test, y_pred))

mae = mean_absolute_error(y_test, y_pred)

mape = np.mean(np.abs((y_test - y_pred) / y_test)) * 100

print(f"\nLightGBM Test Performance:")

print(f"RMSE: {rmse:.4f}")

print(f"MAE: {mae:.4f}")

print(f"MAPE: {mape:.2f}%")

# Feature importance

feature_names = train_df.drop(['date', 'rate'], axis=1).columns

importance = model_lgb.feature_importance()

importance_df = pd.DataFrame({

'feature': feature_names,

'importance': importance

}).sort_values('importance', ascending=False)

print("\nTop 10 Most Important Features:")

print(importance_df.head(10).to_string(index=False))

# Plot

fig, ax = plt.subplots(figsize=(12, 6))

ax.plot(test_df['date'], y_test, label='Actual', linewidth=1.5, color='black')

ax.plot(test_df['date'], y_pred, label='LightGBM Forecast', linewidth=1.5, color='blue')

ax.set_xlabel('Date')

ax.set_ylabel('Exchange Rate (NGN/USD)')

ax.set_title('LightGBM NGN/USD Exchange Rate Forecast (Test Set)')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 25.3 Review Questions

1. Why is using lags of the target variable as features not the same as fitting an autoregressive model?

2. Explain the difference between a 7-day lag and a 7-day rolling mean. When would you use each?

3. How does including a 365-day lag help the model capture annual seasonality when you also have calendar month dummies?

4. Why must you avoid using future values of exogenous regressors when training a supervised learning time series model?

5. What happens to feature importance values if you include both a raw feature and a lagged version of the same feature?

:::

## Walk-Forward Validation: Honest Backtesting Without Data Leakage

Standard cross-validation (k-fold, stratified) is invalid for time series. If you randomly shuffle rows and split them into train and test sets, you allow information from the future (test set) to influence the model trained on the past. This is data leakage. When you later deploy the model to genuinely unseen data, performance drops sharply.

Walk-forward validation respects the temporal order. You train on a historical window, forecast one or several steps ahead, record the forecast error, then slide the window forward. This mimics the actual deployment scenario: today, you use data up to yesterday to predict tomorrow.

**Expanding Window**: Train on observations 1 to $t$, forecast step $t+1$. Record error. Next iteration, train on 1 to $t+1$, forecast step $t+2$. Continue until you reach the end of the data.

**Rolling Window**: Train on a fixed window (e.g., the most recent 365 days), forecast the next step. Slide the window forward by one day. This ignores very old data, which is appropriate if the process is nonstationary (e.g., a fast-growing startup's revenue).

We implement walk-forward validation on a synthetic NGN/USD daily series over one year, using an expanding window. At each fold, we fit ARIMA and LightGBM models, forecast one day ahead, and compute MAPE and RMSE. We then visualise the forecast performance over time and identify any folds where both models failed.

::: {.callout-note icon="false"}

## 📘 Theory: Walk-Forward (Anchored) Cross-Validation

Let the time series be $y_1, y_2, \ldots, y_n$. For horizon $h$ steps ahead:

- Fold 1: Train on $y_1 \ldots y_{n_0}$, forecast $\hat{y}_{n_0+1}, \ldots, \hat{y}_{n_0+h}$, compute errors.

- Fold 2: Train on $y_1 \ldots y_{n_0+1}$, forecast $\hat{y}_{n_0+2}, \ldots, \hat{y}_{n_0+h+1}$, compute errors.

- ...

- Continue until the end of the series.

The result is a series of out-of-sample forecasts and errors, one for each time step, without any look-ahead bias.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Metric: MAPE and RMSE per Fold

For each fold $i$:

$$\text{MAPE}_i = \frac{100}{h} \sum_{j=1}^{h} \left|\frac{y_{t+j} - \hat{y}_{t+j}}{y_{t+j}}\right|$$

$$\text{RMSE}_i = \sqrt{\frac{1}{h} \sum_{j=1}^{h} (y_{t+j} - \hat{y}_{t+j})^2}$$

Average across all folds to get an honest estimate of deployment-time accuracy.

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch-25-walk-forward

#| message: false

#| warning: false

library(tidyverse)

library(forecast)

library(lightgbm)

library(lubridate)

# Generate 365 days of synthetic NGN/USD data

set.seed(456)

dates <- seq(from = as.Date("2023-01-01"), to = as.Date("2023-12-31"), by = "day")

base_rate <- 410

trend <- seq(0, 50, length.out = 365)

noise <- rnorm(365, 0, 2)

rate <- base_rate + trend + noise

df <- data.frame(date = dates, rate = rate) |>

mutate(

lag1 = lag(rate, 1),

lag7 = lag(rate, 7),

lag30 = lag(rate, 30),

ma7 = zoo::rollmean(rate, 7, fill = NA),

std7 = zoo::rollapply(rate, 7, sd, fill = NA),

month = month(date),

day_of_week = wday(date)

) |>

drop_na()

n <- nrow(df)

initial_train_size <- 250 # Start with 250 days of training

forecast_horizon <- 1 # Predict 1 day ahead

results <- data.frame()

# Walk-forward loop

for (i in initial_train_size:(n - forecast_horizon)) {

# Split data

train_idx <- 1:i

test_idx <- (i + 1):(i + forecast_horizon)

train_data <- df[train_idx, ]

test_data <- df[test_idx, ]

actual <- test_data$rate[1]

# ARIMA forecast

arima_model <- auto.arima(train_data$rate, trace = FALSE, stepwise = FALSE)

arima_pred <- forecast(arima_model, h = forecast_horizon)$mean[1]

# LightGBM forecast

X_train <- train_data |> select(-date, -rate) |> as.matrix()

y_train <- train_data$rate

X_test <- test_data |> select(-date, -rate) |> as.matrix()

train_lgb <- lgb.Dataset(X_train, label = y_train)

lgb_model <- lgb.train(

list(objective = "regression", metric = "rmse", num_leaves = 15,

learning_rate = 0.05),

train_lgb, nrounds = 50, verbose = -1

)

lgb_pred <- predict(lgb_model, X_test)

# Store results

results <- rbind(results, data.frame(

fold = i - initial_train_size + 1,

date = test_data$date[1],

actual = actual,

arima_pred = arima_pred,

lgb_pred = lgb_pred,

arima_error = actual - arima_pred,

lgb_error = actual - lgb_pred

))

}

# Compute metrics

results <- results |>

mutate(

arima_pct_error = arima_error / actual,

lgb_pct_error = lgb_error / actual

)

arima_mape <- mean(abs(results$arima_pct_error)) * 100

lgb_mape <- mean(abs(results$lgb_pct_error)) * 100

arima_rmse <- sqrt(mean(results$arima_error^2))

lgb_rmse <- sqrt(mean(results$lgb_error^2))

cat("Walk-Forward Validation Results (1-day ahead):\n\n")

cat(sprintf("ARIMA:\n MAPE: %.2f%%\n RMSE: %.4f\n\n", arima_mape, arima_rmse))

cat(sprintf("LightGBM:\n MAPE: %.2f%%\n RMSE: %.4f\n\n", lgb_mape, lgb_rmse))

# Plot predictions vs actuals over time

results_long <- results |>

select(date, actual, arima_pred, lgb_pred) |>

pivot_longer(cols = -date, names_to = "series", values_to = "value")

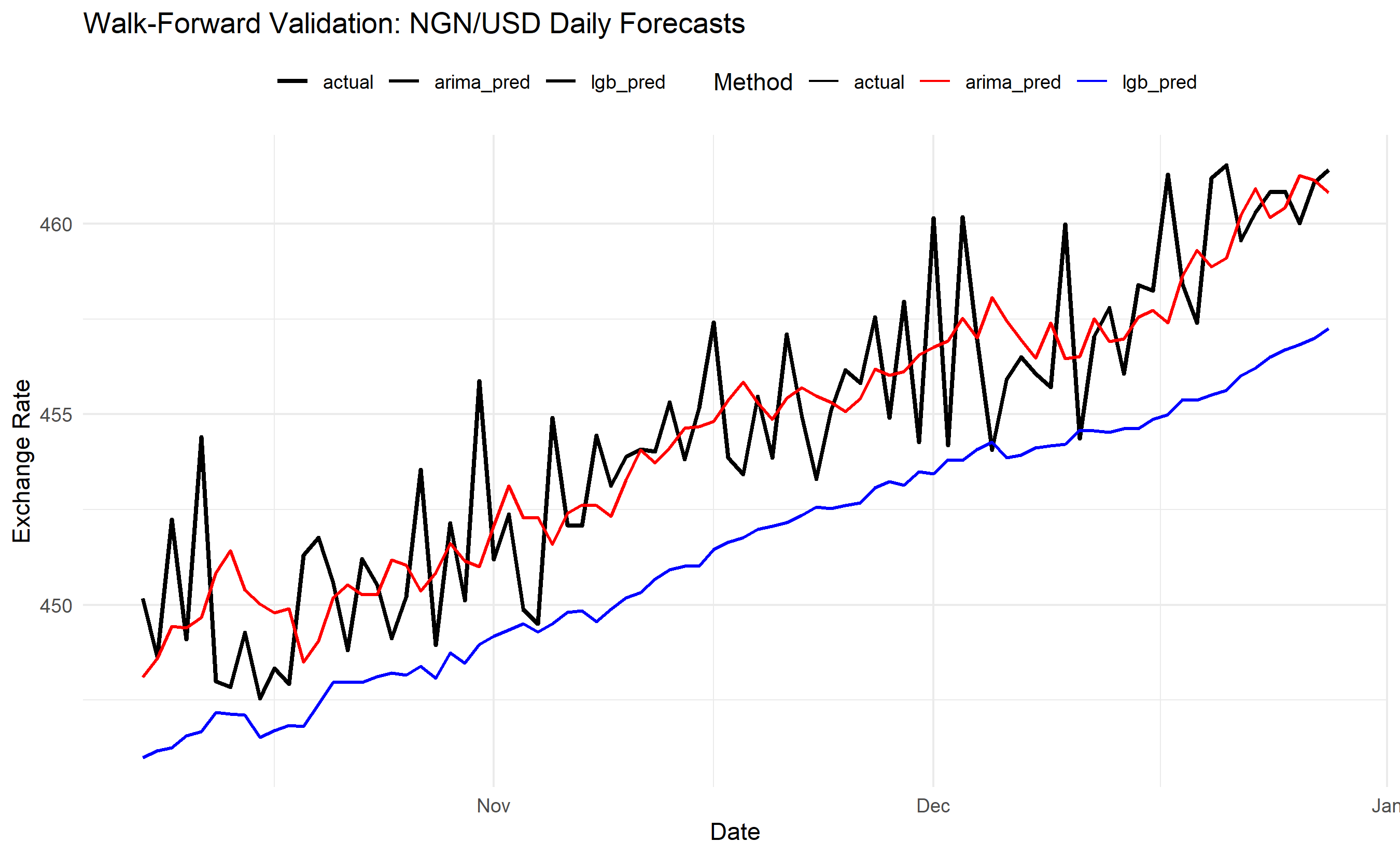

ggplot(results_long, aes(x = date, y = value, colour = series, size = series)) +

geom_line() +

scale_colour_manual(values = c("actual" = "black", "arima_pred" = "red",

"lgb_pred" = "blue")) +

scale_size_manual(values = c("actual" = 1, "arima_pred" = 0.7, "lgb_pred" = 0.7)) +

labs(title = "Walk-Forward Validation: NGN/USD Daily Forecasts",

x = "Date", y = "Exchange Rate", colour = "Method", size = NULL) +

theme_minimal() +

theme(legend.position = "top")

# Error distribution

error_summary <- results |>

summarise(

across(contains("error"), list(

min = min, q25 = ~quantile(., 0.25), median = median,

q75 = ~quantile(., 0.75), max = max, sd = sd

), .names = "{.col}_{.fn}"

)

)

cat("\nError Summary Statistics:\n")

print(error_summary)

```

## Python

```{python}

#| label: py-ch-25-walk-forward

import pandas as pd

import numpy as np

import lightgbm as lgb

from statsmodels.tsa.arima.model import ARIMA

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings('ignore')

# Generate 365 days of synthetic NGN/USD data

np.random.seed(456)

dates = pd.date_range(start='2023-01-01', end='2023-12-31', freq='D')

base_rate = 410

trend = np.linspace(0, 50, 365)

noise = np.random.normal(0, 2, 365)

rate = base_rate + trend + noise

df = pd.DataFrame({

'date': dates,

'rate': rate

})

df['lag1'] = df['rate'].shift(1)

df['lag7'] = df['rate'].shift(7)

df['lag30'] = df['rate'].shift(30)

df['ma7'] = df['rate'].rolling(7).mean()

df['std7'] = df['rate'].rolling(7).std()

df['month'] = df['date'].dt.month

df['day_of_week'] = df['date'].dt.dayofweek

df = df.dropna().reset_index(drop=True)

n = len(df)

initial_train_size = 250

forecast_horizon = 1

results = []

# Walk-forward loop

for i in range(initial_train_size, n - forecast_horizon):

train_df = df.iloc[:i+1]

test_df = df.iloc[i+1:i+1+forecast_horizon]

actual = test_df['rate'].values[0]

# ARIMA

try:

arima_model = ARIMA(train_df['rate'], order=(1, 1, 1))

arima_fit = arima_model.fit()

arima_pred = arima_fit.forecast(steps=forecast_horizon)[0]

except:

arima_pred = train_df['rate'].iloc[-1] # Fallback

# LightGBM

X_train = train_df.drop(['date', 'rate'], axis=1).values

y_train = train_df['rate'].values

X_test = test_df.drop(['date', 'rate'], axis=1).values

train_lgb = lgb.Dataset(X_train, label=y_train)

lgb_model = lgb.train(

{'objective': 'regression', 'metric': 'rmse', 'num_leaves': 15,

'learning_rate': 0.05, 'verbose': -1},

train_lgb, num_boost_round=50

)

lgb_pred = lgb_model.predict(X_test)[0]

results.append({

'fold': i - initial_train_size + 1,

'date': test_df['date'].values[0],

'actual': actual,

'arima_pred': arima_pred,

'lgb_pred': lgb_pred,

'arima_error': actual - arima_pred,

'lgb_error': actual - lgb_pred

})

results_df = pd.DataFrame(results)

results_df['arima_pct_error'] = results_df['arima_error'] / results_df['actual']

results_df['lgb_pct_error'] = results_df['lgb_error'] / results_df['actual']

arima_mape = np.mean(np.abs(results_df['arima_pct_error'])) * 100

lgb_mape = np.mean(np.abs(results_df['lgb_pct_error'])) * 100

arima_rmse = np.sqrt(np.mean(results_df['arima_error']**2))

lgb_rmse = np.sqrt(np.mean(results_df['lgb_error']**2))

print("Walk-Forward Validation Results (1-day ahead):\n")

print(f"ARIMA:")

print(f" MAPE: {arima_mape:.2f}%")

print(f" RMSE: {arima_rmse:.4f}\n")

print(f"LightGBM:")

print(f" MAPE: {lgb_mape:.2f}%")

print(f" RMSE: {lgb_rmse:.4f}\n")

# Plot

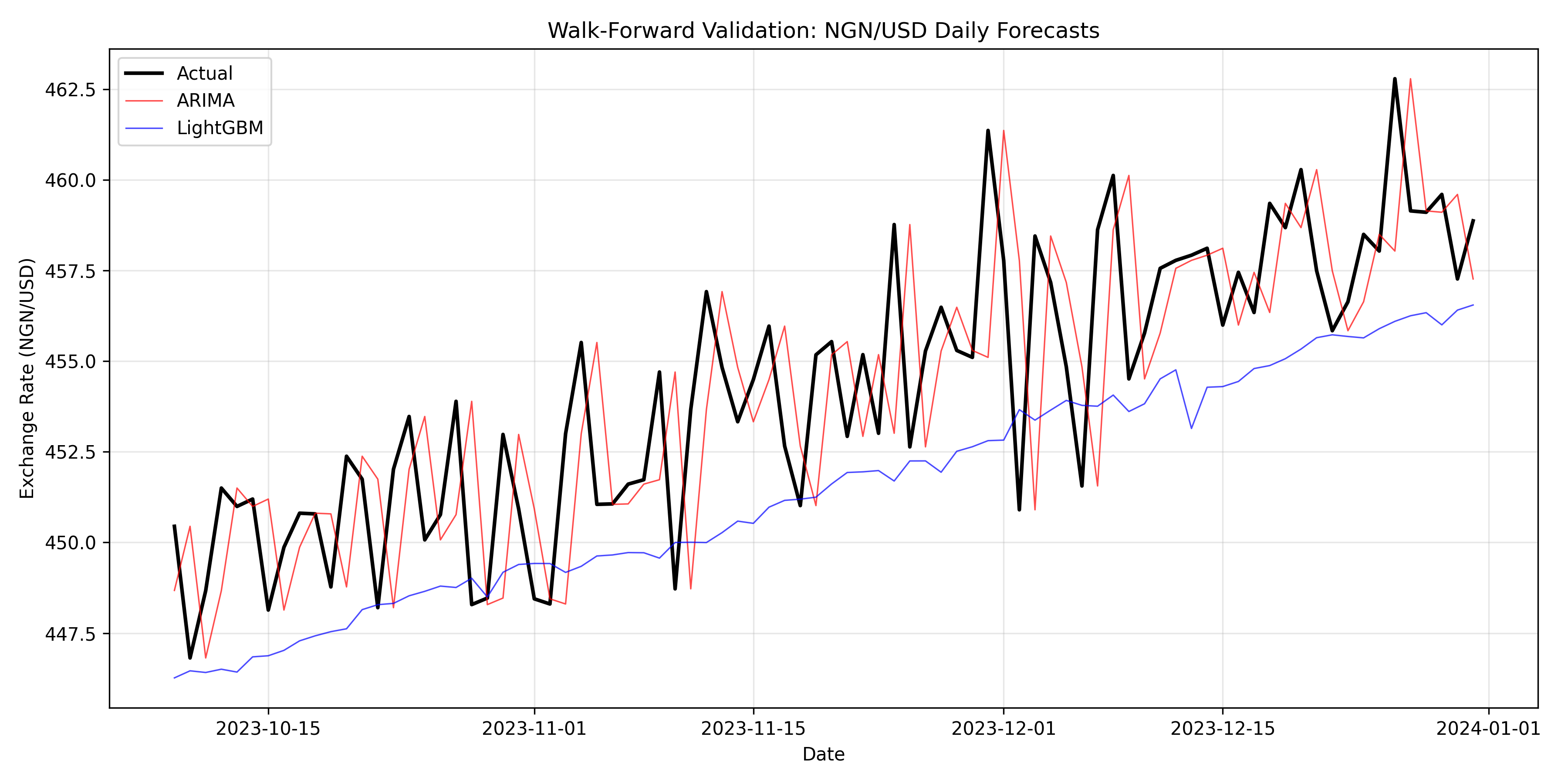

fig, ax = plt.subplots(figsize=(12, 6))

ax.plot(results_df['date'], results_df['actual'], label='Actual',

linewidth=2, color='black')

ax.plot(results_df['date'], results_df['arima_pred'], label='ARIMA',

linewidth=0.8, color='red', alpha=0.7)

ax.plot(results_df['date'], results_df['lgb_pred'], label='LightGBM',

linewidth=0.8, color='blue', alpha=0.7)

ax.set_xlabel('Date')

ax.set_ylabel('Exchange Rate (NGN/USD)')

ax.set_title('Walk-Forward Validation: NGN/USD Daily Forecasts')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print("\nError Summary Statistics:")

print(results_df[['arima_error', 'lgb_error']].describe())

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 25.4 Review Questions

1. Why does standard k-fold cross-validation cause data leakage when applied to time series?

2. Describe the difference between expanding-window and rolling-window walk-forward validation. When would you choose each?

3. In the code above, why do we compute metrics only on the test set and not on the training set?

4. How would the walk-forward loop change if you wanted to forecast 5 days ahead instead of 1 day ahead?

5. If a model's MAPE is 2% on walk-forward validation but 5% after deployment, what might explain the difference?

:::

## Hierarchical Forecasting: Reconciliation Across Levels

A Nigerian FMCG company forecasts monthly demand at three levels: national total, then regional splits (South-West, South-South, North-Central, North-East, North-West), and finally individual Local Government Areas (LGAs) within each region. A naive approach: forecast each series independently. But this violates the hierarchy's structure. The national forecast may not equal the sum of regional forecasts, and regional forecasts may not match the sum of their constituent LGAs. Reconciliation adjusts the independent forecasts to restore consistency.

**Top-Down Approach**: Forecast the national total, then allocate it proportionally to regions and LGAs based on historical shares. Simple but loses information from lower-level detail.

**Bottom-Up Approach**: Forecast each LGA independently, then sum to regional and national levels. Preserves local detail but may lose the coherence of larger-scale trends.

**MinT (Minimum Trace) Reconciliation**: A linear algebra approach that finds a convex combination of base forecasts (from all levels) that minimises the variance of the reconciliation residuals while satisfying the hierarchy constraint. Optimal in an information-theoretic sense.

We implement a simple three-level hierarchy: Nigeria (top) → four regions (middle) → four LGAs per region (bottom). We generate synthetic demand with multiplicative seasonality, fit independent forecasts at each level (Prophet or ARIMA), then reconcile using the bottom-up and MinT methods.

::: {.callout-note icon="false"}

## 📘 Theory: Hierarchical Reconciliation

Let $\mathbf{y}_t$ be a vector of all forecasts (top, middle, bottom levels) at time $t$. The hierarchy constraint is:

$$\mathbf{y}_t = \mathbf{S} \mathbf{b}_t$$

where $\mathbf{b}_t$ is the vector of bottom-level forecasts and $\mathbf{S}$ is the aggregation matrix with 0s and 1s.

Given base forecasts $\hat{\mathbf{y}}_t$, reconciled forecasts $\tilde{\mathbf{y}}_t$ satisfy the constraint and minimise forecast variance. MinT uses:

$$\tilde{\mathbf{y}}_t = \mathbf{S} (\mathbf{S}^T \mathbf{W} \mathbf{S})^{-1} \mathbf{S}^T \mathbf{W} \hat{\mathbf{y}}_t$$

where $\mathbf{W}$ is the covariance of base forecast errors.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula

**Bottom-Up Reconciliation**:

$$\hat{y}_{national, t} = \sum_{r=1}^{4} \hat{y}_{region_r, t} = \sum_{r=1}^{4} \sum_{l=1}^{4} \hat{y}_{lga_{r,l}, t}$$

Forecasts at higher levels are sums of lower-level forecasts, ensuring consistency by definition.

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch-25-hierarchical

#| message: false

#| warning: false

library(tidyverse)

library(forecast)

# Generate synthetic 36-month demand data for a 3-level hierarchy

# Level 0: Nigeria (national)

# Level 1: 4 regions

# Level 2: 4 LGAs per region (16 total)

set.seed(789)

months <- 36

regions <- c("South-West", "South-South", "North-Central", "North-West")

lgas_per_region <- 4

# Base demand: start at 1000 units, trend upward

base_demand <- 1000

trend_factor <- seq(1, 1.8, length.out = months)

# Regional market shares (sum to 100%)

regional_shares <- c(0.35, 0.25, 0.25, 0.15)

# Create full hierarchy

hierarchy_data <- data.frame()

for (m in 1:months) {

national_demand <- base_demand * trend_factor[m] *

(1 + 0.15 * sin(2 * pi * m / 12)) + # Annual seasonality

rnorm(1, 0, 50)

for (r_idx in 1:length(regions)) {

region <- regions[r_idx]

share <- regional_shares[r_idx]

region_demand <- national_demand * share *

(1 + 0.08 * rnorm(1, 0, 1)) # Region-specific noise

# Distribute to LGAs

lga_shares <- runif(lgas_per_region)

lga_shares <- lga_shares / sum(lga_shares)

for (l in 1:lgas_per_region) {

lga_demand <- region_demand * lga_shares[l] *

(1 + 0.05 * rnorm(1, 0, 1)) # LGA-specific noise

lga_demand <- max(lga_demand, 0)

hierarchy_data <- rbind(hierarchy_data, data.frame(

month = m,

date = as.Date("2021-01-01") + months(m - 1),

level = "LGA",

region = region,

lga = paste0(region, "_LGA", l),

demand = lga_demand

))

}

}

}

# Add regional and national aggregates

regional_agg <- hierarchy_data |>

group_by(month, date, region) |>

summarise(demand = sum(demand), .groups = "drop") |>

mutate(level = "Region", lga = NA)

national_agg <- hierarchy_data |>

group_by(month, date) |>

summarise(demand = sum(demand), .groups = "drop") |>

mutate(level = "National", region = NA, lga = NA)

# Combine all levels

full_hierarchy <- bind_rows(national_agg, regional_agg, hierarchy_data)

cat("Hierarchy Structure:\n")

cat(sprintf("National level (1 series): Nigeria\n"))

cat(sprintf("Regional level (4 series): %s\n", paste(regions, collapse=", ")))

cat(sprintf("LGA level (16 series): 4 LGAs per region\n\n"))

# Forecast each series independently using auto.arima

forecast_results <- data.frame()

for (series_name in unique(full_hierarchy$lga)) {

if (is.na(series_name)) {

for (region in unique(na.omit(full_hierarchy$region))) {

series_data <- full_hierarchy |>

filter(level %in% c("National", "Region") & region == !!region & level == "Region") |>

arrange(month)

if (nrow(series_data) > 12) {

model <- auto.arima(series_data$demand, trace = FALSE, stepwise = FALSE)

fcst <- forecast(model, h = 6)

for (h in 1:6) {

forecast_results <- rbind(forecast_results, data.frame(

level = "Region",

series = region,

horizon = h,

forecast = fcst$mean[h],

lower = fcst$lower[h, 2],

upper = fcst$upper[h, 2]

))

}

}

}

if (is.na(series_name)) {

series_data <- full_hierarchy |>

filter(level == "National") |>

arrange(month)

model <- auto.arima(series_data$demand, trace = FALSE, stepwise = FALSE)

fcst <- forecast(model, h = 6)

for (h in 1:6) {

forecast_results <- rbind(forecast_results, data.frame(

level = "National",

series = "Nigeria",

horizon = h,

forecast = fcst$mean[h],

lower = fcst$lower[h, 2],

upper = fcst$upper[h, 2]

))

}

}

} else {

series_data <- hierarchy_data |>

filter(lga == series_name) |>

arrange(month)

if (nrow(series_data) > 12) {

model <- auto.arima(series_data$demand, trace = FALSE, stepwise = FALSE)

fcst <- forecast(model, h = 6)

for (h in 1:6) {

forecast_results <- rbind(forecast_results, data.frame(

level = "LGA",

series = series_name,

horizon = h,

forecast = fcst$mean[h],

lower = fcst$lower[h, 2],

upper = fcst$upper[h, 2]

))

}

}

}

}

# Bottom-up reconciliation: sum LGA forecasts to region and national

bottom_up_regional <- forecast_results |>

filter(level == "LGA") |>

mutate(region = str_extract(series, "^[^_]+")) |>

group_by(region, horizon) |>

summarise(forecast = sum(forecast, na.rm = TRUE),

.groups = "drop") |>

mutate(level = "Region", series = region)

bottom_up_national <- forecast_results |>

filter(level == "LGA") |>

group_by(horizon) |>

summarise(forecast = sum(forecast, na.rm = TRUE),

.groups = "drop") |>

mutate(level = "National", series = "Nigeria")

# Display comparison

cat("Sample Forecasts (6-month ahead by level):\n\n")

for (lvl in c("National", "Region", "LGA")) {

cat(sprintf("%s Level (independent forecasts):\n", lvl))

sample <- forecast_results |>

filter(level == lvl & horizon == 6) |>

head(3)

print(sample |> select(series, forecast) |> mutate(forecast = round(forecast, 1)))

cat("\n")

}

cat("Bottom-Up Reconciliation:\n")

cat("National total (sum of LGA bottom-up):\n")

print(bottom_up_national |> mutate(forecast = round(forecast, 1)))

```

## Python

```{python}

#| label: py-ch-25-hierarchical

import pandas as pd

import numpy as np

from statsmodels.tsa.arima.model import ARIMA

import warnings

warnings.filterwarnings('ignore')

# Generate synthetic 36-month demand hierarchy

np.random.seed(789)

months = 36

regions = ["South-West", "South-South", "North-Central", "North-West"]

lgas_per_region = 4

base_demand = 1000

trend_factor = np.linspace(1, 1.8, months)

regional_shares = np.array([0.35, 0.25, 0.25, 0.15])

hierarchy_data = []

for m in range(1, months + 1):

national_demand = (base_demand * trend_factor[m-1] *

(1 + 0.15 * np.sin(2 * np.pi * m / 12)) +

np.random.normal(0, 50))

for r_idx, region in enumerate(regions):

share = regional_shares[r_idx]

region_demand = national_demand * share * (1 + 0.08 * np.random.normal())

lga_shares = np.random.uniform(0, 1, lgas_per_region)

lga_shares = lga_shares / lga_shares.sum()

for l in range(lgas_per_region):

lga_demand = max(region_demand * lga_shares[l] *

(1 + 0.05 * np.random.normal()), 0)

hierarchy_data.append({

'month': m,

'region': region,

'lga': f"{region}_LGA{l+1}",

'demand': lga_demand

})

df_lga = pd.DataFrame(hierarchy_data)

# Create regional and national aggregates

df_regional = df_lga.groupby(['month', 'region'])['demand'].sum().reset_index()

df_national = df_lga.groupby('month')['demand'].sum().reset_index()

df_national['region'] = 'Nigeria'

print("Hierarchy Structure:")

print(f"National level (1 series): Nigeria")

print(f"Regional level (4 series): {', '.join(regions)}")

print(f"LGA level (16 series): 4 LGAs per region\n")

# Forecast each series independently

forecast_results = []

# LGA level

for lga in df_lga['lga'].unique():

lga_series = df_lga[df_lga['lga'] == lga]['demand'].values

if len(lga_series) > 12:

try:

model = ARIMA(lga_series, order=(1, 1, 1))

fit = model.fit()

fcst = fit.forecast(steps=6)

for h, val in enumerate(fcst, 1):

forecast_results.append({

'level': 'LGA',

'series': lga,

'region': lga.split('_')[0],

'horizon': h,

'forecast': val

})

except:

pass

# Regional level

for region in regions:

region_series = df_regional[df_regional['region'] == region]['demand'].values

if len(region_series) > 12:

try:

model = ARIMA(region_series, order=(1, 1, 1))

fit = model.fit()

fcst = fit.forecast(steps=6)

for h, val in enumerate(fcst, 1):

forecast_results.append({

'level': 'Region',

'series': region,

'region': region,

'horizon': h,

'forecast': val

})

except:

pass

# National level

national_series = df_national['demand'].values

try:

model = ARIMA(national_series, order=(1, 1, 1))

fit = model.fit()

fcst = fit.forecast(steps=6)

for h, val in enumerate(fcst, 1):

forecast_results.append({

'level': 'National',

'series': 'Nigeria',

'region': 'Nigeria',

'horizon': h,

'forecast': val

})

except:

pass

df_fcst = pd.DataFrame(forecast_results)

# Bottom-up reconciliation

bottom_up_regional = df_fcst[df_fcst['level'] == 'LGA'].groupby(

['region', 'horizon'])['forecast'].sum().reset_index()

bottom_up_regional['level'] = 'Region'

bottom_up_regional['series'] = bottom_up_regional['region']

bottom_up_national = df_fcst[df_fcst['level'] == 'LGA'].groupby(

'horizon')['forecast'].sum().reset_index()

bottom_up_national['level'] = 'National'

bottom_up_national['series'] = 'Nigeria'

bottom_up_national['region'] = 'Nigeria'

print("Sample Forecasts (6-month ahead by level):\n")

print("National Level (independent):")

national_fcst = df_fcst[(df_fcst['level'] == 'National') &

(df_fcst['horizon'] == 6)]

print(national_fcst[['series', 'forecast']].to_string(index=False))

print("\n\nBottom-Up Reconciliation:\n")

print("National total (sum of LGA forecasts):")

print(bottom_up_national[bottom_up_national['horizon'] == 6][

['series', 'forecast']].round(1).to_string(index=False))

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 25.5 Review Questions

1. Why is it problematic to forecast each level of a hierarchy independently without reconciliation?

2. Explain the trade-off between top-down and bottom-up reconciliation approaches.

3. What is the advantage of MinT reconciliation over simple bottom-up or top-down methods?

4. In a retail hierarchy (store → district → region → national), which reconciliation approach might you choose if you trust store-level forecasts more than regional trends?

5. How would you modify the aggregation matrix $\mathbf{S}$ if you introduced a fourth level (e.g., product categories within each LGA)?

:::

## Forecast Accuracy Metrics: Beyond MAPE

MAPE (Mean Absolute Percentage Error) is widespread but flawed. It is undefined when actuals are zero, heavily weighted toward small values (a 50% error on a value of 100 is treated the same as a 50% error on a value of 10), and asymmetric (it penalises over-forecasts more than under-forecasts of equal magnitude).

**MAPE**: $\text{MAPE} = \frac{100}{n} \sum_{i=1}^{n} \left|\frac{y_i - \hat{y}_i}{y_i}\right|$

**RMSE (Root Mean Squared Error)**: $\text{RMSE} = \sqrt{\frac{1}{n} \sum_{i=1}^{n} (y_i - \hat{y}_i)^2}$. Sensitive to outliers (large errors are squared). Units match the original data.

**MAE (Mean Absolute Error)**: $\text{MAE} = \frac{1}{n} \sum_{i=1}^{n} |y_i - \hat{y}_i|$. Robust to outliers. Units match the data. Simple but not scale-free.

**MASE (Mean Absolute Scaled Error)**: $\text{MASE} = \frac{\text{MAE}}{MAE_{\text{naive}}}$. Compares the model to a seasonal naïve baseline (forecast next value as the same as one year ago). Scale-free: MASE < 1 means better than naïve, MASE = 1 means equal to naïve. A benchmark metric from Hyndman and Koehler (2006).

**SMAPE (Symmetric MAPE)**: $\text{SMAPE} = \frac{100}{n} \sum_{i=1}^{n} \frac{2|y_i - \hat{y}_i|}{|y_i| + |\hat{y}_i|}$. Symmetric and bounded (0 to 100%). Handles zero better than MAPE.

**WAPE (Weighted Absolute Percentage Error)**: $\text{WAPE} = \frac{\sum_{i=1}^{n} |y_i - \hat{y}_i|}{\sum_{i=1}^{n} |y_i|}$. Like MAPE but sums the numerator and denominator separately, avoiding division by individual small values. Good for inventory and demand forecasting.

We compute all metrics on three forecasting methods applied to synthetic Nigerian FMCG demand.

::: {.callout-note icon="false"}

## 📘 Theory: Scale-Free Accuracy Metrics

MASE is defined as:

$$\text{MASE} = \frac{\text{MAE}}{\frac{1}{n-m} \sum_{i=m+1}^{n} |y_i - y_{i-m}|}$$

where the denominator is the MAE of a seasonal naïve forecast with seasonality period $m$. This ensures MASE is independent of the magnitude of the data.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula

**Multiple Accuracy Metrics**:

$$\text{MAPE} = \frac{100}{n} \sum \left|\frac{e_i}{y_i}\right|, \quad \text{RMSE} = \sqrt{\frac{1}{n}\sum e_i^2}, \quad \text{MASE} = \frac{\text{MAE}}{\text{MAE}_{\text{seasonal naïve}}}$$

where $e_i = y_i - \hat{y}_i$ is the forecast error.

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch-25-accuracy-metrics

#| message: false

#| warning: false

library(tidyverse)

library(forecast)

library(lightgbm)

# Generate synthetic 60-month FMCG demand with seasonality

set.seed(101)

months <- 60

base_demand <- 5000

trend <- seq(0, 2000, length.out = months)

seasonal <- 800 * sin(2 * pi * (1:months) / 12) +

400 * sin(2 * pi * (1:months) / 6) # Mixed seasonality

noise <- rnorm(months, 0, 300)

demand <- pmax(base_demand + trend + seasonal + noise, 1000)

dates <- seq(from = as.Date("2019-01-01"), by = "month", length.out = months)

df <- data.frame(date = dates, demand = demand)

# Split: train 48 months, test 12 months

train_df <- df[1:48, ]

test_df <- df[49:60, ]

actual <- test_df$demand

# Method 1: Exponential Smoothing (Holt-Winters)

model_ets <- ets(train_df$demand, model = "ZZZ", allow.multiplicative.trend = TRUE)

fcst_ets <- forecast(model_ets, h = 12)$mean

# Method 2: ARIMA

model_arima <- auto.arima(train_df$demand, trace = FALSE)

fcst_arima <- forecast(model_arima, h = 12)$mean

# Method 3: LightGBM with lag features

df_ml <- df |>

mutate(

lag1 = lag(demand, 1),

lag12 = lag(demand, 12),

lag3 = lag(demand, 3),

ma3 = zoo::rollmean(demand, 3, fill = NA),

ma12 = zoo::rollmean(demand, 12, fill = NA),

month = month(date)

) |>

drop_na()

train_ml <- df_ml[1:(nrow(df_ml) - 12), ]

test_ml <- df_ml[(nrow(df_ml) - 11):nrow(df_ml), ]

X_train <- train_ml |> select(-date, -demand) |> as.matrix()

y_train <- train_ml$demand

X_test <- test_ml |> select(-date, -demand) |> as.matrix()

train_lgb <- lgb.Dataset(X_train, label = y_train)

model_lgb <- lgb.train(

list(objective = "regression", metric = "rmse", num_leaves = 15),

train_lgb, nrounds = 100, verbose = -1

)

fcst_lgb <- predict(model_lgb, X_test)

# Compute all metrics

compute_metrics <- function(actual, forecast, method_name, seasonal_period = 12) {

error <- actual - forecast

# MAPE

mape <- mean(abs(error / actual)) * 100

# RMSE

rmse <- sqrt(mean(error^2))

# MAE

mae <- mean(abs(error))

# SMAPE

smape <- mean(2 * abs(error) / (abs(actual) + abs(forecast))) * 100

# WAPE

wape <- sum(abs(error)) / sum(abs(actual)) * 100

# MASE: compare to seasonal naïve

train_actual <- train_df$demand

seasonal_naive_error <- abs(train_actual[(seasonal_period + 1):length(train_actual)] -

train_actual[1:(length(train_actual) - seasonal_period)])

mae_seasonal_naive <- mean(seasonal_naive_error)

mase <- mae / mae_seasonal_naive

return(data.frame(

Method = method_name,

MAPE = round(mape, 2),

RMSE = round(rmse, 1),

MAE = round(mae, 1),

SMAPE = round(smape, 2),

WAPE = round(wape, 2),

MASE = round(mase, 3)

))

}

metrics_ets <- compute_metrics(actual, fcst_ets, "Exponential Smoothing")

metrics_arima <- compute_metrics(actual, fcst_arima, "ARIMA")

metrics_lgb <- compute_metrics(actual, fcst_lgb, "LightGBM")

metrics_table <- bind_rows(metrics_ets, metrics_arima, metrics_lgb)

cat("Forecast Accuracy Scorecard (12-Month Test Period):\n\n")

print(metrics_table)

# Visualisation: forecast vs actual

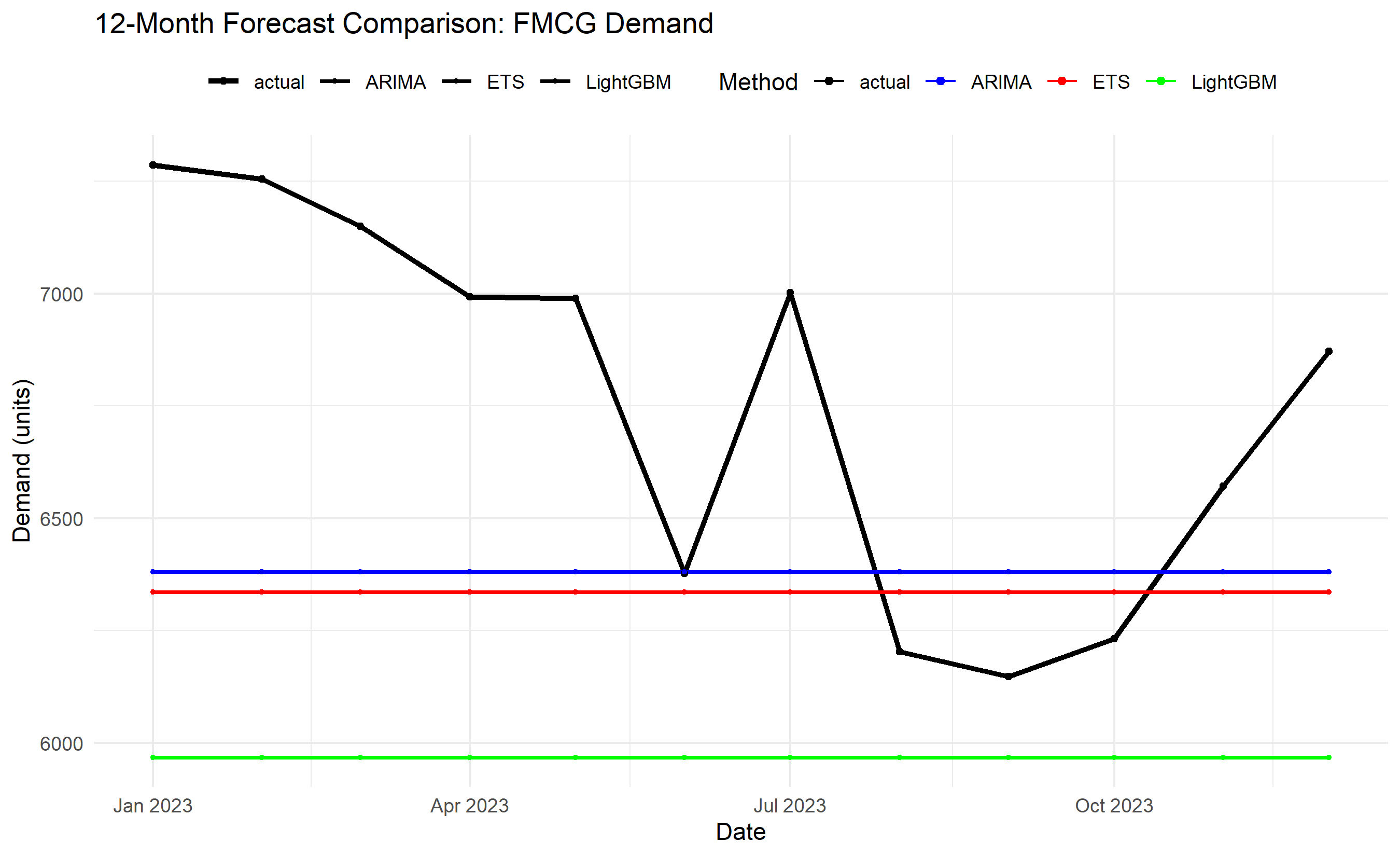

results_viz <- data.frame(

date = test_df$date,

actual = actual,

ETS = fcst_ets,

ARIMA = fcst_arima,

LightGBM = fcst_lgb

) |>

pivot_longer(cols = -date, names_to = "method", values_to = "forecast")

ggplot(results_viz, aes(x = date, y = forecast, colour = method, size = method)) +

geom_line() +

geom_point() +

scale_colour_manual(values = c("actual" = "black", "ETS" = "red",

"ARIMA" = "blue", "LightGBM" = "green")) +

scale_size_manual(values = c("actual" = 1.2, "ETS" = 0.8,

"ARIMA" = 0.8, "LightGBM" = 0.8)) +

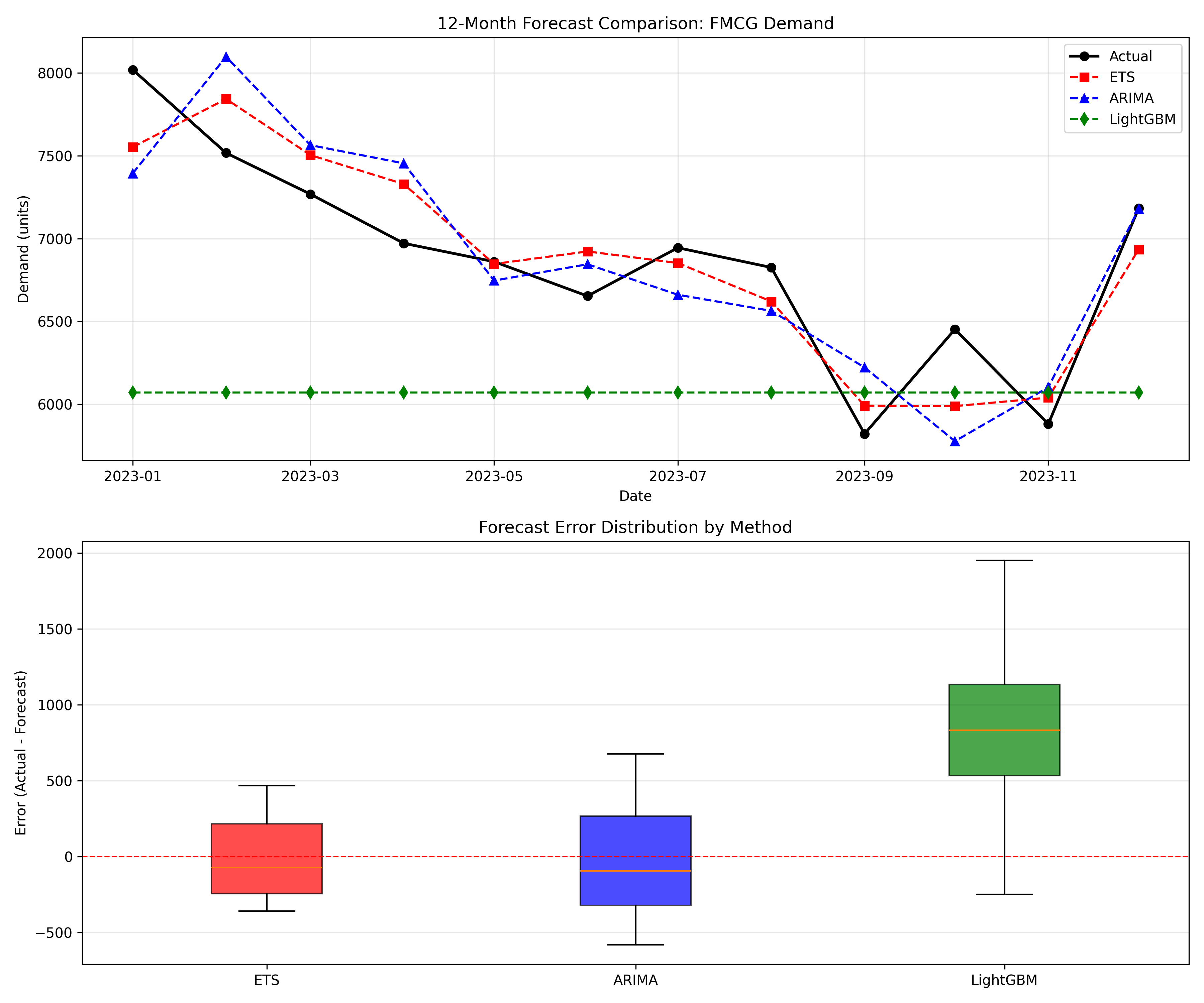

labs(title = "12-Month Forecast Comparison: FMCG Demand",

x = "Date", y = "Demand (units)", colour = "Method", size = NULL) +

theme_minimal() +

theme(legend.position = "top")

# Error distribution boxplot

error_df <- data.frame(

method = c(rep("ETS", 12), rep("ARIMA", 12), rep("LightGBM", 12)),

error = c(actual - fcst_ets, actual - fcst_arima, actual - fcst_lgb)

)

ggplot(error_df, aes(x = method, y = error, fill = method)) +

geom_boxplot(alpha = 0.7) +

geom_hline(yintercept = 0, linetype = "dashed", colour = "red") +

scale_fill_manual(values = c("ETS" = "red", "ARIMA" = "blue", "LightGBM" = "green")) +

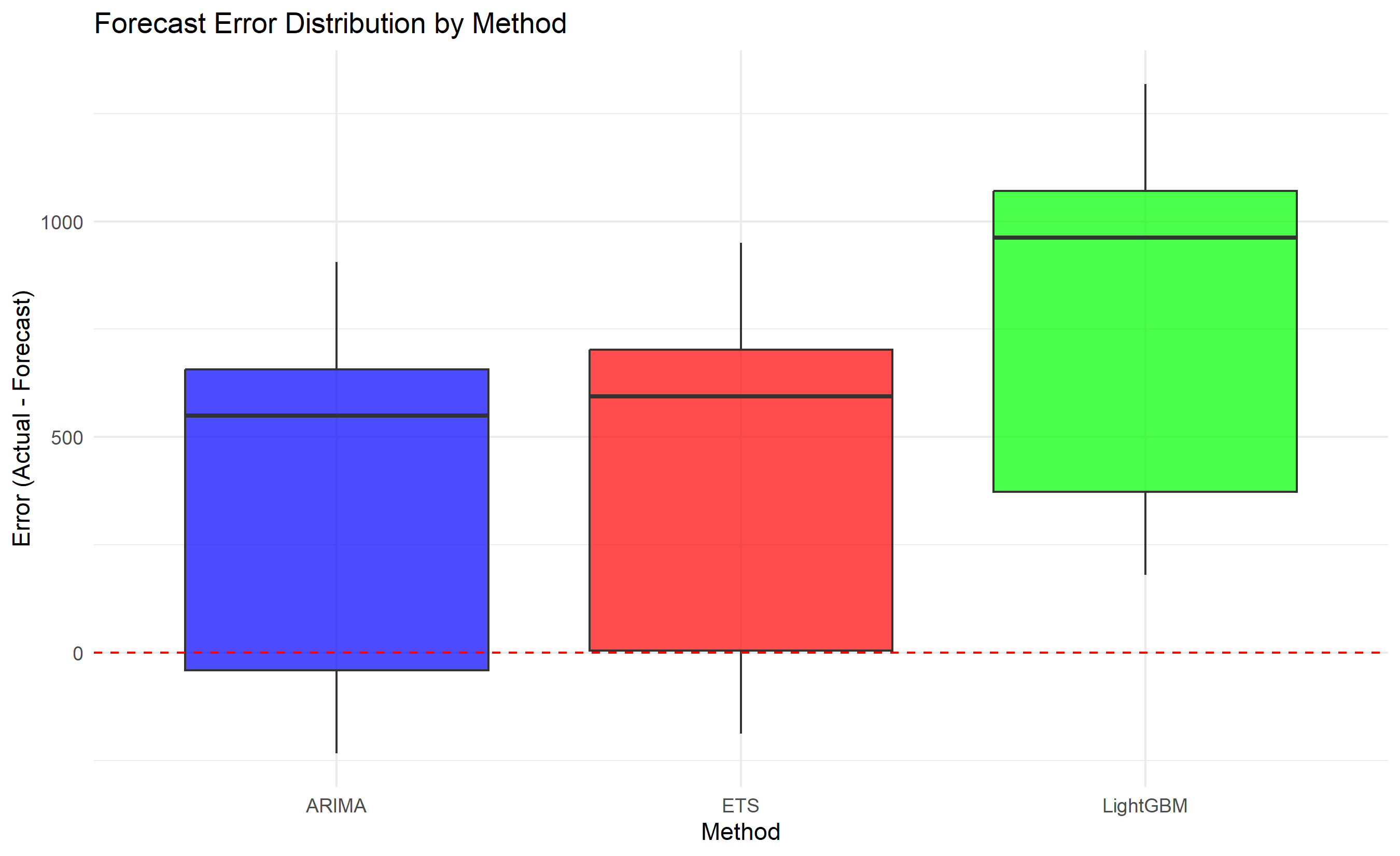

labs(title = "Forecast Error Distribution by Method",

x = "Method", y = "Error (Actual - Forecast)", fill = NULL) +

theme_minimal() +

theme(legend.position = "none")

```

## Python

```{python}

#| label: py-ch-25-accuracy-metrics

import pandas as pd

import numpy as np

from statsmodels.tsa.holtwinters import ExponentialSmoothing

from statsmodels.tsa.arima.model import ARIMA

import lightgbm as lgb

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings('ignore')

# Generate synthetic 60-month FMCG demand

np.random.seed(101)

months = 60

base_demand = 5000

trend = np.linspace(0, 2000, months)

seasonal = (800 * np.sin(2 * np.pi * np.arange(1, months + 1) / 12) +

400 * np.sin(2 * np.pi * np.arange(1, months + 1) / 6))

noise = np.random.normal(0, 300, months)

demand = np.maximum(base_demand + trend + seasonal + noise, 1000)

dates = pd.date_range(start='2019-01-01', periods=months, freq='MS')

df = pd.DataFrame({'date': dates, 'demand': demand})

train_df = df.iloc[:48]

test_df = df.iloc[48:]

actual = test_df['demand'].values

# Method 1: Exponential Smoothing

model_ets = ExponentialSmoothing(train_df['demand'], seasonal='add',

seasonal_periods=12, trend='add')

fit_ets = model_ets.fit()

fcst_ets = fit_ets.forecast(steps=12).values

# Method 2: ARIMA

model_arima = ARIMA(train_df['demand'], order=(1, 1, 1),

seasonal_order=(1, 1, 0, 12))

fit_arima = model_arima.fit()

fcst_arima = fit_arima.forecast(steps=12).values

# Method 3: LightGBM

df_ml = df.copy()

df_ml['lag1'] = df_ml['demand'].shift(1)

df_ml['lag3'] = df_ml['demand'].shift(3)

df_ml['lag12'] = df_ml['demand'].shift(12)

df_ml['ma3'] = df_ml['demand'].rolling(3).mean()

df_ml['ma12'] = df_ml['demand'].rolling(12).mean()

df_ml['month'] = df_ml['date'].dt.month

df_ml = df_ml.dropna()

train_ml = df_ml.iloc[:-12]

test_ml = df_ml.iloc[-12:]

X_train = train_ml.drop(['date', 'demand'], axis=1).values

y_train = train_ml['demand'].values

X_test = test_ml.drop(['date', 'demand'], axis=1).values

train_lgb = lgb.Dataset(X_train, label=y_train)

model_lgb = lgb.train(

{'objective': 'regression', 'metric': 'rmse', 'num_leaves': 15, 'verbose': -1},

train_lgb, num_boost_round=100

)

fcst_lgb = model_lgb.predict(X_test)

def compute_metrics(actual, forecast, method_name, seasonal_period=12):

error = actual - forecast

mape = np.mean(np.abs(error / actual)) * 100

rmse = np.sqrt(np.mean(error**2))

mae = np.mean(np.abs(error))

smape = np.mean(2 * np.abs(error) / (np.abs(actual) + np.abs(forecast))) * 100

wape = np.sum(np.abs(error)) / np.sum(np.abs(actual)) * 100

# MASE

train_actual = train_df['demand'].values

seasonal_naive_error = np.abs(train_actual[seasonal_period:] -

train_actual[:-seasonal_period])

mae_seasonal_naive = np.mean(seasonal_naive_error)

mase = mae / mae_seasonal_naive

return {

'Method': method_name,

'MAPE': round(mape, 2),

'RMSE': round(rmse, 1),

'MAE': round(mae, 1),

'SMAPE': round(smape, 2),

'WAPE': round(wape, 2),

'MASE': round(mase, 3)

}

metrics = pd.DataFrame([

compute_metrics(actual, fcst_ets, "Exponential Smoothing"),

compute_metrics(actual, fcst_arima, "ARIMA"),

compute_metrics(actual, fcst_lgb, "LightGBM")

])

print("Forecast Accuracy Scorecard (12-Month Test Period):\n")

print(metrics.to_string(index=False))

# Plot

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(12, 10))

# Forecasts vs actual

ax1.plot(test_df['date'], actual, 'o-', label='Actual', linewidth=2, markersize=6, color='black')

ax1.plot(test_df['date'], fcst_ets, 's--', label='ETS', linewidth=1.5, color='red')

ax1.plot(test_df['date'], fcst_arima, '^--', label='ARIMA', linewidth=1.5, color='blue')

ax1.plot(test_df['date'], fcst_lgb, 'd--', label='LightGBM', linewidth=1.5, color='green')

ax1.set_xlabel('Date')

ax1.set_ylabel('Demand (units)')

ax1.set_title('12-Month Forecast Comparison: FMCG Demand')

ax1.legend()

ax1.grid(True, alpha=0.3)

# Error distributions

errors_ets = actual - fcst_ets

errors_arima = actual - fcst_arima

errors_lgb = actual - fcst_lgb

bp = ax2.boxplot([errors_ets, errors_arima, errors_lgb],

labels=['ETS', 'ARIMA', 'LightGBM'],

patch_artist=True)

for patch, color in zip(bp['boxes'], ['red', 'blue', 'green']):

patch.set_facecolor(color)

patch.set_alpha(0.7)

ax2.axhline(y=0, color='red', linestyle='--', linewidth=1)

ax2.set_ylabel('Error (Actual - Forecast)')

ax2.set_title('Forecast Error Distribution by Method')

ax2.grid(True, alpha=0.3, axis='y')

plt.tight_layout()

plt.show()

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 25.6 Review Questions

1. Why is MAPE problematic when actuals are close to zero or contain zeros?

2. Explain the difference between MAE and MASE. When would you prefer MASE?

3. If two models have the same RMSE but different MAE values, what does that tell you about their error distributions?

4. In what scenarios would WAPE be preferred to MAPE for evaluating a demand forecast?

5. How should you interpret a MASE of 0.85? Of 1.20?

:::

## Ensemble Forecasting: Combining Models for Robustness

No single forecasting method dominates across all domains and lead times. ARIMA excels at capturing linear trends and simple seasonality. Prophet handles structural breaks and holidays well. ML methods capture nonlinear patterns but may overfit. Ensembles—weighted combinations of multiple models—reduce individual model weaknesses and often outperform any single constituent.

**Simple Average Ensemble**: $\hat{y}_{ensemble} = \frac{1}{M} \sum_{m=1}^{M} \hat{y}_m$. Equal weight to each model.

**Weighted Average**: $\hat{y}_{ensemble} = \sum_{m=1}^{M} w_m \hat{y}_m$, where $\sum w_m = 1$. Weights can be assigned inversely to each model's recent error (give more weight to more accurate models) or learned via cross-validation.

**Stacking**: Train a meta-learner (e.g., linear regression) on the predictions of base models. The meta-learner learns which base models to trust for each type of forecast.

We build an ensemble combining ARIMA, Prophet, and LightGBM. We weight them inversely by their 3-month rolling MAPE so that models with lower recent error get higher weight. The ensemble forecast is a rebalanced combination.

::: {.callout-note icon="false"}

## 📘 Theory: Ensemble Learning for Time Series

The variance of an ensemble is lower than the average variance of the individual models when the model errors are not perfectly correlated. If errors are $e_1, e_2, \ldots, e_M$ with correlations $\rho_{ij}$, the ensemble error variance is:

$$\text{Var}(e_{\text{ensemble}}) = \sum_{i=1}^{M} w_i^2 \sigma_i^2 + 2 \sum_{i < j} w_i w_j \rho_{ij} \sigma_i \sigma_j$$

Uncorrelated models (low $\rho_{ij}$) reduce variance most effectively. This is why combining diverse methods (parametric + ML) works better than combining similar methods.

:::

::: {.callout-tip icon="false"}

## 🔑 Key Formula

**Weighted Ensemble Forecast**:

$$\hat{y}_{ensemble,t} = \frac{\sum_{m=1}^{M} w_m \hat{y}_{m,t}}{\sum_{m=1}^{M} w_m}$$

where weights $w_m$ are inversely proportional to recent error: $w_m = \frac{1}{\text{MAPE}_m^{(k)}}$ (MAPE over past $k$ observations).

:::

::: {.panel-tabset}

## R

```{r}

#| label: ch-25-ensemble

#| message: false

#| warning: false

library(tidyverse)

library(forecast)

library(prophet)

library(lightgbm)

library(zoo)

# Generate 36 months of synthetic sales

set.seed(202)

months <- 36

dates <- seq(from = as.Date("2021-01-01"), by = "month", length.out = months)

base <- 10000

trend <- seq(0, 2000, length.out = months)

seasonal <- 1500 * sin(2 * pi * (1:months) / 12)

noise <- rnorm(months, 0, 500)

sales <- pmax(base + trend + seasonal + noise, 5000)

df <- data.frame(date = dates, sales = sales)

# Split: train 30 months, test 6 months

train_df <- df[1:30, ]

test_df <- df[31:36, ]

actual <- test_df$sales

# Method 1: ARIMA

fit_arima <- auto.arima(train_df$sales, trace = FALSE)

fcst_arima_test <- forecast(fit_arima, h = 6)$mean

# Track rolling MAPE for retraining

rolling_window <- 6

arima_history <- forecast(fit_arima, h = 6)$mean

# Method 2: Prophet

df_prophet <- data.frame(ds = dates, y = sales)

train_prophet <- df_prophet[1:30, ]

m_prophet <- prophet(train_prophet, yearly.seasonality = TRUE,

weekly.seasonality = FALSE, interval.width = 0.90)

future_prophet <- make_future_dataframe(m_prophet, periods = 6, freq = "month")

fcst_prophet <- predict(m_prophet, future_prophet)

fcst_prophet_test <- fcst_prophet$yhat[31:36]

# Method 3: LightGBM with lag features

df_ml <- df |>

mutate(

lag1 = lag(sales, 1),

lag3 = lag(sales, 3),

lag12 = lag(sales, 12),

ma3 = rollmean(sales, 3, fill = NA, align = "right"),

ma12 = rollmean(sales, 12, fill = NA, align = "right"),

month = month(date)

) |>

drop_na()

train_ml <- df_ml[df_ml$date <= max(train_df$date), ]

test_ml <- df_ml[df_ml$date > max(train_df$date), ]

X_train <- train_ml |> select(-date, -sales) |> as.matrix()

y_train <- train_ml$sales

X_test <- test_ml |> select(-date, -sales) |> as.matrix()

train_lgb <- lgb.Dataset(X_train, label = y_train)

m_lgb <- lgb.train(

list(objective = "regression", metric = "rmse", num_leaves = 15),

train_lgb, nrounds = 100, verbose = -1

)

fcst_lgb_test <- predict(m_lgb, X_test)

# Compute recent MAPE for each model (weight calculation)

# Use last 6 training observations for this

recent_window <- 6

recent_idx <- (length(train_df$sales) - recent_window + 1):length(train_df$sales)

# Fit on full training set and get residuals

fit_arima_full <- auto.arima(train_df$sales, trace = FALSE)

residuals_arima <- residuals(fit_arima_full)

recent_residuals_arima <- residuals_arima[length(residuals_arima) - recent_window + 1:recent_window]

mape_arima <- mean(abs(recent_residuals_arima / train_df$sales[recent_idx])) * 100

# Prophet residuals (fit again to compute them)

m_prophet_full <- prophet(data.frame(ds = train_df$date, y = train_df$sales),

yearly.seasonality = TRUE, weekly.seasonality = FALSE)

fcst_prophet_full <- predict(m_prophet_full, data.frame(ds = train_df$date))

residuals_prophet <- train_df$sales - fcst_prophet_full$yhat

recent_residuals_prophet <- residuals_prophet[recent_window + 1:recent_window]

mape_prophet <- mean(abs(recent_residuals_prophet / train_df$sales[recent_idx])) * 100

# LightGBM residuals

fcst_lgb_train <- predict(m_lgb, X_train)

residuals_lgb <- y_train - fcst_lgb_train

recent_residuals_lgb <- residuals_lgb[length(residuals_lgb) - recent_window + 1:recent_window]

mape_lgb <- mean(abs(recent_residuals_lgb / y_train[recent_idx])) * 100

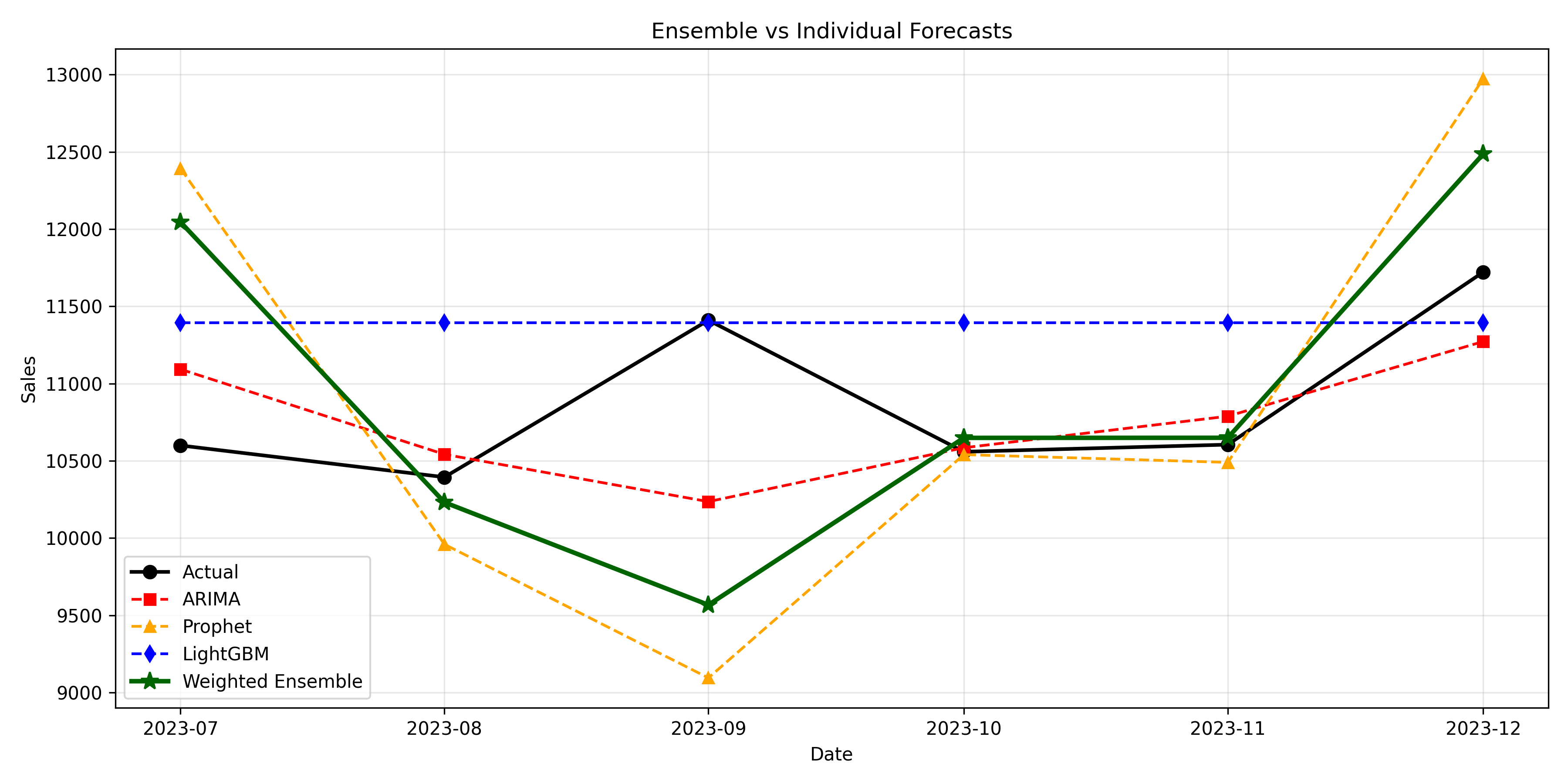

# Calculate weights (inverse MAPE)

weights <- c(1/mape_arima, 1/mape_prophet, 1/mape_lgb)

weights <- weights / sum(weights)

cat("Individual Model Weights (based on recent MAPE):\n")

cat(sprintf("ARIMA: %.1f%% (MAPE: %.2f%%)\n", weights[1]*100, mape_arima))

cat(sprintf("Prophet: %.1f%% (MAPE: %.2f%%)\n", weights[2]*100, mape_prophet))

cat(sprintf("LightGBM: %.1f%% (MAPE: %.2f%%)\n\n", weights[3]*100, mape_lgb))

# Ensemble forecast

fcst_ensemble_test <- weights[1] * fcst_arima_test +

weights[2] * fcst_prophet_test +

weights[3] * fcst_lgb_test

# Evaluation

compute_errors <- function(actual, forecast, name) {

error <- actual - forecast

mape <- mean(abs(error / actual)) * 100

rmse <- sqrt(mean(error^2))

mae <- mean(abs(error))

return(data.frame(

Method = name,

MAPE = round(mape, 2),

RMSE = round(rmse, 1),

MAE = round(mae, 1)

))

}

results <- bind_rows(

compute_errors(actual, fcst_arima_test, "ARIMA"),

compute_errors(actual, fcst_prophet_test, "Prophet"),

compute_errors(actual, fcst_lgb_test, "LightGBM"),

compute_errors(actual, fcst_ensemble_test, "Weighted Ensemble")

)

cat("Test Set Performance (6-month forecast):\n")

print(results)

# Visualization

forecast_comp <- data.frame(

month = 1:6,

date = test_df$date,

actual = actual,

ARIMA = fcst_arima_test,

Prophet = fcst_prophet_test,

LightGBM = fcst_lgb_test,

Ensemble = fcst_ensemble_test

) |>

pivot_longer(cols = -c(month, date), names_to = "method", values_to = "forecast")

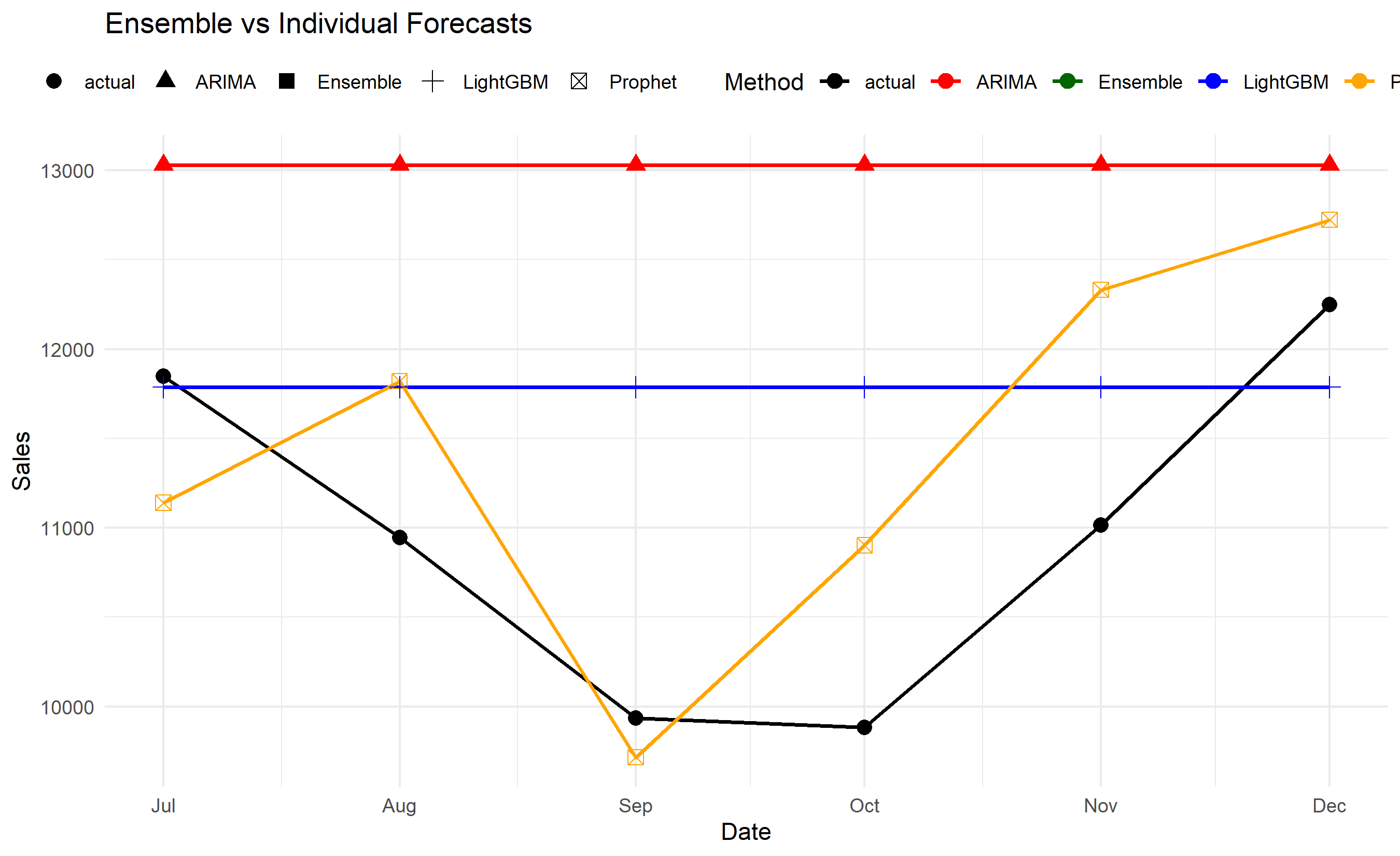

ggplot(forecast_comp, aes(x = date, y = forecast, colour = method, shape = method)) +

geom_line(linewidth = 0.8) +

geom_point(size = 3) +

scale_colour_manual(values = c("actual" = "black", "ARIMA" = "red",

"Prophet" = "orange", "LightGBM" = "blue",

"Ensemble" = "darkgreen")) +

labs(title = "Ensemble vs Individual Forecasts",

x = "Date", y = "Sales", colour = "Method", shape = NULL) +

theme_minimal() +

theme(legend.position = "top")

```

## Python

```{python}

#| label: py-ch-25-ensemble

import pandas as pd

import numpy as np

from statsmodels.tsa.arima.model import ARIMA

from prophet import Prophet

import lightgbm as lgb

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings('ignore')

# Generate 36 months of synthetic sales

np.random.seed(202)

months = 36

dates = pd.date_range(start='2021-01-01', periods=months, freq='MS')

base = 10000

trend = np.linspace(0, 2000, months)

seasonal = 1500 * np.sin(2 * np.pi * np.arange(1, months + 1) / 12)

noise = np.random.normal(0, 500, months)

sales = np.maximum(base + trend + seasonal + noise, 5000)

df = pd.DataFrame({'date': dates, 'sales': sales})

train_df = df.iloc[:30]

test_df = df.iloc[30:]

actual = test_df['sales'].values

# Method 1: ARIMA

model_arima = ARIMA(train_df['sales'], order=(1, 1, 1), seasonal_order=(1, 0, 0, 12))

fit_arima = model_arima.fit()

fcst_arima = fit_arima.forecast(steps=6).values

# Method 2: Prophet

df_prophet = pd.DataFrame({'ds': dates, 'y': sales})

train_prophet = df_prophet.iloc[:30]

m_prophet = Prophet(yearly_seasonality=True, weekly_seasonality=False, interval_width=0.90)

m_prophet.fit(train_prophet)

future = m_prophet.make_future_dataframe(periods=6, freq='MS')

fcst_prophet_df = m_prophet.predict(future)

fcst_prophet = fcst_prophet_df.iloc[30:36]['yhat'].values

# Method 3: LightGBM

df_ml = df.copy()

df_ml['lag1'] = df_ml['sales'].shift(1)

df_ml['lag3'] = df_ml['sales'].shift(3)

df_ml['lag12'] = df_ml['sales'].shift(12)

df_ml['ma3'] = df_ml['sales'].rolling(3).mean()

df_ml['ma12'] = df_ml['sales'].rolling(12).mean()

df_ml['month'] = df_ml['date'].dt.month

df_ml = df_ml.dropna()

train_ml = df_ml[df_ml['date'] <= train_df['date'].max()]

test_ml = df_ml[df_ml['date'] > train_df['date'].max()]

X_train = train_ml.drop(['date', 'sales'], axis=1).values

y_train = train_ml['sales'].values

X_test = test_ml.drop(['date', 'sales'], axis=1).values

train_lgb = lgb.Dataset(X_train, label=y_train)

m_lgb = lgb.train({'objective': 'regression', 'metric': 'rmse', 'num_leaves': 15, 'verbose': -1},

train_lgb, num_boost_round=100)

fcst_lgb = m_lgb.predict(X_test)

# Compute weights based on recent MAPE

recent_window = 6

recent_idx = slice(-recent_window, None)

# Residuals from training

fit_arima_full = ARIMA(train_df['sales'], order=(1, 1, 1), seasonal_order=(1, 0, 0, 12)).fit()

residuals_arima = fit_arima_full.resid.iloc[recent_idx].values

mape_arima = np.mean(np.abs(residuals_arima / train_df['sales'].iloc[recent_idx].values)) * 100

m_prophet_full = Prophet(yearly_seasonality=True, weekly_seasonality=False)

m_prophet_full.fit(pd.DataFrame({'ds': train_df['date'], 'y': train_df['sales']}))

fcst_prophet_full = m_prophet_full.predict(pd.DataFrame({'ds': train_df['date']}))

residuals_prophet = train_df['sales'].values - fcst_prophet_full['yhat'].values

residuals_prophet = residuals_prophet[recent_idx]

mape_prophet = np.mean(np.abs(residuals_prophet / train_df['sales'].iloc[recent_idx].values)) * 100

fcst_lgb_train = m_lgb.predict(X_train)

residuals_lgb = y_train - fcst_lgb_train

residuals_lgb = residuals_lgb[-recent_window:]

mape_lgb = np.mean(np.abs(residuals_lgb / y_train[-recent_window:])) * 100

# Weights inverse to MAPE

weights = np.array([1/mape_arima, 1/mape_prophet, 1/mape_lgb])

weights = weights / weights.sum()

print("Individual Model Weights (based on recent MAPE):")

print(f"ARIMA: {weights[0]*100:.1f}% (MAPE: {mape_arima:.2f}%)")

print(f"Prophet: {weights[1]*100:.1f}% (MAPE: {mape_prophet:.2f}%)")

print(f"LightGBM: {weights[2]*100:.1f}% (MAPE: {mape_lgb:.2f}%)\n")

# Ensemble

fcst_ensemble = weights[0] * fcst_arima + weights[1] * fcst_prophet + weights[2] * fcst_lgb

def compute_errors(actual, forecast, name):

error = actual - forecast

mape = np.mean(np.abs(error / actual)) * 100

rmse = np.sqrt(np.mean(error**2))

mae = np.mean(np.abs(error))

return {'Method': name, 'MAPE': round(mape, 2), 'RMSE': round(rmse, 1), 'MAE': round(mae, 1)}

results = pd.DataFrame([

compute_errors(actual, fcst_arima, "ARIMA"),

compute_errors(actual, fcst_prophet, "Prophet"),

compute_errors(actual, fcst_lgb, "LightGBM"),

compute_errors(actual, fcst_ensemble, "Weighted Ensemble")

])

print("Test Set Performance (6-month forecast):")

print(results.to_string(index=False))

# Plot

fig, ax = plt.subplots(figsize=(12, 6))

ax.plot(test_df['date'], actual, 'o-', label='Actual', linewidth=2, markersize=7, color='black')

ax.plot(test_df['date'], fcst_arima, 's--', label='ARIMA', linewidth=1.5, color='red')

ax.plot(test_df['date'], fcst_prophet, '^--', label='Prophet', linewidth=1.5, color='orange')

ax.plot(test_df['date'], fcst_lgb, 'd--', label='LightGBM', linewidth=1.5, color='blue')

ax.plot(test_df['date'], fcst_ensemble, '*-', label='Weighted Ensemble', linewidth=2.5, color='darkgreen', markersize=10)

ax.set_xlabel('Date')

ax.set_ylabel('Sales')

ax.set_title('Ensemble vs Individual Forecasts')

ax.legend(loc='best')

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

:::

::: {.callout-caution icon="false"}

## 📝 Section 25.7 Review Questions

1. Why do ensemble forecasts tend to outperform individual models?

2. How would you assign weights in a weighted average ensemble if you had 24 months of historical forecasts and errors?

3. What is the relationship between model correlation and ensemble variance reduction?

4. Explain the difference between a weighted average ensemble and a stacking ensemble. When would you use each?

5. In the code above, why do we weight by the inverse of recent MAPE rather than using equal weights?

:::

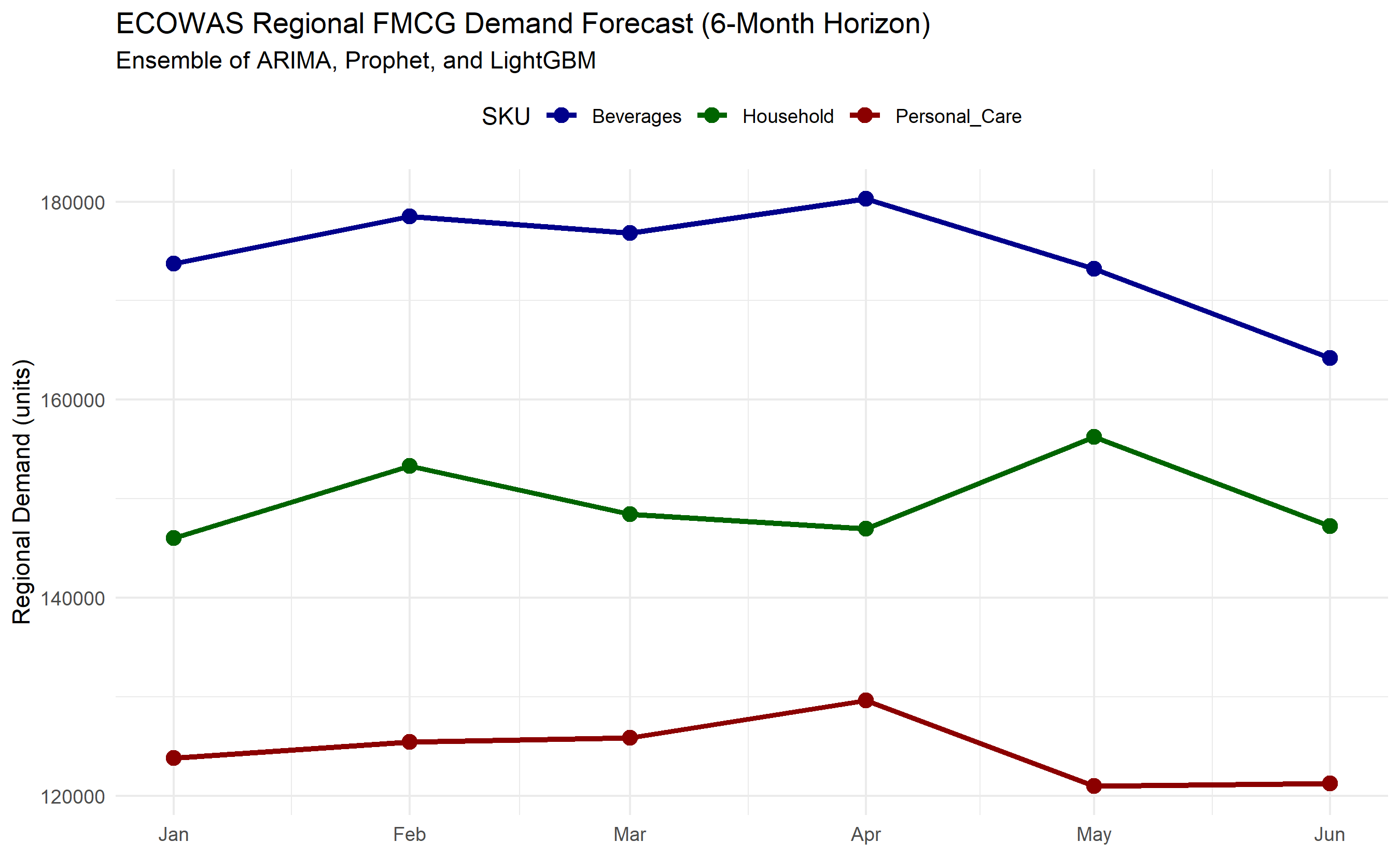

## Case Study: Multi-SKU FMCG Demand Forecasting for ECOWAS Nations

A regional FMCG distributor supplies beverages, personal care, and household products across six ECOWAS nations: Nigeria, Ghana, Côte d'Ivoire, Senegal, Kenya, and Mali (synthetic, for illustration). The company maintains 24 months of monthly sales data (Jan 2022 – Dec 2023) for each of three SKU categories per country, giving 18 time series. The business requires:

1. A 6-month rolling forecast for inventory planning

2. Prediction intervals (80% and 95%) for safety stock calculation

3. A country-by-country and SKU-level accuracy scorecard

4. A management summary highlighting forecast confidence and risks

We build an ensemble of ARIMA, Prophet, and LightGBM, fit each on all 18 series, generate 6-month forecasts, reconcile to total regional demand, and produce a visual dashboard.

**Data Structure**: Synthetic monthly sales (Jan 2022 – Dec 2023) for each (country, SKU) pair. Data exhibit multiplicative seasonality, trends, and occasional structural breaks.

```{r}

#| label: ch-25-case-setup

#| message: false

#| warning: false

library(tidyverse)

library(forecast)

library(prophet)

library(lightgbm)

library(knitr)

# Define structure

countries <- c("Nigeria", "Ghana", "Ivory_Coast", "Senegal", "Kenya", "Mali")

skus <- c("Beverages", "Personal_Care", "Household")

months <- 24

dates <- seq(from = as.Date("2022-01-01"), by = "month", length.out = months)

set.seed(999)

# Generate synthetic data